Kalman Trend Sniper# KALMAN TREND SNIPER

## ORIGINALITY STATEMENT

The Kalman Trend Sniper combines adaptive trend detection with precision entry validation to identify high-probability trading opportunities. Unlike static moving averages that use fixed parameters, this indicator adapts to changing market volatility through ATR-based gain adjustment and distinguishes trending from ranging markets using ADX regime detection.

The indicator's unique contribution is its three-phase entry validation system: signals must hold for three bars, undergo a pullback test to the signal level, and receive confirmation through price action before generating an entry. This structured approach helps traders enter established trends at favorable retracement levels rather than chasing momentum.

---

## TECHNICAL METHODOLOGY

### Kalman Filter Implementation

This indicator implements an Alpha-Beta variant of the Kalman filter, a recursive algorithm that estimates trend from noisy price data:

1. Prediction: kf = kf + velocity

2. Error calculation: error = price - kf

3. Correction: kf = kf + gain * error

4. Velocity update: velocity = velocity + (gain * error) / 2

The gain parameter determines filter responsiveness. Higher gain values track price more closely but increase noise sensitivity, while lower values provide smoother output but lag price changes.

### Adaptive Gain Mechanism

The indicator adjusts gain dynamically based on volatility:

Volatility Factor = Current ATR / Long-term ATR

Adaptive Gain = Base Gain * (0.7 + 0.6 * Volatility Factor)

This ATR ratio increases responsiveness during high-volatility periods and reduces sensitivity during consolidations, addressing the fixed-parameter limitation of traditional moving averages. The volatility factor is bounded between configurable minimum and maximum values to prevent extreme adjustments.

### Regime Detection

The indicator uses the Average Directional Index (ADX) to distinguish market conditions:

- Trending markets (ADX above threshold): Full gain applied, signals generated

- Ranging markets (ADX below threshold): Gain reduced 25%, fewer signals

This regime awareness helps reduce whipsaw signals during sideways consolidation periods.

### Signal Line Validation System

When the Kalman line changes direction in trending conditions, the indicator draws a horizontal signal line at the low (for long signals) or high (for short signals) of the signal candle. This line represents a potential support or resistance level.

The validation system then monitors three phases:

Phase 1 - Hold Period: Price must remain above (long) or below (short) the signal line for three consecutive bars. This requirement filters weak signals where price immediately violates the signal level.

Phase 2 - Test: After the hold period, the system waits for price to pull back and touch the signal line, with configurable tolerance for volatile instruments.

Phase 3 - Confirmation: Within eight bars of the test, a confirmation candle must close above (long) or below (short) the test candle's body, demonstrating renewed momentum. If confirmation does not occur within eight bars, the validation attempt expires.

Successful validation generates an R label at the entry point. This three-phase structure helps identify entries where trend direction and support/resistance validation align.

---

## USAGE INSTRUCTIONS

### Signal Interpretation

Triangle Signals:

- Upward triangle (teal): Kalman line turns bullish in trending market (ADX above threshold)

- Downward triangle (red): Kalman line turns bearish in trending market

Signal Lines (horizontal):

- Teal line: Potential long support level at signal candle low

- Red line: Potential short resistance level at signal candle high

- Gray line: First opposite-color candle after signal (initial reversal pressure)

R Labels (optional, disabled by default):

- Green R below price: Validation complete for long entry

- Red R above price: Validation complete for short entry

Stop Levels:

- Red dots: Long stop level (Kalman line minus ATR multiplier)

- Teal dots: Short stop level (Kalman line plus ATR multiplier)

### Dashboard Information

The dashboard displays real-time indicator state:

- Trend: Current Kalman direction (BULL/BEAR)

- Regime: Market classification (Trending when ADX exceeds threshold, Ranging otherwise)

- Gain: Current adaptive gain value

- Vol Factor: Volatility ratio (current ATR / long-term ATR)

- ADX: Trend strength (higher values indicate stronger trends)

- Z-Score: Standard deviation distance from Kalman line (when enabled)

- Stop Dist: Current ATR-based stop distance

- Lines: Number of active signal lines displayed

- R-Status: Validation system state (Idle / Waiting / Testing)

### Trading Applications

Trend Following Approach:

1. Wait for triangle signal in trending market (ADX above threshold)

2. Enter immediately at signal candle close or wait for pullback

3. Place stop at displayed stop level

4. Trail stop using Kalman line as dynamic support/resistance

Validation Entry Approach (conservative):

1. After triangle signal, observe three-bar hold period

2. Wait for pullback to signal line (test phase)

3. Enter on R label confirmation

4. Place stop below/above signal line

5. Provides higher probability entries but reduces trade frequency

Z-Score Mean Reversion (when enabled):

1. Watch for Z-Score exceeding entry threshold (default +/-2.0)

2. Consider counter-trend entries when price touches Kalman line

3. Target return to Kalman line (Z-Score near zero)

4. Use Z-Score threshold as stop level for extreme continuation

### Optimal Conditions

The indicator performs optimally in clearly trending markets where ADX consistently exceeds the threshold. Performance degrades in sideways, choppy conditions.

Recommended timeframes:

- 1-5 minute charts: Use Crypto_1M preset (faster adaptation)

- 15-60 minute charts: Use Crypto_15M preset (balanced)

- Hourly charts: Use Forex preset (smoother)

- Daily charts: Use Stocks_Daily preset (long-term trends)

Market conditions:

- High volatility (Vol Factor above 1.5): Expect faster adaptation, wider stops needed

- Normal volatility (Vol Factor 0.7-1.5): Standard behavior

- Low volatility (Vol Factor below 0.7): Expect slower adaptation, tighter stops possible

---

## PARAMETER DOCUMENTATION

### Kalman Filter Settings

Preset Mode: Select optimized configuration for specific markets

- Custom: Manual parameter control

- Crypto_1M: Base Gain 0.05, ATR 7 (fast response for 1-5 minute crypto charts)

- Crypto_15M: Base Gain 0.03, ATR 14 (balanced for 15-60 minute crypto charts)

- Forex: Base Gain 0.02, ATR 14 (standard for forex pairs)

- Stocks_Daily: Base Gain 0.01, ATR 20 (smooth for daily stock charts)

Base Gain (0.001-0.2): Core Kalman filter responsiveness parameter. Higher values increase sensitivity to price changes. Low values (0.01-0.02) provide smooth output with fewer whipsaws but slower trend changes. High values (0.06-0.08) offer fast response with more signals but increased whipsaw risk.

Adaptive (checkbox): When enabled, automatically adjusts gain based on ATR ratio. Recommended to keep enabled for dynamic volatility adaptation.

ATR (5-50): Short-term Average True Range period for current volatility measurement. Default 14 is industry standard. Lower values respond faster to volatility changes.

Long ATR (20-200): Long-term ATR period for baseline volatility comparison. Default 50 provides stable reference. The ratio between ATR and Long ATR determines adaptive adjustment magnitude.

Regime Filter (checkbox): Enables ADX-based trending/ranging detection. When enabled, reduces gain by 25 percent during ranging markets to minimize false signals.

ADX Period (7-30): Period for ADX calculation. Default 14 is standard. Lower values respond faster to trend strength changes.

Threshold (15-40): ADX level distinguishing trending from ranging markets. Default 25. Above threshold: trending (generate signals normally). Below threshold: ranging (reduce sensitivity).

Min Vol / Max Vol (0.3-3.0): Bounds for volatility factor adjustment. Prevents extreme gain changes during unusual volatility spikes or quiet periods. Default minimum 0.5, maximum 2.0.

Stop ATR x (1.0-3.0): Multiplier for ATR-based stop loss distance. Default 2.0 places stops two ATRs from Kalman line. Use 1.5 for tight stops (intraday), 2.5-3.0 for wide stops (swing trading).

Show Signals (checkbox): Displays triangle signals when Kalman changes direction in trending markets. Disable to use indicator purely as dynamic support/resistance without signals.

Z-Score (checkbox): Enables mean-reversion signal generation based on statistical deviation from Kalman line.

Period (10-100): Lookback period for Z-Score standard deviation calculation. Default 20 bars. Longer periods produce smoother, less sensitive readings.

Entry (1.5-3.5): Standard deviation threshold for Z-Score signals. Default 2.0 generates signals at plus/minus two standard deviations (approximately 95th percentile moves).

Bull / Bear Colors: Customize Kalman line colors for uptrend (default teal) and downtrend (default red).

Fill (checkbox): Shows semi-transparent fill between price and Kalman line for visual trend emphasis.

### Signal Line System Settings

Signal Lines (checkbox): Displays horizontal signal lines at low (long) or high (short) of signal candles. These function as dynamic support/resistance levels.

Reverse Lines (checkbox): Shows gray horizontal lines at first opposite-colored candle after signal. Helps identify initial resistance points in new trends.

Max Lines (0-20): Maximum number of signal lines to display simultaneously. Older lines are removed as new signals appear. Use 1-2 for clean charts, 3-5 for recent support/resistance history.

Style (Solid/Dotted/Dashed): Visual style for signal and reverse lines. Dotted provides subtle appearance, solid is most prominent.

Line % / Label % (0-100): Transparency percentage for lines and labels. Zero is fully opaque, 100 is invisible.

R Labels (checkbox): Shows R labels when validation confirmation occurs. Default disabled. Enable if you want visual confirmation of successful pullback entries.

Tolerance % (0-1.0): Price deviation tolerance for test candle detection. Zero requires exact touch. 0.5 allows 0.5 percent deviation for volatile instruments.

### Dashboard Settings

Show Dashboard (checkbox): Toggles visibility of information panel. Disable for clean chart presentation.

Position: Choose dashboard location from nine positions (Top/Middle/Bottom combined with Left/Center/Right).

---

## LIMITATIONS AND WARNINGS

This indicator is a technical analysis tool that processes historical price data. It does not predict future price movements.

Inherent limitations:

1. Lagging nature: Like all trend indicators, the Kalman filter lags price. Signals occur after trend changes begin, not before.

2. Ranging markets: Generates fewer signals and reduced performance when ADX falls below threshold. Not optimized for sideways consolidation.

3. Whipsaw risk: In choppy, indecisive markets near ADX threshold, signals may reverse quickly despite regime filtering.

4. Parameter sensitivity: Inappropriate Base Gain settings can cause over-trading (too high) or missed trends (too low).

5. Validation requirement: The three-phase confirmation system provides higher accuracy but significantly reduces trade frequency. Not all trends produce valid pullback entries.

Not suitable for:

- Scalping strategies requiring instant signals (Kalman filter has intentional smoothing)

- Ultra-high frequency trading (indicator updates once per bar close)

- Markets with extreme overnight gaps (stops may be exceeded)

- Strategies requiring signals on Heikin Ashi, Renko, Kagi, Point and Figure, or Range charts

Risk management requirements:

This indicator provides trend direction and signal levels but does not incorporate position sizing, risk management, or account balance considerations. Users must implement appropriate position sizing, maximum daily loss limits, and portfolio diversification. Past performance does not indicate future results.

Optimal usage:

- Works optimally in clearly trending markets where ADX consistently exceeds threshold

- Performance degrades in sideways, choppy conditions

- Designed for swing trading and position trading timeframes (15-minute and above)

- Requires confirmation from price action or additional technical analysis

---

## NO REPAINT GUARANTEE

This indicator operates on bar close confirmation only. All signals, signal lines, and validation labels appear exclusively when candles close. Historical signals remain exactly where they appeared. This makes the indicator suitable for automated trading and reliable backtesting. What you see in historical data matches what appeared in real-time.

---

## ALERTS

The indicator provides eight alert conditions:

1. Kalman Buy Signal: Fires when upward triangle appears (bullish trend change in trending market)

2. Kalman Sell Signal: Fires when downward triangle appears (bearish trend change in trending market)

3. Trend Change to Bullish: Fires whenever Kalman line changes to bullish (regardless of ADX)

4. Trend Change to Bearish: Fires whenever Kalman line changes to bearish (regardless of ADX)

5. SCT-R Long Retest Confirmed: Fires when green R label appears for long validation

6. SCT-R Short Retest Confirmed: Fires when red R label appears for short validation

7. SCT Test Long Detected: Fires when test candle appears for long signal (before confirmation)

8. SCT Test Short Detected: Fires when test candle appears for short signal (before confirmation)

Alert messages include context about bar close confirmation and current price levels.

---

## CALCULATION TRANSPARENCY

While complete proprietary optimization methodology is not disclosed, the core technical approach is fully explained: Alpha-Beta Kalman filter with ATR-based adaptive gain adjustment and ADX regime detection. The signal line validation system uses a three-phase structure (hold, test, confirmation) with configurable parameters. Users can understand indicator functionality and make informed decisions about application.

---

## DISCLAIMER

This indicator is provided as a technical analysis tool. It does not constitute financial advice, trading recommendations, or performance guarantees. All trading decisions carry risk. Users are responsible for their own trading decisions and risk management. Past results do not indicate future performance.

Kalman

VWAP Kalman FilterOverview

This indicator applies Kalman filtering techniques to Volume Weighted Average Price (VWAP) calculations, providing a statistically optimized approach to VWAP analysis. The Kalman filter reduces noise while maintaining responsiveness to genuine price movements, addressing common VWAP limitations in volatile or low-volume conditions.

Technical Implementation

Kalman Filter Mathematics

The indicator implements a state-space model for VWAP estimation:

- Prediction Step: x̂(k|k-1) = x̂(k-1|k-1) + v(k-1)

- Update Step: x̂(k|k) = x̂(k|k-1) + K(k)

- Kalman Gain: K(k) = P(k|k-1) / (P(k|k-1) + R)

Where:

- x̂ = estimated VWAP state

- K = Kalman gain (adaptive weighting factor)

- P = error covariance

- R = measurement noise

- Q = process noise

- v = optional velocity component

Core Components

Dual VWAP System

- Standard VWAP: Traditional volume-weighted calculation

- Kalman-filtered VWAP: Noise-reduced estimation with optional velocity tracking

- Real-time divergence measurement between filtered and unfiltered values

Adaptive Filtering

- Process Noise (Q): Controls adaptation to price changes (0.001-1.0)

- Measurement Noise (R): Determines smoothing intensity (0.01-5.0)

- Optional velocity tracking for momentum-based filtering

Multi-Timeframe Anchoring

- Session, Weekly, Monthly, Quarterly, and Yearly anchor periods

- Automatic Kalman state reset on anchor changes

- Maintains VWAP integrity across timeframes

Features

Visual Components

- Dual VWAP Lines: Compare filtered vs. unfiltered in real-time

- Dynamic Bands: Three-level deviation bands (1σ, 2σ, 3σ)

- Trend Coloring: Automatic color adaptation based on price position

- Cloud Visualization: Highlights divergence between standard and Kalman VWAP

- Signal Markers: Crossover and band-touch indicators

Trading Signals

- VWAP crossover detection with Kalman filtering

- Band touch alerts at multiple standard deviation levels

- Velocity-based momentum confirmation (optional)

- Divergence warnings when filtered/unfiltered values separate

Information Display

- Real-time VWAP values (both standard and filtered)

- Trend direction indicator

- Velocity/momentum reading (when enabled)

- Divergence percentage calculation

- Anchor period display

Input Parameters

VWAP Settings

- Anchor Period: Choose calculation reset period

- Band Multipliers: Customize deviation band distances

- Display Options: Toggle standard VWAP and bands

Kalman Parameters

- Length: Base period for calculations (5-200)

- Process Noise (Q: Higher values increase responsiveness

- Measurement Noise (R): Higher values increase smoothing

- Velocity Tracking: Enable momentum-based filtering

Visual Controls

- Toggle filtered/unfiltered VWAP display

- Band visibility options

- Signal markers on/off

- Cloud fill between VWAPs

- Bar coloring by trend

Use Cases

Noise Reduction

Particularly effective during:

- Low volume periods (pre-market, lunch hours)

- Volatile market conditions

- Fast-moving markets where standard VWAP whipsaws

Trend Identification

- Cleaner trend signals with reduced false crosses

- Earlier trend detection through velocity component

- Confirmation through divergence analysis

Support/Resistance

- Filtered VWAP provides more stable S/R levels

- Bands adapt to filtered values for better zone identification

- Reduced false breakout signals

Technical Advantages

1. Optimal Estimation: Mathematically optimal under Gaussian noise assumptions

2. Adaptive Response: Self-adjusting to market conditions

3. Predictive Element: Velocity component provides forward-looking insight

4. Noise Immunity: Superior noise rejection vs. simple moving average smoothing

Limitations

- Assumes linear price dynamics

- Requires parameter optimization for different instruments

- May lag during sudden volatility regime changes

- Not suitable as standalone trading system

Mathematical Background

Based on control systems theory, the Kalman filter provides recursive Bayesian estimation originally developed for aerospace applications. This implementation adapts the algorithm specifically for financial time series, maintaining VWAP's volume-weighted properties while adding statistical filtering.

Comparison with Standard VWAP

Standard VWAP Issues Addressed:

- Choppy behavior in low volume

- Whipsaws around VWAP line

- Lag in trend identification

- Noise in deviation bands

Kalman VWAP Benefits:

- Smooth yet responsive line

- Fewer false signals

- Optional momentum tracking

- Statistically optimized filtering

Alert Conditions

The indicator includes several pre-configured alert conditions:

- Bullish/Bearish VWAP crosses

- Upper/Lower band touches

- High divergence warnings

- Velocity shifts (if enabled)

---

This open-source indicator is provided as-is for educational and trading purposes. No guarantees are made regarding trading performance. Users should conduct their own testing and validation before using in live trading.

Kalman Adaptive Score Overlay [BackQuant]Kalman Adaptive Score Overlay

A powerful indicator that uses adaptive scoring to assess market conditions and trends, utilizing advanced filtering techniques to smooth price data, enhance trend-following precision, and predict future price movements based on past data. It is ideal for traders who need a dynamic and responsive trend analysis tool that adjusts to market fluctuations.

What is Adaptive Scoring?

Adaptive scoring is a technique that adjusts the weight or importance of certain price movements over time based on an ongoing assessment of market behavior. This indicator uses dynamic scoring to assess the strength and direction of price movements, providing insight into whether a trend is likely to continue or reverse. The score is recalculated continuously to reflect the most up-to-date market conditions, offering a responsive approach to trend-following.

How It Works

The core of this indicator is built on advanced filtering methods that smooth price data, adjusting the response to recent price changes. The filtering mechanism incorporates a Kalman filter to reduce noise and improve the accuracy of price signals. Combined with adaptive scoring, this creates a robust framework that automatically adjusts to both short-term fluctuations and long-term trends.

The indicator also uses a dynamic trend-following component that updates its analysis based on the direction of the market, with the option to visualize it through colored candles. When a strong trend is identified, the candles are painted to reflect the prevailing trend, helping traders quickly identify whether the market is in a bullish or bearish state.

Why Adaptive Scoring Is Important

Dynamic Response: Adaptive scoring allows the indicator to respond to changing market conditions. By adjusting its sensitivity to price fluctuations, it ensures that trends are captured accurately, without being overly influenced by short-term noise.

Trend Precision: By combining Kalman filtering with adaptive scoring, the indicator offers a precise and smooth trend-following mechanism. It helps traders stay aligned with the market direction and avoid false signals.

Versatility: The indicator works across multiple timeframes, making it adaptable to different trading strategies, from scalping to long-term trend-following.

Confidence in Market Moves: The adaptive scoring component provides traders with confidence in the strength of the trend, helping them determine when to enter or exit positions with greater certainty.

How Traders Use It

Trend-Following Strategy: Traders can use this indicator to confirm trends and refine their entries and exits. The colored candles and adaptive scoring offer a visual cue of trend strength and direction, making it easier to follow the prevailing market movement.

Multi-Timeframe Analysis: The script supports multi-timeframe analysis, allowing traders to analyze trends and scores across different timeframes (e.g., 1m, 5m, 15m, 30m, 1h, 4h, 12h). This is useful for traders who want to confirm trends on both short and long-term charts before making a trade.

Refining Entry Points: By utilizing the adaptive scoring, traders can identify potential entry points where the score indicates a high probability of trend continuation. Higher scores signal stronger trends, guiding decision-making.

Managing Risk: Traders can use the adaptive scoring system to assess trend stability and adjust their risk management strategies accordingly. For example, higher confidence in the trend allows for larger positions, while lower confidence may require smaller, more cautious trades.

Key Features and Benefits

Kalman Filter for Noise Reduction: The Kalman filter helps to smooth out market noise and allows for a clearer understanding of the underlying price movements. This is particularly useful in volatile markets where short-term fluctuations can cloud trend analysis.

Adaptive Scoring for Flexibility: Adaptive scoring ensures that the indicator remains responsive to changing market conditions. It automatically adjusts to the strength of price movements, enabling better detection of trends and reversals.

Visual Trend Signals: The indicator provides visual signals through candle coloring, making it easier to identify whether the market is in a bullish, neutral, or bearish phase.

Multi-Timeframe Display: The indicator’s multi-timeframe feature allows traders to see the trend and adaptive score on different timeframes simultaneously, providing a comprehensive view of the market.

Customizable Settings: Traders can customize the indicator’s settings, such as the filter parameters, scoring thresholds, and visualization options, tailoring it to their specific trading style and strategy.

Why This is Important for Traders

Improved Decision Making: The adaptive nature of the scoring system allows traders to make more informed decisions based on real-time market data, without being influenced by past volatility.

Market Clarity: By smoothing out price movements and scoring trends adaptively, the indicator provides a clearer picture of market behavior, which is essential for effective trend-following and timing entries and exits.

Increased Confidence in Signals: Adaptive scoring ensures that signals are based on the current market structure, reducing the likelihood of false positives. This boosts traders' confidence when acting on signals.

Conclusion

The Kalman Adaptive Score Overlay offers a dynamic and responsive trend-following tool that integrates Kalman filtering with adaptive scoring. By adjusting to market fluctuations in real time, it allows traders to identify and follow trends with greater precision. Whether you are trading on short or long timeframes, this tool helps you stay aligned with market momentum, ensuring that your entries and exits are based on the most up-to-date and reliable data available.

Kalman VWAP Filter [BackQuant]Kalman VWAP Filter

A precision-engineered price estimator that fuses Kalman filtering with the Volume-Weighted Average Price (VWAP) to create a smooth, adaptive representation of fair value. This hybrid model intelligently balances responsiveness and stability, tracking trend shifts with minimal noise while maintaining a statistically grounded link to volume distribution.

If you would like to see my original Kalman Filter, please find it here:

Concept overview

The Kalman VWAP Filter is built on two core ideas from quantitative finance and control theory:

Kalman filtering — a recursive Bayesian estimator used to infer the true underlying state of a noisy system (in this case, fair price).

VWAP anchoring — a dynamic reference that weights price by traded volume, representing where the majority of transactions have occurred.

By merging these concepts, the filter produces a line that behaves like a "smart moving average": smooth when noise is high, fast when markets trend, and self-adjusting based on both market structure and user-defined noise parameters.

How it works

Measurement blend : Combines the chosen Price Source (e.g., close or hlc3) with either a Session VWAP or a Rolling VWAP baseline. The VWAP Weight input controls how much the filter trusts traded volume versus price movement.

Kalman recursion : Each bar updates an internal "state estimate" using the Kalman gain, which determines how much to trust new observations vs. the prior state.

Noise parameters :

Process Noise controls agility — higher values make the filter more responsive but also more volatile.

Measurement Noise controls smoothness — higher values make it steadier but slower to adapt.

Filter order (N) : Defines how many parallel state estimates are used. Larger orders yield smoother output by layering multiple one-dimensional Kalman passes.

Final output : A refined price trajectory that captures VWAP-adjusted fair value while dynamically adjusting to real-time volatility and order flow.

Why this matters

Most smoothing techniques (EMA, SMA, Hull) trade off lag for smoothness. Kalman filtering, however, adaptively rebalances that tradeoff each bar using probabilistic weighting, allowing it to follow market state changes more efficiently. Anchoring it to VWAP integrates microstructure context — capturing where liquidity truly lies rather than only where price moves.

Use cases

Trend tracking : Color-coded candle painting highlights shifts in slope direction, revealing early trend transitions.

Fair value mapping : The line represents a continuously updated equilibrium price between raw price action and VWAP flow.

Adaptive moving average replacement : Outperforms static MAs in variable volatility regimes by self-adjusting smoothness.

Execution & reversion logic : When price diverges from the Kalman VWAP, it may indicate short-term imbalance or overextension relative to volume-adjusted fair value.

Cross-signal framework : Use with standard VWAP or other filters to identify convergence or divergence between liquidity-weighted and state-estimated prices.

Parameter guidance

Process Noise : 0.01–0.05 for swing traders, 0.1–0.2 for intraday scalping.

Measurement Noise : 2–5 for normal use, 8+ for very smooth tracking.

VWAP Weight : 0.2–0.4 balances both price and VWAP influence; 1.0 locks output directly to VWAP dynamics.

Filter Order (N) : 3–5 for reactive short-term filters; 8–10 for smoother institutional-style baselines.

Interpretation

When price > Kalman VWAP and slope is positive → bullish pressure; buyers dominate above fair value.

When price < Kalman VWAP and slope is negative → bearish pressure; sellers dominate below fair value.

Convergence of price and Kalman VWAP often signals equilibrium; strong divergence suggests imbalance.

Crosses between Kalman VWAP and the base VWAP can hint at shifts in short-term vs. long-term liquidity control.

Summary

The Kalman VWAP Filter blends statistical estimation with market microstructure awareness, offering a refined alternative to static smoothing indicators. It adapts in real time to volatility and order flow, helping traders visualize balance, transition, and momentum through a lens of probabilistic fair value rather than simple price averaging.

Kalman Adjusted Average True Range [BackQuant]Kalman Adjusted Average True Range

A volatility-aware trend baseline that fuses a Kalman price estimate with ATR “rails” to create a smooth, adaptive guide for entries, exits, and trailing risk.

Built on my original Kalman

This indicator is based on my original Kalman Price Filter:

That core smoother is used here to estimate the “true” price path, then blended with ATR to control step size and react proportionally to market noise.

What it plots

Kalman ATR Line the main baseline that turns up/down with the filtered trend.

Optional Moving Average of the Kalman ATR a secondary line for confluence (SMA/Hull/EMA/WMA/DEMA/RMA/LINREG/ALMA).

Candle Coloring (optional) paint bars by the baseline’s current direction.

Why combine Kalman + ATR?

Kalman reduces measurement noise and produces a stable path without the lag of heavy MAs.

ATR rails scale the baseline’s step to current volatility, so it’s calm in chop and more responsive in expansion.

The result is a single, intelligible line you can trade around: slope-up = constructive; slope-down = caution.

How it works (plain English)

Each bar, the Kalman filter updates an internal state (tunable via Process Noise , Measurement Noise , and Filter Order ) to estimate the underlying price.

An ATR band (Period × Factor) defines the allowed per-bar adjustment. The baseline cannot “jump” beyond those rails in one step.

A direction flip is detected when the baseline’s slope changes sign (upturn/downturn), and alerts are provided for both.

Typical uses

Trend confirmation Trade in the baseline’s direction; avoid fading a firmly rising/falling line.

Pullback timing Look for entries when price mean-reverts toward a rising baseline (or exits on tags of a falling one).

Trailing risk Use the baseline as a dynamic guide; many traders set stops a small buffer beyond it (e.g., a fraction of ATR).

Confluence Enable the MA overlay of the Kalman ATR; alignment (baseline above its MA and rising) supports continuation.

Inputs & what they do

Calculation

Kalman Price Source which price the filter tracks (Close by default).

Process Noise how quickly the filter can adapt. Higher = more responsive (but choppier).

Measurement Noise how much you distrust raw price. Higher = smoother (but slower to turn).

Filter Order (N) depth of the internal state array. Higher = slightly steadier behavior.

Kalman ATR

Period ATR lookback. Shorter = snappier; longer = steadier.

Factor scales the allowed step per bar. Larger factors permit faster drift; smaller factors clamp movement.

Confluence (optional)

MA Type & Period compute an MA on the Kalman ATR line , not on price.

Sigma (ALMA) if ALMA is selected, this input controls the curve’s shape. (Ignored for other MA types.)

Visuals

Plot Kalman ATR toggle the main line.

Paint Candles color bars by up/down slope.

Colors choose long/short hues.

Signals & alerts

Trend Up baseline turns upward (slope crosses above 0).

Alert: “Kalman ATR Trend Up”

Trend Down baseline turns downward (slope crosses below 0).

Alert: “Kalman ATR Trend Down”

These are state flips , not “price crossovers,” so you avoid many one-bar head-fakes.

How to start (fast presets)

Swing (daily/4H) ATR Period 7–14, Factor 0.5–0.8, Process Noise 0.02–0.05, Measurement Noise 2–4, N = 3–5.

Intraday (5–15m) ATR Period 5–7, Factor 0.6–1.0, Process Noise 0.05–0.10, Measurement Noise 2–3, N = 3–5.

Slow assets / FX raise Measurement Noise or ATR Period for calmer lines; drop Factor if the baseline feels too jumpy.

Reading the line

Rising & curving upward momentum building; consider long bias until a clear downturn.

Flat & choppy regime uncertainty; many traders stand aside or tighten risk.

Falling & accelerating distribution lower; short bias until a clean upturn.

Practical playbook

Continuation entries After a Trend Up alert, wait for a minor pullback toward the baseline; enter on evidence the line keeps rising.

Exit/reduce If long and the baseline flattens then turns down, trim or exit; reverse logic for shorts.

Filters Add a higher-timeframe check (e.g., only take longs when the daily Kalman ATR is rising).

Stops Place stops just beyond the baseline (e.g., baseline − x% ATR for longs) to avoid “tag & reverse” noise.

Notes

This is a guide to state and momentum, not a guarantee. Combine with your process (structure, volume, time-of-day) for decisions.

Settings are asset/timeframe dependent; start with the presets and nudge Process/Measurement Noise until the baseline “feels right” for your market.

Summary

Kalman ATR takes the noise-reduction of a Kalman price estimate and couples it with volatility-scaled movement to produce a clean, adaptive baseline. If you liked the original Kalman Price Filter (), this is its trend-trading cousin purpose-built for cleaner state flips, intuitive trailing, and confluence with your existing

Algorithmic Kalman Filter [CRYPTIK1]Price action is chaos. Markets are driven by high-frequency algorithms, emotional reactions, and raw speculation, creating a constant stream of noise that obscures the true underlying trend. A simple moving average is too slow, too primitive to navigate this environment effectively. It lags, it gets chopped up, and it fails when you need it most.

This script implements an Algorithmic Kalman Filter (AKF), a sophisticated signal processing algorithm adapted from aerospace and robotic guidance systems. Its purpose is singular: to strip away market noise and provide a hyper-adaptive, self-correcting estimate of an asset's true trajectory.

The Concept: An Adaptive Intelligence

Unlike a moving average that mindlessly averages past data, the Kalman Filter operates on a two-step principle: Predict and Update.

Predict: On each new bar, the filter makes a prediction of the true price based on its previous state.

Update: It then measures the error between its prediction and the actual closing price. It uses this error to intelligently correct its estimate, learning from its mistakes in real-time.

The result is a flawlessly smooth line that adapts to volatility. It remains stable during chop and reacts swiftly to new trends, giving you a crystal-clear view of the market's real intention.

How to Wield the Filter: The Core Settings

The power of the AKF lies in its two tuning parameters, which allow you to calibrate the filter's "brain" to any asset or timeframe.

Process Noise (Q) - Responsiveness: This controls how much you expect the true trend to change.

A higher Q value makes the filter more sensitive and responsive to recent price action. Use this for highly volatile assets or lower timeframes.

A lower Q value makes the filter smoother and more stable, trusting that the underlying trend is slow-moving. Use this for higher timeframes or ranging markets.

Measurement Noise (R) - Smoothness: This controls how much you trust the incoming price data.

A higher R value tells the filter that the price is extremely noisy and to be more skeptical. This results in a much smoother, slower-moving line.

A lower R value tells the filter to trust the price data more, resulting in a line that tracks price more closely.

The interaction between Q and R is what gives the filter its power. The default settings provide a solid baseline, but a true operator will fine-tune these to perfectly match the rhythm of their chosen market.

Tactical Application

The AKF is not just a line; it's a complete framework for viewing the market.

Trend Identification: The primary signal. The filter's color code provides an unambiguous definition of the trend. Teal for an uptrend, Pink for a downtrend. No more guesswork.

Dynamic Support & Resistance: The filter itself acts as a dynamic level. Watch for price to pull back and find support on a rising (Teal) filter in an uptrend, or to be rejected by a falling (Pink) filter in a downtrend.

A Higher-Order Filter: Use the AKF's trend state to filter signals from your primary strategy. For example, only take long signals when the AKF is Teal. This single rule can dramatically reduce noise and eliminate low-probability trades.

This is a professional-grade tool for traders who are serious about gaining a statistical edge. Ditch the lagging averages. Extract the signal from the noise.

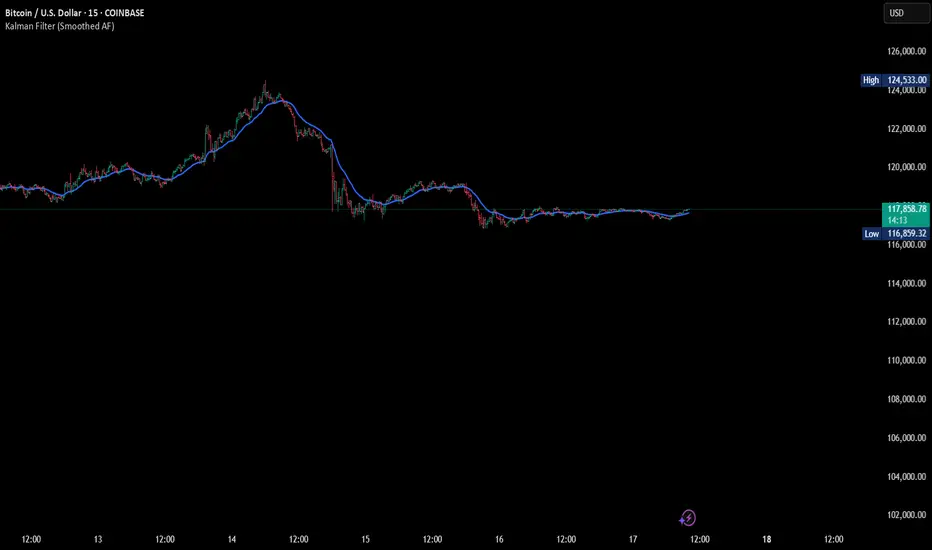

Kalman Filter (Smoothed)The Kalman Filter is a recursive statistical algorithm that smooths noisy price data while adapting dynamically to new information. Unlike simple moving averages or EMAs, it minimizes lag by balancing measurement noise (R) and process noise (Q), giving traders a clean, adaptive estimate of true price action.

🔹 Core Features

Real-time recursive estimation

Adjustable noise parameters (R = sensitivity to price, Q = smoothness vs. responsiveness)

Reduces market noise without heavy lag

Overlay on chart for direct comparison with raw price

🔹 Trading Applications

Smoother trend visualization compared to traditional MAs

Spotting true direction during volatile/sideways markets

Filtering out market “whipsaws” for cleaner signals

Building blocks for advanced quant/trading models

⚠️ Note: The Kalman Filter is a state-space model; it doesn’t predict future price, but smooths past and present data into a more reliable signal.

TradersAID - Adaptive Smoothing Velocity ColoringTradersAID – Adaptive Smoothing Velocity Coloring

1. Overview

TradersAID – Adaptive Smoothing Velocity Coloring is a momentum visualization tool designed to highlight bullish or bearish pressure directly on price bars — helping you intuitively read directional strength and velocity shifts in any market or timeframe.

Using a Kalman-inspired estimation framework originally developed for aerospace and autonomous navigation, this tool analyzes the velocity of price movement and assigns a contextual candle color — offering a clean and readable way to interpret short-term flow.

Whether you’re navigating ranges or watching for trend continuation, this visualization simplifies complex data into actionable visual rhythm.

2. What It Does

Instead of measuring only price, the script focuses on price velocity — the rate of change over time. It computes this through a proprietary estimator that continuously adapts to volatility and momentum shifts.

The output is color-coded candles that reflect velocity dynamics:

• Green shades represent bullish acceleration

• Red shades reflect bearish velocity

• Neutral tones indicate fading momentum or transition phases

This allows you to quickly assess market tone:

• In strong trends: Watch for fading momentum (weaker colors)

• In ranges: Spot subtle shifts that hint at upcoming breakout direction

• Near potential reversals: Diverging velocity and price can stand out at a glance

3. How to Use It

• Momentum Insight:

Use color intensity to judge whether the current move is gaining or losing strength.

• Breakout Anticipation:

In sideways markets, shifting colors within the range can help anticipate which side may take control next.

• Divergence Reading:

Look for double tops or bottoms where price holds but velocity changes — often a hint that the move is maturing.

• Visual Confirmation Layer:

Combine with structural tools (like TradersAID Warning Dots or Trend Bands) to add a layer of momentum awareness.

4. Key Features

• Adaptive Velocity Model: Kalman-filter-like algorithm continuously tracks price velocity

• Gradient Candle Coloring: Smooth scale from deep red (strong bearish) to deep green (strong bullish)

• Flexible Sensitivity Modes:

o Slow – smoothest interpretation

o Regular – balanced tone

o Fast – more responsive

• RSI Normalization: Translates raw velocity into a familiar oscillator scale

• Full Overlay Integration: Candle coloring works seamlessly with other studies on the same chart

5. Technical Basis (Why It’s Closed Source)

The tool is built on a proprietary Unscented Kalman Filter implementation that estimates both price and its velocity simultaneously.

This advanced approach is rare in retail tools, drawing from real-time estimation techniques used in robotics and aerospace applications.

While the source remains closed to protect the performance logic and smoothing implementation, the core concepts — adaptive filtering, velocity-based analysis, and visual gradient output — are fully explained here for transparency and compliant understanding.

6. Settings

• Sensitivity Modes: Fast / Regular / Slow

• RSI Length: Adjustable to control the smoothness of velocity normalization

• Color Theme: Intuitive gradient from red (bearish) to green (bullish)

• Compatible Timeframes: Designed to work across all timeframes — no restriction

7. Disclaimer

This tool is for educational and informational purposes only. It does not offer financial advice, predict outcomes, or generate trading signals. Always use in conjunction with your own analysis and supporting systems.

Quantitative Breakout Bands (AIBitcoinTrend)Quantitative Breakout Bands (AIBitcoinTrend) is an advanced indicator designed to adapt to dynamic market conditions by utilizing a Kalman filter for real-time data analysis and trend detection. This innovative tool empowers traders to identify price breakouts, evaluate trends, and refine their trading strategies with precision.

👽 What Are Quantitative Breakout Bands, and Why Are They Unique?

Quantitative Breakout Bands combine advanced filtering techniques (Kalman Filters) with statistical measures such as mean absolute error (MAE) to create adaptive price bands. These bands adjust to market conditions dynamically, providing insights into volatility, trend strength, and breakout opportunities.

What sets this indicator apart is its ability to incorporate both position (price) and velocity (rate of price change) into its calculations, making it highly responsive yet smooth. This dual consideration ensures traders get reliable signals without excessive lag or noise.

👽 The Math Behind the Indicator

👾 Kalman Filter Estimation:

At the core of the indicator is the Kalman Filter, a recursive algorithm used to predict the next state of a system based on past observations. It incorporates two primary elements:

State Prediction: The indicator predicts future price (position) and velocity based on previous values.

Error Covariance Adjustment: The process and measurement noise parameters refine the prediction's accuracy by balancing smoothness and responsiveness.

👾 Breakout Bands Calculation:

The breakout bands are derived from the mean absolute error (MAE) of price deviations relative to the filtered trendline:

float upperBand = kalmanPrice + bandMultiplier * mae

float lowerBand = kalmanPrice - bandMultiplier * mae

The multiplier allows traders to adjust the sensitivity of the bands to market volatility.

👾 Slope-Based Trend Detection:

A weighted slope calculation measures the gradient of the filtered price over a configurable window. This slope determines whether the market is trending bullish, bearish, or neutral.

👾 Trailing Stop Mechanism:

The trailing stop employs the Average True Range (ATR) to calculate dynamic stop levels. This ensures positions are protected during volatile moves while minimizing premature exits.

👽 How It Adapts to Price Movements

Dynamic Noise Calibration: By adjusting process and measurement noise inputs, the indicator balances smoothness (to reduce noise) with responsiveness (to adapt to sharp price changes).

Trend Responsiveness: The Kalman Filter ensures that trend changes are quickly identified, while the slope calculation adds confirmation.

Volatility Sensitivity: The MAE-based bands expand and contract in response to changes in market volatility, making them ideal for breakout detection.

👽 How Traders Can Use the Indicator

👾 Breakout Detection:

Bullish Breakouts: When the price moves above the upper band, it signals a potential upward breakout.

Bearish Breakouts: When the price moves below the lower band, it signals a potential downward breakout.

The trailing stop feature offers a dynamic way to lock in profits or minimize losses during trending moves.

👾 Trend Confirmation:

The color-coded Kalman line and slope provide visual cues:

Bullish Trend: Positive slope, green line.

Bearish Trend: Negative slope, red line.

👽 Why It’s Useful for Traders

Dynamic and Adaptive: The indicator adjusts to changing market conditions, ensuring relevance across timeframes and asset classes.

Noise Reduction: The Kalman Filter smooths price data, eliminating false signals caused by short-term noise.

Comprehensive Insights: By combining breakout detection, trend analysis, and risk management, it offers a holistic trading tool.

👽 Indicator Settings

Process Noise (Position & Velocity): Adjusts filter responsiveness to price changes.

Measurement Noise: Defines expected price noise for smoother trend detection.

Slope Window: Configures the lookback for slope calculation.

Lookback Period for MAE: Defines the sensitivity of the bands to volatility.

Band Multiplier: Controls the band width.

ATR Multiplier: Adjusts the sensitivity of the trailing stop.

Line Width: Customizes the appearance of the trailing stop line.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

Kalman Step Signals [AlgoAlpha]Take your trading to the next level with the Kalman Step Signals indicator by AlgoAlpha! This advanced tool combines the power of Kalman Filtering and the Supertrend indicator, offering a unique perspective on market trends and price movements. Designed for traders who seek clarity and precision in identifying trend shifts and potential trade entries, this indicator is packed with customizable features to suit your trading style.

Key Features

🔍 Kalman Filter Smoothing : Dynamically smooths price data with user-defined parameters for Alpha, Beta, and Period, optimizing responsiveness and trend clarity.

📊 Supertrend Overlay : Incorporates a classic Supertrend indicator to provide clear visual cues for trend direction and potential reversals.

🎨 Customizable Appearance : Adjust colors for bullish and bearish trends, along with optional exit bands for more nuanced analysis.

🔔 Smart Alerts : Detect key moments like trend changes or rejection entries for timely trading decisions.

📈 Advanced Visualization : Includes optional entry signals, exit bands, and rejection markers to pinpoint optimal trading opportunities.

How to Use

Add the Indicator : Add the script to your TradingView favorites. Customize inputs like Kalman parameters (Alpha, Beta, Period) and Supertrend settings (Factor, ATR Period) based on your trading strategy.

Interpret the Signals : Watch for trend direction changes using Supertrend lines and directional markers. Utilize rejection entries to identify price rejections at trendlines for precision entry points.

Set Alerts : Enable the built-in alert conditions for trend changes or rejection entries to act swiftly on trading opportunities without constant chart monitoring.

How It Works

The indicator leverages a Kalman Filter to smooth raw price data, balancing responsiveness and noise reduction using user-controlled parameters. This refined price data is then fed into a Supertrend calculation, combining ATR-based volatility analysis with dynamic upper and lower bands. The result is a clear and reliable trend-detection system. Additionally, it features rejection markers for bullish and bearish reversals when prices reject the trendline, along with exit bands to visualize potential price targets. The integration of customizable alerts ensures traders never miss critical market moves.

Add the Kalman Step Signals to your TradingView charts today and enjoy a smarter, more efficient trading experience! 🚀🌟

Kalman Filter Oscillator v4The Kalman Filter Oscillator v4 is an advanced tool designed to help traders and investors identify trends more effectively while reducing the impact of market noise. As the latest iteration in its development, this version integrates improvements that make it more adaptive and precise, catering to the challenges of today’s financial markets.

This indicator operates on the principle of the Kalman filter, a well-regarded mathematical approach used for estimating the state of a dynamic system. By filtering out random fluctuations, it smooths price data to provide clearer insights into underlying trends. Unlike traditional methods such as moving averages, which often lag and can miss rapid shifts, the Kalman Filter Oscillator is reactive in real time, making it particularly suited for dynamic markets.

Version v4 builds on earlier versions by offering a refined combination of short-term and long-term trend analysis. Through adjustable parameters, traders can balance sensitivity to immediate price changes with a broader perspective of the market direction. Additionally, the oscillator incorporates a unique feature that tracks a price’s position relative to its recent highs and lows, which enhances its ability to pinpoint potential turning points or key market conditions.

The indicator’s value lies in its adaptability and practicality. Traders can use it to confirm trends, identify overbought or oversold conditions, or smooth out erratic price movements, reducing the likelihood of false signals. By presenting information in a clear and actionable format, it allows users to make better-informed decisions with greater confidence.

As of late 2024, the Kalman Filter Oscillator v4 represents a sophisticated yet user-friendly advancement in trend analysis. While not a one-size-fits-all solution, it serves as a valuable component in a trader’s toolkit, complementing other strategies and enhancing overall market understanding.

Adaptive Kalman filter - Trend Strength Oscillator (Zeiierman)█ Overview

The Adaptive Kalman Filter - Trend Strength Oscillator by Zeiierman is a sophisticated trend-following indicator that uses advanced mathematical techniques, including vector and matrix operations, to decompose price movements into trend and oscillatory components. Unlike standard indicators, this model assumes that price is driven by two latent (unobservable) factors: a long-term trend and localized oscillations around that trend. Through a dynamic "predict and update" process, the Kalman Filter leverages vectors to adaptively separate these components, extracting a clearer view of market direction and strength.

█ How It Works

This indicator operates on a trend + local change Kalman Filter model. It assumes that price movements consist of two underlying components: a core trend and an oscillatory term, representing smaller price fluctuations around that trend. The Kalman Filter adaptively separates these components by observing the price series over time and performing real-time updates as new data arrives.

Predict and Update Procedure: The Kalman Filter uses an adaptive predict-update cycle to estimate both components. This cycle allows the filter to adjust dynamically as the market evolves, providing a smooth yet responsive signal. The trend component extracted from this process is plotted directly, giving a clear view of the prevailing direction. The oscillatory component indicates the tendency or strength of the trend, reflected in the green/red coloration of the oscillator line.

Trend Strength Calculation: Trend strength is calculated by comparing the current oscillatory value against a configurable number of past values.

█ Three Kalman filter Models

This indicator offers three distinct Kalman filter models, each designed to handle different market conditions:

Standard Model: This is a conventional Kalman Filter, balancing responsiveness and smoothness. It works well across general market conditions.

Volume-Adjusted Model: In this model, the filter’s measurement noise automatically adjusts based on trading volume. Higher volumes indicate more informative price movements, which the filter treats with higher confidence. Conversely, low-volume movements are treated as less informative, adding robustness during low-activity periods.

Parkinson-Adjusted Model: This model adjusts measurement noise based on price volatility. It uses the price range (high-low) to determine the filter’s sensitivity, making it ideal for handling markets with frequent gaps or spikes. The model responds with higher confidence in low-volatility periods and adapts to high-volatility scenarios by treating them with more caution.

█ How to Use

Trend Detection: The oscillator oscillates around zero, with positive values indicating a bullish trend and negative values indicating a bearish trend. The further the oscillator moves from zero, the stronger the trend. The Kalman filter trend line on the chart can be used in conjunction with the oscillator to determine the market's trend direction.

Trend Reversals: The blue areas in the oscillator suggest potential trend reversals, helping traders identify emerging market shifts. These areas can also indicate a potential pullback within the prevailing trend.

Overbought/Oversold: The thresholds, such as 70 and -70, help identify extreme conditions. When the oscillator reaches these levels, it suggests that the trend may be overextended, possibly signaling an upcoming reversal.

█ Settings

Process Noise 1: Controls the primary level of uncertainty in the Kalman filter model. Higher values make the filter more responsive to recent price changes, but may also increase susceptibility to random noise.

Process Noise 2: This secondary noise setting works with Process Noise 1 to adjust the model's adaptability. Together, these settings manage the uncertainty in the filter's internal model, allowing for finely-tuned adjustments to smoothness versus responsiveness.

Measurement Noise: Sets the uncertainty in the observed price data. Increasing this value makes the filter rely more on historical data, resulting in smoother but less reactive filtering. Lower values make the filter more responsive but potentially more prone to noise.

O sc Smoothness: Controls the level of smoothing applied to the trend strength oscillator. Higher values result in a smoother oscillator, which may cause slight delays in response. Lower values make the oscillator more reactive to trend changes, useful for capturing quick reversals or volatility within the trend.

Kalman Filter Model: Choose between Standard, Volume-Adjusted, and Parkinson-Adjusted models. Each model adapts the Kalman filter for specific conditions, whether balancing general market data, adjusting based on volume, or refining based on volatility.

Trend Lookback: Defines how far back to look when calculating the trend strength, which impacts the indicator's sensitivity to changes in trend strength. Shorter values make the oscillator more reactive to recent trends, while longer values provide a smoother reading.

Strength Smoothness: Adjusts the level of smoothing applied to the trend strength oscillator. Higher values create a more gradual response, while lower values make the oscillator more sensitive to recent changes.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Kalman Based VWAP [EdgeTerminal]Kalman VWAP is a different take on volume-weighted average price (VWAP) indicator where we enhance the results with Kalman filtering and dynamic wave visualization for a more smooth and improved trend identification and volatility analysis.

A little bit about Kalman Filter:

Kalman filtering (also known as linear quadratic estimation) is an algorithm that uses a series of measurements observed over time, including statistical noise and other inaccuracies, to produce estimates of unknown variables that tend to be more accurate than those based on a single measurement, by estimating a joint probability distribution over the variables for each time-step. The filter is constructed as a mean squared error minimiser, but an alternative derivation of the filter is also provided showing how the filter relates to maximum likelihood statistics

This indicator combines:

Volume-Weighted Average Price (VWAP) for institutional price levels

Kalman filtering for noise reduction and trend smoothing

Dynamic wave visualization for volatility zones

This creates a robust indicator that helps traders identify trends, support/resistance zones, and potential reversal points with high precision.

What makes this even more special is the fact that we use open price as a data source instead of usual close price. This allows you to tune the indicator more accurately when back testing it and generally get results that are closer to real time market data.

The math:

In case if you're interested in the math of this indicator, the indicator employs a state-space Kalman filter model:

State Equation: x_t = x_{t-1} + w_t

Measurement Equation: z_t = x_t + v_t

x_t is the filtered VWAP state

w_t is process noise ~ N(0, Q)

v_t is measurement noise ~ N(0, R)

z_t is the traditional VWAP measurement

The Kalman filter recursively updates through:

Prediction: x̂_t|t-1 = x̂_{t-1}

Update: x̂_t = x̂_t|t-1 + K_t(z_t - x̂_t|t-1)

Where K_t is the Kalman gain, optimally balancing between prediction and measurement.

Input Parameters

Measurement Noise: Controls signal smoothing (0.0001 to 1.0)

Process Noise: Adjusts trend responsiveness (0.0001 to 1.0)

Wave Size: Multiplier for volatility bands (0.1 to 5.0)

Trend Lookback: Period for trend determination (1 to 100)

Bull/Bear Colors: Customizable color schemes

Application:

I recommend using this along other indicators. This is best used for assets that don't have a close time, such as BTC but can be used with anything as long as the data is there.

With default settings, this works better for swing trades but you can adjust it for day trading as well, by adjusting the lookback and also process noise.

Kalman For Loop [BackQuant]Kalman For Loop

Introducing BackQuant's Kalman For Loop (Kalman FL) — a highly adaptive trading indicator that uses a Kalman filter to smooth price data and generate actionable long and short signals. This advanced indicator is designed to help traders identify trends, filter out market noise, and optimize their entry and exit points with precision. Let’s explore how this indicator works, its key features, and how it can enhance your trading strategies.

Core Concept: Kalman Filter

The Kalman Filter is a mathematical algorithm used to estimate the state of a system by filtering noisy data. It is widely used in areas such as control systems, signal processing, and time-series analysis. In the context of trading, a Kalman filter can be applied to price data to smooth out short-term fluctuations, providing a clearer view of the underlying trend.

Unlike moving averages, which use fixed weights to smooth data, the Kalman Filter adjusts its estimate dynamically based on the relationship between the process noise and the measurement noise. This makes the filter more adaptive to changing market conditions, providing more accurate trend detection without the lag associated with traditional smoothing techniques.

Please see the original Kalman Price Filter

In this script, the Kalman For Loop applies the Kalman filter to the price source (default set to the closing price) to generate a smoothed price series, which is then used to calculate signals.

Adaptive Smoothing with Process and Measurement Noise

Two key parameters govern the behavior of the Kalman filter:

Process Noise: This controls the extent to which the model allows for uncertainty in price changes. A lower process noise value will make the filter smoother but slower to react to price changes, while a higher value makes it more sensitive to recent price fluctuations.

Measurement Noise: This represents the uncertainty or "noise" in the observed price data. A higher measurement noise value gives the filter more leeway to ignore short-term fluctuations, focusing on the broader trend. Lowering the measurement noise makes the filter more responsive to minor changes in price.

These settings allow traders to fine-tune the Kalman filter’s sensitivity, adjusting it to match their preferred trading style or market conditions.

For-Loop Scoring Mechanism

The Kalman FL further enhances the effectiveness of the Kalman filter by using a for-loop scoring system. This mechanism evaluates the smoothed price over a range of periods (defined by the Calculation Start and Calculation End inputs), assigning a score based on whether the current filtered price is higher or lower than previous values.

Long Signals: A long signal is generated when the for-loop score surpasses the Long Threshold (default set at 20), indicating a strong upward trend. This helps traders identify potential buying opportunities.

Short Signals: A short signal is triggered when the score crosses below the Short Threshold (default set at -10), signaling a potential downtrend or selling opportunity.

These signals are plotted on the chart, giving traders a clear visual indication of when to enter long or short positions.

Customization and Visualization Options

The Kalman For Loop comes with a range of customization options to give traders full control over how the indicator operates and is displayed on the chart:

Kalman Price Source: Choose the price data used for the Kalman filter (default is the closing price), allowing you to apply the filter to other price points like open, high, or low.

Filter Order: Set the order of the Kalman filter (default is 5), controlling how far back the filter looks in its calculations.

Process and Measurement Noise: Fine-tune the sensitivity of the Kalman filter by adjusting these noise parameters.

Signal Line Width and Colors: Customize the appearance of the signal line and the colors used to indicate long and short conditions.

Threshold Lines: Toggle the display of the long and short threshold lines on the chart for better visual clarity.

The indicator also includes the option to color the candlesticks based on the current trend direction, allowing traders to quickly identify changes in market sentiment. In addition, a background color feature further highlights the overall trend by shading the background in green for long signals and red for short signals.

Trading Applications

The Kalman For Loop is a versatile tool that can be adapted to a variety of trading strategies and markets. Some of the primary use cases include:

Trend Following: The adaptive nature of the Kalman filter helps traders identify the start of new trends with greater precision. The for-loop scoring system quantifies the strength of the trend, making it easier to stay in trades for longer when the trend remains strong.

Mean Reversion: For traders looking to capitalize on short-term reversals, the Kalman filter's ability to smooth price data makes it easier to spot when price has deviated too far from its expected path, potentially signaling a reversal.

Noise Reduction: The Kalman filter excels at filtering out short-term price noise, allowing traders to focus on the broader market movements without being distracted by minor fluctuations.

Risk Management: By providing clear long and short signals based on filtered price data, the Kalman FL helps traders manage risk by entering positions only when the trend is well-defined, reducing the chances of false signals.

Alerts and Automation

To further assist traders, the Kalman For Loop includes built-in alert conditions that notify you when a long or short signal is generated. These alerts can be configured to trigger notifications, helping you stay on top of market movements without constantly monitoring the chart.

Final Thoughts

The Kalman For Loop is a powerful and adaptive trading indicator that combines the precision of the Kalman filter with a for-loop scoring mechanism to generate reliable long and short signals. Whether you’re a trend follower or a reversal trader, this indicator offers the flexibility and accuracy needed to navigate complex markets with confidence.

As always, it’s important to backtest the indicator and adjust the settings to fit your trading style and market conditions. No indicator is perfect, and the Kalman FL should be used alongside other tools and sound risk management practices for the best results.

Kalman Filter RoC with Adaptive Thresholds [BackQuant]Kalman Filter RoC with Adaptive Thresholds

Another Kalman Script !!

Please Find the Basic Kalman Here:

Overview and Purpose

The Kalman Filter RoC with Adaptive Thresholds is an advanced tool designed for traders seeking to refine their trend detection and momentum analysis. By combining the robustness of the Kalman filter with the Rate of Change (RoC) indicator, this tool offers a highly responsive and adaptive method to identify shifts in market trends. The inclusion of adaptive thresholding further enhances the indicator’s precision by dynamically adjusting to market volatility, providing traders with reliable entry and exit signals.

Kalman Filter Dynamics

The Kalman Filter is renowned for its ability to estimate the true state of a system amidst noisy data. In this indicator, the Kalman filter is applied to the price data to smooth out fluctuations and generate a more accurate representation of the underlying trend. This is particularly useful in volatile markets where noise can obscure the true direction of price movements. The Kalman filter adapts in real-time based on user-defined parameters, such as process noise and measurement noise, making it highly customizable for different market conditions.

Rate of Change (RoC) and Smoothing The Rate of Change (RoC) is a classic momentum indicator that measures the percentage change in price over a specific period. By integrating it with the Kalman-filtered price, the RoC becomes more responsive to genuine price trends while filtering out short-term noise. An optional smoothing feature using the ALMA (Arnaud Legoux Moving Average) further refines the signal, allowing traders to adjust the calculation length and smoothing factor (sigma) for even greater precision.

Adaptive Thresholds A key innovation in this indicator is the adaptive thresholding mechanism. Traditional RoC indicators rely on static thresholds to identify overbought or oversold conditions, but the Kalman Filter RoC adapts these thresholds dynamically. The adaptive thresholds are calculated based on the historical volatility of the filtered RoC values, allowing the indicator to adjust in response to changing market conditions. This feature reduces the risk of false signals in choppy or highly volatile markets.

Divergence Detection The Kalman Filter RoC also includes divergence detection, helping traders identify when the momentum of the RoC diverges from the price action. Divergences can often signal potential reversals or trend continuations, making them a valuable tool in any trader’s toolkit. Regular and hidden divergences are plotted directly on the chart, providing visual cues for traders to act upon.

Customization and Flexibility This indicator offers a wide range of customization options, making it suitable for various trading strategies and market conditions:

Process Noise & Measurement Noise: These parameters control how sensitive the Kalman filter is to price changes and help traders fine-tune the balance between noise reduction and signal responsiveness.

ALMA Smoothing: Traders can apply ALMA smoothing to the RoC signal to reduce short-term volatility and improve signal clarity.

Adaptive Threshold Calculation Period: The length of the lookback period for the adaptive thresholds can be adjusted, allowing traders to tailor the indicator to fit their specific trading style.

Practical Applications

Trend Detection: The Kalman-filtered RoC helps identify shifts in momentum, making it easier for traders to spot emerging trends early. The dynamic thresholding ensures that these signals are reliable, even in volatile markets.

Divergence Trading: Divergences between the RoC and price action are clear indicators of potential trend reversals. The visual plotting of divergences simplifies the process of identifying these opportunities.

Momentum Analysis: The combination of Kalman filtering and RoC provides a smoother, more accurate view of market momentum, helping traders stay on the right side of the market.

Conclusion

The Kalman Filter RoC is a powerful and adaptable tool that merges advanced filtering techniques with momentum analysis. Its real-time responsiveness and dynamic thresholding make it a highly effective indicator for identifying trends, managing risk, and capitalizing on divergence signals. Traders looking to enhance their trend-following or momentum strategies will find this indicator to be a valuable addition to their toolkit.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Kalman Hull RSI [BackQuant]Kalman Hull RSI

At its core, this indicator uses a Kalman filter of price, put inside of a hull moving average function (replacing the weighted moving averages) and then using that as a price source for the the RSI, very similar to the Kalman Hull Supertrend just processing price for a different indicator.

This also allows it to make it more adaptive to price and also sensitive to recent price action. This indicator is also mainly built for trend-following systems

PLEASE Read the following, knowing what an indicator does at its core before adding it into a system is pivotal. The core concepts can allow you to include it in a logical and sound manner.

1. What is a Kalman Filter

The Kalman Filter is an algorithm renowned for its efficiency in estimating the states of a linear dynamic system amidst noisy data. It excels in real-time data processing, making it indispensable in fields requiring precise and adaptive filtering, such as aerospace, robotics, and financial market analysis. By leveraging its predictive capabilities, traders can significantly enhance their market analysis, particularly in estimating price movements more accurately.

If you would like this on its own, with a more in-depth description please see our Kalman Price Filter.

OR our Kalman Hull Supertrend

2. Hull Moving Average (HMA) and Its Core Calculation

The Hull Moving Average (HMA) improves on traditional moving averages by combining the Weighted Moving Average's (WMA) smoothness and reduced lag. Its core calculation involves taking the WMA of the data set and doubling it, then subtracting the WMA of the full period, followed by applying another WMA on the result over the square root of the period's length. This methodology yields a smoother and more responsive moving average, particularly useful for identifying market trends more rapidly.

3. Combining Kalman Filter with HMA

The innovative combination of the Kalman Filter with the Hull Moving Average (KHMA) offers a unique approach to smoothing price data. By applying the Kalman Filter to the price source before its incorporation into the HMA formula, we enhance the adaptiveness and responsiveness of the moving average. This adaptive smoothing method reduces noise more effectively and adjusts more swiftly to price changes, providing traders with clearer signals for market entries or exits.

The calculation is like so:

KHMA(_src, _length) =>

f_kalman(2 * f_kalman(_src, _length / 2) - f_kalman(_src, _length), math.round(math.sqrt(_length)))

Use Case

The Kalman Hull RSI is particularly suited for traders who require a highly adaptive indicator that can respond to rapid market changes without the excessive noise associated with typical RSI calculations. It can be effectively used in markets with high volatility where traditional indicators might lag or produce misleading signals.

Application in a Trading System

The Kalman Hull RSI is versatile in application, suitable for:

Trend Identification: Quickly identify potential reversals or confirmations of existing trends.

Overbought/Oversold Conditions: Utilize the dynamic RSI thresholds to pinpoint potential entry and exit points, adapting to current market conditions.

Risk Management: Enhance trading strategies by integrating a more reliable measure of momentum, which can lead to improved stop-loss placements and exit strategies.

Core Calculations and Benefits

Dynamic State Estimation: By applying the Kalman Filter, the indicator continually adjusts its calculations based on incoming price data, providing a real-time, smoothed response to price movements.

Reduced Lag: The integration with HMA significantly reduces lag, offering quicker responses to price changes than traditional moving averages or RSI alone.

Increased Accuracy: The dual filtering effect minimizes the impact of price spikes and noise, leading to more accurate signaling for trades.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Kalman Volume Filter [ChartPrime]The "Kalman Volume Filter" , aims to provide insights into market volume dynamics by filtering out noise and identifying potential overbought or oversold conditions. Let's break down its components and functionality:

Settings:

Users can adjust various parameters to customize the indicator according to their preferences:

Volume Length: Defines the length of the volume period used in calculations.

Stabilization Coefficient (k): Determines the level of noise reduction in the signals.

Signal Line Length: Sets the length of the signal line used for identifying trends.