LowFinder_PyraMider_V2This strategy is a result of an exploration to experiment with other ways to detect lows / dips in the price movement, to try out alternative ways to exit and stop positions and a dive into risk management. It uses a combination of different indicators to detect and filter the potential lows and opens multiple positions to spread the risk and opportunities for unrealized losses or profits. This script combines code developed by fellow Tradingview community_members.

LowFinder

The lows in the price movement are detected by the Low finder script by RafaelZioni . It finds the potential lows based on the difference between RSI and EMA RSI. The MTF RSI formula is part of the MTFindicators library developed by Peter_O and is integrated in the Low finder code to give the option to use the RSI of higher timeframes. The sensitivity of the LowFinder is controlled by the MA length. When potential lows are detected, a Moving Average, a MTF Stochastic (based the the MTFindiicators by Peter_O) and the average price level filter out the weak lows. In the settings the minimal percentage needed for a low to be detected below the average price can be specified.

Order Sizing and Pyramiding

Pyramiding, or spreading multiple positions, is at the heart of this strategy and what makes it so powerful. The order size is calculated based on the max number of orders and portfolio percentage specified in the input settings. There are two order size modes. The ‘base’ mode uses the same base quantity for each order it opens, the ‘multiply’ mode multiplies the quantity with each order number. For example, when Long 3 is opened, the quantity is multiplied by 3. So, the more orders the bigger the consecutive order sizes. When using ‘multiply’ mode the sizes of the first orders are considerably lower to make up for the later bigger order sizes. There is an option to manually set a fixed order size but use this with caution as it bypasses all the risk calculations.

Stop Level, Take Profit, Trailing Stop

The one indicator that controls the exits is the Stop Level. When close crosses over the Stop Level, the complete position is closed and all orders are exited. The Stop Level is calculated based on the highest high given a specified candle lookback (settings). There is an option to deviate above this level with a specified percentage to tweak for better results. You can activate a Take Profit / Trailing Stop. When activated and close crosses the specified percentage, the Stop Level logic changes to a trailing stop to gain more profits. Another option is to use the percentage as a take profit, either when the stop level crosses over the take profit or close. With this option active, you can make this strategy more conservative. It is active by default.

And finally there is an option to Take Profit per open order. If hit, the separate orders close. In the current settings this option is not used as the percentage is 10%.

Stop Loss

I published an earlier version of this script a couple of weeks ago, but it got hidden by the moderators. Looking back, it makes sense because I didn’t pay any attention to risk management and save order sizing. This resulted in unrealistic results. So, in this script update I added a Stop Loss option. There are two modes. The ‘average price’ mode calculates the stop loss level based on a given percentage below the average price of the total position. The ‘equity’ mode calculates the stop loss level based on a given percentage of your equity you want to lose. By default, the ‘equity’ mode is active. By tweaking the percentage of the portfolio size and the stop loss equity mode, you can achieve a quite low risk strategy set up.

Variables in comments

To sent alerts to my exchange I use a webhook server. This works with a sending the information in the form of a comment. To be able to send messages with different quantities, a variable is added to the comment. This makes it possible to open different positions on the exchange with increasing quantities. To test this the quantities are printed in the comment and the quantities are switched off in the style settings.

This code is a result of a study and not intended for use as a worked out and full functioning strategy. Use it at your own risk. To make the code understandable for users that are not so much introduced into pine script (like me), every step in the code is commented to explain what it does. Hopefully it helps.

Enjoy!

震荡指标

VWAP+15EMA with RSIVWAP+EMA+RSI Strategy for the group MelléCasH

This strategy will enter a long position when the closing price is above both the VWAP and the 15 EMA, and the RSI is above the specified overbought level. It will exit the position when the price falls by the specified stop loss percentage, rises by the specified take profit percentage, or when the trailing stop loss (which trails the highest price achieved after the position was entered by the specified percentage) is hit. The VWAP, EMA, and RSI indicators are also plotted on the chart for reference.

MTF Diagonally Layered RSI - 1 minute Bitcoin Bot [wbburgin]This is a NON-REPAINTING multi-timeframe RSI strategy (long-only) that enters a trade only when two higher timeframes are oversold. I wrote it on BTC/USD for 1min, but the logic should work on other assets as well. It is diagonally layered to be profitable for when the asset is in a downtrend.

Diagonal layering refers to entry and exit conditions spread across different timeframes. Normally, indicators can become unprofitable because in downtrends, the overbought zones of the current timeframe are not reached. Rather, the overbought zones of the faster timeframes are reached first, and then a selloff occurs. Diagonally-layered strategies mitigate this by selling diagonally, that is, selling once the faster timeframe reaches overbought and buying once the slower timeframe reaches oversold.

Thus this strategy is diagonally layered down . I may create a separate script that alternates between diagonal-up and diagonal-down based off of overall trend, as in extended trend periods up this indicator may not flash as frequently. This can be visualized in a time series x timeframe chart as an "X" shape. Something to consider...

Let me know if you like this strategy. Feel free to alter the pyramiding entries, initial capital, and entry size, as well as commission regime. My strategies are designed to maximize average profit instead of flashing super frequently, as the fees will eat you up. Additionally, at the time of publication, all of my strategy scripts are intended to have profitable Sharpe and Sortino ratios.

Timeframes, RSI period, and oversold/overbought bounds are configurable.

Kitchen [ilovealgotrading]

OVERVIEW:

Kitchen is a strategy that aims to trade in the direction of the trend by using supertrend and stochRsi data by calculating at different time values.

IMPLEMENTATION DETAILS – SETTINGS:

First of all, let's understand the supertrend and stocrsi indicators.

How do you read and use Super Trend for trading ?

The price is often going upwards when it breaks the super trend line while keeping its position above the indication level.

When the market is in a bullish trend, the indicator becomes green. The indicator level will act as trendline support in such a scenario. The color of the indicator changes to red to indicate a negative trend once the price crosses the support line. The price uses the super trend level as a trendline resistance during a bearish move.

In our strategy, if our 1-hour and 4-hour supertrend lines show the up or down train in the same direction at the same time, we can assume that a train is forming here.

Why do I use the time of 1 hour and 4 hours ?

When I did a backtest from the past to the present, I discovered that the most accurate and consistent time zones are the 1 hour and 4 hour time zones.

By the way we can change our short term timeframe(1H) and long term timeframe(4H) from settings panel.

How do you read and use the Stoch-RSI Indicator?

This indicator analyzes price dynamics automatically to detect overbought and oversold locations.

The indicator includes:

- The primary line, which typically has values between 0 and 100;

- Two dynamic levels for overbought and oversold conditions.

IF our stoch-rsi indicator value has fallen below our lower boundary line, the oversold event has been observed in the price, if our stoch-rsi value breaks up our bottom line after becoming oversold, we think that the price will start the recovery phase.(The case is also true for the opposite.)

However, this does not always apply and we need additional approvals, Therefore, our 1H and 4H supertrrend indicator provides us with additional confirmation.

Buy Condition:

Our 1H(short term) and 4H(long term) supertrrend indicator, has given the buy signal(green line and yellow line), and if our stochrsi indicator has broken our oversold line up on the past 15 bars, the buy signal is formed here.

Sell Condition:

Our 1H(short term) and 4H(long term) supertrrend indicator, has given the sell signal(red line and orange line), and if our stochrsi indicator has broken our overbuy line down on the past 15 bars, the sell signal is formed here.

Stop Loss or Take Profit Conditions:

Exit Long Senerio:

All conditions are completed, the buy signal has arrived and we have entered a LONG trade, the 1-hour supertrend line follows the price rise(yellow line), if the price breaks below the 1-hour super trend line and a sell condition occurs for 1H timeframe for supertrend indcator, LONG trade will exit here.

Exit Short Senerio:

All conditions are completed, the Sell signal has arrived and we have entered a SHORT trade, the 1-hour supertrend line follows the price down(orange line), if the price breaks up the 1-hour super trend line and a buy condition occurs for 1H timeframe for supertrend indcator, SHORT trade will exit here.

What can you change in the settings panel?

1-We can set Start and End date for backtest and future alarms

2-We can set ATR length and Factor for supertrend indicator

3-We can set our short term and long term timeframe value

4-We can set StochRsi Up and Low limit to confirm buy and sell conditions

5-We can set stochrsi retroactive approval length

6-We can set stochrsi values or the length

7-We can set Dollar cost for per position

8- We can choose the direction of our positions, we can set only LONG, only SHORT or both directions.

9-IF you want to place automatic buy and sell orders with this strategy, you can paste your codes into the Long open-close or Short open-close message sections.

For example

IF you write your alert window this code {{strategy.order.alert_message}}.

When trigger Long signal you will get dynamically what you pasted here for Long Open Message

ALSO:

Please do not open trades without properly managing your risk and psychology!!!

If you have any ideas what to add to my work to add more sources or make calculations cooler, suggest in DM .

Mean Reversion and TrendfollowingTitle: Mean Reversion and Trendfollowing

Introduction:

This script presents a hybrid trading strategy that combines mean reversion and trend following techniques. The strategy aims to capitalize on short-term price corrections during a downtrend (mean reversion) as well as ride the momentum of a trending market (trend following). It uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

Key Features:

Combines mean reversion and trend following techniques

Utilizes 200-period SMA and 2-period RSI

Customizable starting date

Allows for enabling/disabling mean reversion or trend following modes

Adjustable position sizing for trend following and mean reversion

Script Description:

The script implements a trading strategy that combines mean reversion and trend following techniques. Users can enable or disable either of these techniques through the input options. The strategy uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

The mean reversion mode is active when the price is below the SMA200, while the trend following mode is active when the price is above the SMA200. The script generates buy signals when the RSI is below 20 (oversold) in mean reversion mode or when the price is above the SMA200 in trend following mode. The script generates sell signals when the RSI is above 80 (overbought) in mean reversion mode or when the price falls below 95% of the SMA200 in trend following mode.

Users can adjust the position sizing for both trend following and mean reversion modes using the input options.

To use this script on TradingView, follow these steps:

Open TradingView and load your preferred chart.

Click on the 'Pine Editor' tab located at the bottom of the screen.

Paste the provided script into the Pine Editor.

Click 'Add to Chart' to apply the strategy to your chart.

Please note that the past performance of any trading system or methodology is not necessarily indicative of future results. Always use proper risk management and consult a financial advisor before making any investment decisions.

------

The following is a summary of the underlying whitepaper (onlinelibrary.wiley.com) for this strategy:

This paper proposes a theory of securities market under- and overreactions based on two psychological biases: investor overconfidence about the precision of private information and biased self-attribution, which causes asymmetric shifts in investors' confidence as a function of their investment outcomes. The authors show that overconfidence implies negative long-lag autocorrelations, excess volatility, and public-event-based return predictability. Biased self-attribution adds positive short-lag autocorrelations (momentum), short-run earnings "drift," and negative correlation between future returns and long-term past stock market and accounting performance.

The paper explains that there is empirical evidence challenging the traditional view that securities are rationally priced to reflect all publicly available information. Some of these anomalies include event-based return predictability, short-term momentum, long-term reversal, high volatility of asset prices relative to fundamentals, and short-run post-earnings announcement stock price "drift."

The authors argue that investor overconfidence can lead to stock prices overreacting to private information signals and underreacting to public signals. This overreaction-correction pattern is consistent with long-run negative autocorrelation in stock returns, excess volatility, and further implications for volatility conditional on the type of signal. The market's tendency to over- or underreact to different types of information allows the authors to address the pattern that average announcement date returns in virtually all event studies are of the same sign as the average post-event abnormal returns.

Biased self-attribution implies short-run momentum and long-term reversals in security prices. The dynamic analysis based on biased self-attribution can also lead to a lag-dependent response to corporate events. Cash flow or earnings surprises at first tend to reinforce confidence, causing a same-direction average stock price trend. Later reversal of overreaction can lead to an opposing stock price trend.

The paper concludes by summarizing the findings, relating the analysis to the literature on exogenous noise trading, and discussing issues related to the survival of overconfident traders in financial markets.

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

Advanced VWAP_Pullback Strategy_Trend-Template QualifierGeneral Description and Unique Features of this Script

Introducing the Advanced VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends. Mark Minervini, a 2x US Investment Champion, developed the Trend-Template, which covers eight different and independent characteristics that can be adjusted and optimized in this trend-following strategy to ensure the best results. The strategy will only trigger buy-signals in case the optimized qualifiers are being met.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strategy

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably. You also have the option to make use of the trailing stop exit strategy.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from Jan 2020 until March 2023

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

- This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

- The combination of the Trend-Template and the RSI qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

- Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

JS-TechTrading: VWAP Momentum_Pullback StrategyGeneral Description and Unique Features of this Script

Introducing the VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available on TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strateg y

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

Fair Value Strategy - ekmllThis is a strategy using SPX's Fair Value derived from Net Liquidity.

The main difference between this one and calebsandfort's one is net liquidity values in this one are calculated in TradingView and doesn't need author's daily library updates to function.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: (WALCL - WTREGEN - RRPONTSYD)/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

I've optimized the parameters for SPX.

Soheil PKO's 5 min Hitman Scalp - 3MA + Laguerre RSI + ADX [Pt]Someone sent me this strategy found on YouTube. It is Soheil PKO's "The Best and Most Profitable Scalping Strategy" Best way to find out is to code it =)

This strategy uses Moving Average Ribbon, Laguerre RSI, and ADX. This script only displays the MA ribbon, you will need to add Laguerre RSI and ADX separately.

Long Entry Criteria:

- 16 EMA > 48 EMA > 200 SMA

- Laguerre RSI > 80

- ADX > 20

Long Exit Criterion:

- 16 EMA < 48 EMA

Short Entry Criteria:

- 16 EMA < 48 EMA < 200 SMA

- Laguerre RSI < 20

- ADX > 20

Short Exit Criterion:

- 16 EMA > 48 EMA

As mentioned in the video, risk management is very important, especially for scalping strategies. Therefore, I've added option for setting Stop Loss and Price Target in the options for you guys to play with.

All parameters are configurable.

Enjoy~~

Shorting when Bollinger Band Above Price with RSI (by Coinrule)The Bollinger Bands are among the most famous and widely used indicators. A Bollinger Band is a technical analysis tool defined by a set of trendlines plotted two standard deviations (positively and negatively) away from a simple moving average ( SMA ) of a security's price, but which can be adjusted to user preferences. They can suggest when an asset is oversold or overbought in the short term, thus providing the best time for buying and selling it.

The relative strength index ( RSI ) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of a security's recent price changes to evaluate overvalued or undervalued conditions in the price of that security. The RSI can do more than point to overbought and oversold securities. It can also indicate securities primed for a trend reversal or corrective pullback in price. It can signal when to buy and sell. Traditionally, an RSI reading of 70 or above indicates an overbought situation. A reading of 30 or below indicates an oversold condition.

The short order is placed on assets that present strong momentum when it's more likely that it is about to reverse. The rule strategy places and closes the order when the following conditions are met:

ENTRY

The closing price is greater than the upper standard deviation of the Bollinger Bands

The RSI is less than 70.

EXIT

The trade is closed when the RSI is less than 70

The lower standard deviation of the Bollinger Band is less than the closing price.

This strategy was backtested from the beginning of 2022 to capture how this strategy would perform in a bear market.

The strategy assumes each order to trade 70% of the available capital to make the results more realistic. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange by volume.

Simple_RSI+PA+DCA StrategyThis strategy is a result of a study to understand better the workings of functions, for loops and the use of lines to visualize price levels. The strategy is a complete rewrite of the older RSI+PA+DCA Strategy with the goal to make it dynamic and to simplify the strategy settings to the bare minimum.

In case you are not familiar with the older RSI+PA+DCA Strategy, here is a short explanation of the idea behind the strategy:

The idea behind the strategy based on an RSI strategy of buying low. A position is entered when the RSI and moving average conditions are met. The position is closed when it reaches a specified take profit percentage. As soon as the first the position is opened multiple PA (price average) layers are setup based on a specified percentage of price drop. When the price hits the layer another position with the same position size is is opened. This causes the average cost price (the white line) to decrease. If the price drops more, another position is opened with another price average decrease as result. When the price starts rising again the different positions are separately closed when each reaches the specified take profit. The positions can be re-opened when the price drops again. And so on. When the price rises more and crosses over the average price and reached the specified Stop level (the red line) on top of it, it closes all the positions at once and cancels all orders. From that moment on it waits for another price dip before it opens a new position.

This is the old RSI+PA+DCA Strategy:

The reason to completely rewrite the code for this strategy is to create a more automated, adaptable and dynamic system. The old version is static and because of the linear use of code the amount of DCA levels were fixed to max 6 layers. If you want to add more DCA layers you manually need to change the script and add extra code. The big difference in the new version is that you can specify the amount of DCA layers in the strategy settings. The use of 'for loops' in the code gives the possibility to make this very dynamic and adaptable.

The RSI code is adapted, just like the old version, from the RSI Strategy - Buy The Dips by Coinrule and is used for study purpose. Any other low/dip finding indicator can be used as well

The distance between the DCA layers are calculated exponentially in a function. In the settings you can define the exponential scale to create the distance between the layers. The bigger the scale the bigger the distance. This calculation is not working perfectly yet and needs way more experimentation. Feel free to leave a comment if you have a better idea about this.

The idea behind generating DCA layers with a 'for loop' is inspired by the Backtesting 3commas DCA Bot v2 by rouxam .

The ideas for creating a dynamic position count and for opening and closing different positions separately based on a specified take profit are taken from the Simple_Pyramiding strategy I wrote previously.

This code is a result of a study and not intended for use as a full functioning strategy. To make the code understandable for users that are not so much introduced into pine script (like myself), every step in the code is commented to explain what it does. Hopefully it helps.

Enjoy!

Negroni MA & RSI Strategy, plus trade entry and SL/TP optionsI will start with the context, and some things to think about when using a strategy tool to back-test ideas.

CONTEXT

FIRST: This is derived from other people's work, but I honestly hadn't found a mixed indicator MA strategy tool that does what this now does. If it is out there, apologies!!

This tool can help back-test various MA trends (SMA, EMA, HMA, VWMA); as well as factoring in RSI levels (or not); and can factor in a fixed HTF MA (or not). You can apply a 'retest entry' or a 'breakout entry', and you can also apply various risk mgt for SL/TP orders: 1) No SL/TP; or 2) a fixed %, or 3) dynamic ATR multipliers.

Find below, some details explaining what this tool is attempting to do.

Thank you, tack, salute!

THINGS TO REVIEW (it is not just about 'profitability'!!)

Whilst discretion is always highly encouraged as a trader, and a 100% indicator-driven strategy is VERY unlikely to yield sustainable results going forward, at the very least back-testing your strategies can help provide some guidance, not just on win rate Vs profit factor, but other things including:

a) Trade frequency: if a strategy has an 75% win rate and profit factor of 4, with all your parameters and confluence checks, but only triggers 3 trades every 5 years, is that realistically implementable to your trading situation if you have a $10,000 account?

b) Trade entry type: is it consistently better to wait for a retest of an 'MA zone', or is it better to market buy/sell on breakout of the 'MA zone'?

c) Risk management (SL/TP): is it consistently better to have a fixed static % for SL/TP ("I always place my stops 2% away, whether it is EURUSD or BTCUSDT"), or would you be better placed to try using an ATR multiplier of the respective assets?

d) Moving average type: is your old faithful 100 EMA really serving you well, or is the classic SMA more reliable, or how about the HMA, or the VWMA? Is the 100/200 cross holding up, or do you need something more sensitive? Is there any significant difference between a 10 EMA/20 EMA trend zone compared to a 13 EMA /25 EMA zone?

e) Confluence: Do added confluence checks (RSI, higher timeframe MA) actually improve profitability? But even if they do, is at the cost of cutting too many trades?

INPUTS AND PARAMETERS

Choice 1) Entry Strategy: Retest or Breakout - You can select both!

[ ]:

a) RETEST entry strat: price crosses UNDER FastMA INTO the 'MA trend zone'.

b) BREAKOUT entry strat: price crosses OVER FastMA OUT the 'MA trend zone'.

Choice 2) Risk Management (SL and TP) - You can select more than 1 strategy!

a) No SL/TP: Long trades are closed when the LOW crosses back UNDER the fastMA again, and shorts are closed when the HIGH crosses back OVER the fastMA again.

b) Static % SL/TP: Your SL/TP will be a fixed % away from avg. position price... WARNING: You should change this for various asset classes; FX vol is not the same as crypto altcoin vol!

c) Dynamic ATR SL/TP: Your SL/TP is a multiple of your selected ATR range (default is 50, see 'info' when you select ATR range). ATR accounts for the change in vol of different asset classes somewhat, HOWEVER... you should probably still not have the same multiplier trading S&P500 as you would trading crypto altcoins!

Then select your preferred parameters: EMA, SMA, HMA, VWMA, etc. You can mix and match, and most options have a info/tooltip guide.

RSI note: If you don't care for RSI levels, then set buy signal at 1... i.e always buys! Similarly set sell signal at 99.

ATR note: standard ATR length is usually 14, however... your SL/TP will move POST entry, and can tighten or widen your initial SL/TP... for better AND usually for worse! Go find a trade (strat 3) on the chart, look at the SL/TP lines, now change the number to 5, you'll see.

Fixed HTF MA note: If you don't care for HTF MA confluence, just change the timeframe/options to match the 'Slow MA' options you've chosen.

Divergence for Many [Dimkud - v5]Strategy is based on "Divergence for Many Indicators v4 ST" strategy by CannyTolany01

which is based on "Divergence for Many Indicator" indicator by LonesomeTheBlue

This strategy is searching for divergences on 18 indicators which you can select and optimise one by one.

Additionally you can connect any other External Indicator value. (just add this indicator the the chart and select option in settings)

To the original indicator/strategy I have added 9 additional indicators:

( Money Flow Index, Williams_Vix, Stochastic RSI , SMI Ergodic Oscillator, Volume Weighted MACD , Bull Bear Power, Balance of Power , Relative Volatility Index , Logistic Settings).

Converted strategy to v5 of Pine Script.

Added Static SL/TP in percents (%).

Added filters to filter enters:

1. Volume Weighted MACD - Multi-TimeFrame Filter

(It checks for histogram to falling or rising for a set periods of bars)

2. Money Flow Index - Multi-TimeFrame Filter

(It checks if MFI Oscillator is in the set diapason.

Also It checks if MFI is falling or rising for a set periods of bars )

3. ATR filter

(check changes in fast ATR to slow ATR )

Strategy shows good backtest results on many crypto tokens on 45m - 1h periods. (with parameters optimisation for every indicator)

To find best parameters - you can enable indicators one-by one, and optimise best parameters for each of them.

Then enable all indicators with successful results.

Optimise SL/TP.

Then try to enable and optimise filters (channels etc.)

The better is to optimise parameters separately for Short and Long trading. And run two separate bots (in settings enable only Long or only Short.)

Updates:

- Added visualisation for open trades (SL/TP)

- Added Volatility filter by ATR with many options for tests.

- Fixed some small bugs.

- Added second RSI filter (you can use two RSIs with different TF or settings)

- Updated ATR volatility and MFI filter. Removed non-effective options

- Added CCI filter

- Added option to Enable/Disable visualisation of TP/SL on chart

- Fixed one small quick bug. ("ATR filter short" was not working)

- Added Super Trend filter

- Added Momentum filter

- Added Volume Filter

- All "request.security" MultiTimeFrame calls changed to 100% non-repait function "f_security()"

Rsi strategy for BTC with (Rsi SPX)

I hope this strategy is just an idea and a starting point, I use the correlation of the Sp500 with the Btc, this does not mean that this correlation will exist forever!. I love Trading view and I'm learning to program, I find correlations very interesting and here is a simple strategy.

This is a trading strategy script written in Pine Script language for use in TradingView. Here is a brief overview of the strategy:

The script uses the RSI (Relative Strength Index) technical indicator with a period of 14 on two securities: the S&P 500 (SPX) and the symbol corresponding to the current chart (presumably Bitcoin, based on the variable name "Btc_1h_fixed"). The RSI is plotted on the chart for both securities.

The script then sets up two trading conditions using the RSI values:

A long entry condition: when the RSI for the current symbol crosses above the RSI for the S&P 500, a long trade is opened using the "strategy.entry" function.

A short entry condition: when the RSI for the current symbol crosses below the RSI for the S&P 500, a short trade is opened using the "strategy.entry" function.

The script also includes a take profit input parameter that allows the user to set a percentage profit target for closing the trade. The take profit is set using the "strategy.exit" function.

Overall, the strategy aims to take advantage of divergences in RSI values between the current symbol and the S&P 500 by opening long or short trades accordingly. The take profit parameter allows the user to set a specific profit target for each trade. However, the script does not include any stop loss or risk management features, which should be considered when implementing the strategy in a real trading scenario.

MVRV Z Score and MVRV Free Float Z-ScoreIMPORTANT: This script needs as much historic data as possible. Please run it on INDEX:BTCUSD , BNC:BLX or another chart of sufficient length.

MVRV

The MVRV (Market Value to Realised Value Ratio) simply divides bitcoins market cap by bitcoins realized market cap. This was previously impossible on Tradingview but has now been made possible thanks to Coinmetrics providing us with the realized market cap data.

In the free float version, the free float market cap is used instead of the regular market cap.

Z-Score

The MVRV Z-score divides the difference between Market cap and realized market cap by the historic standard deviation of the market cap.

Historically, this has been insanely accurate at detecting bitcoin tops and bottoms:

A Z-Score above 7 means bitcoin is vastly overpriced and at a local top.

A Z-Score below 0.1 means bitcoin is underpriced and at a local bottom.

In the free float version, the free float market cap is used instead of the regular market cap.

The Z-Score, also known as the standard score is hugely popular in a wide range of mathematical and statistical fields and is usually used to measure the number of standard deviations by which the value of a raw score is above or below the mean value of what is being observed or measured.

Credits

MVRV Z Score initially created by aweandwonder

MVRV initially created by Murad Mahmudov and David Puell

Kimchi Premium StrategyThis strategy is based on the Korea Premium, also known as the “Kimchi Premium,” which indicates how expensive or cheap the price of Bitcoin in Korean Won on a Bitcoin exchange in South Korea is relative to the price of Bitcoin being traded in USD or Tether. Inverse Kimchi Premium RSI was newly defined to create a strategy with Kimchi Premium. Assuming that the larger the kimchi premium, the greater the individual's purchasing power. In this case, if the Inverse Kimchi Premium RSI falls and closes the candle below the bear level, a short is triggered. Long is the opposite.

This strategy defaults to a combination of the traditional RSI and the Inverse Kimchi Premium RSI. If the user wishes to unlock the Inverse Kimchi Premium RSI combination and only use it as a traditional RSI strategy, the following settings can be used.

Use Combination of Inverse Kimchi Premium RSI: Uncheck

Resolution: Chart (4hr Candle)

Source: Close

Length of RSI: 14

Bull Level: 74

Bear Level: 25

__________________________________________________________________________________

김치프리미엄(김프) 전략은 달러 혹은 테더로 거래되고 있는 비트코인 가격 대비 한국에 있는 비트코인 거래소의 비트코인 원화 가격이 얼마나 비싸고 싼 지를 나타내는 코리아 프리미엄, 일명 "김치 프리미엄" 지표를 기반으로 만들어졌습니다. 김치 프리미엄을 가지고 전략을 만들기위해 Inverse Kimchi Premium RSI를 새롭게 정의하였습니다. 김치 프리미엄이 커질수록 개인의 매수세가 커진다고 가정하고, 이 경우 Inverse Kimchi Premium RSI이 하락하여 Bear Level 아래에서 캔들 마감을 하면 Short을 트리거 합니다. Long은 그 반대입니다.

이 전략은 전통적인 RSI와 Inverse Kimchi Premium RSI을 조합하여 기본값을 설정하였습니다. 유저가 원한다면 Inverse Kimchi Premium RSI의 조합을 해제하고 전통적인 RSI 전략으로만 사용하려면 아래 다음의 설정값을 사용할 수 있습니다.

Use Combination of Inverse Kimchi Premium RSI: 체크 해제

Resolution: Chart (4hr Candle)

Source: Close

Length of RSI: 14

Bull Level: 74

Bear Level: 25

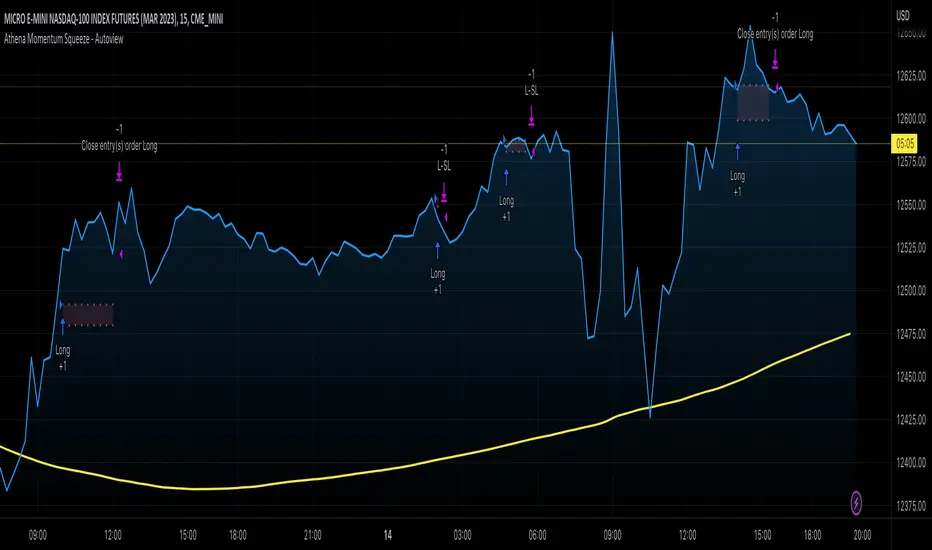

Athena Momentum Squeeze - Short, Lean, and Mean This is a very profitable strategy focusing on 15 minute intervals on the Micro Nasdaq Futures contracts. CME_MINI:MNQH2023

As this contract only keeps positions for on average about an hour risk is managed. At a profit factor of 3.382 with a max drawdown of $123 from January 1st to February 15. Looking back to Dec 2019 still maintains a profit factor of 1.3.

See backtesting: www.screencast.com

2019 backtesting: www.screencast.com

Based on the classic Lazy Bear Oscillator Squeeze with a number of modifications from ADX, MAs and adding fibonacci levels.

We like keeping strategies simple yet powerful, no completely where you can't understand your own trades.

Our team is always modifying and improving the strategy. Always open to collaborating on improving as there is no perfect strategy. www.screencast.com

Exponential Stochastic Strategywhat is Exponential Stochastic?

it is a modified version of the stochastic indicator. This strategy does not include pyramiding, repaint, trailing stop or take profit.

what it does?

It contains an extra input in addition to the stochastic indicator. Thanks to this input, different exponential weights can be given to the outputs and the indicator can be made more sensitive or insensitive. The strategy buys when the indicator leaves the overbought zone, sells when it leaves the oversold zone and always stays in the trade.

how it does it?

it uses this formula: i.hizliresim.com

Thanks to this formula, even if the weights given to the outputs change, the indicator always continues to take a value between 0 and 100.

how to use it ?

With the input named "exp", you can change the sensitivity of the indicator and develop different strategies. other inputs are the same as the stochastic indicator. Increasing the exp value causes the indicator to signal less, decreasing it makes it much more sensitive.

TradePro's 2 EMA + Stoch RSI + ATR StrategySaw TradePro's "NEW BEST HIGHEST PROFITING STRATEGY WITH CRAZY RESULTS - 2 EMA+ Stochastic RSI+ ATR", and was curious on the back testing results. This strategy is an attempt to recreate it.

This strategy uses 50 / 200 EMAs, Stochastic RSI and ATR.

Long Entry Criteria:

- 50 EMA > 200 EMA

- Price closes below 50 EMA

- Stochastic RSI has gone into oversold < 20

- Stochastic RSI crosses up while making higher low from previous cross up

Short Entry Criteria:

- 50 EMA < 200 EMA

- Price closes above 50 EMA

- Stochastic RSI has gone into overbought > 80

- Stochastic RSI crosses down while making lower high from previous cross down

Stop-loss is set to ATR stop-loss

Take Profit is 2x the risk

All parameters are configurable.

Enjoy~~

Fair Value Strategy UltimateThis is a strategy using an index's (SPX, NDX, RUT) Fair Value derived from Net Liquidity.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: net_liquidity/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

The net liquidity values I calculate outside of TradingView. If you'd like the strategy to work for future dates, you'll need to update the reference to my NetLiquidityLibrary , which I update daily.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

Optimal Parameters:

I've optimized the parameters for each index using the python backtesting library and they are as follows =>

SPX

Scalar: 1.1

Subtractor: 1425

OB Threshold: 0

OS Threshold: -175

NDX

Scalar: 0.5

Subtractor: 250

OB Threshold: 0

OS Threshold: -25

RUT

Scalar: 3.2

Subtractor: 50

OB Threshold: 25

OS Threshold: -25

Strategy Myth-Busting #5 - POKI+GTREND+ADX - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our fifth one we are automating is one of the strategies from "The Best 3 Buy And Sell Indicators on Tradingview + Confirmation Indicators ( The Golden Ones ))" from "Online Trading Signals (Scalping Channel)". No formal backtesting was done by them and resuructo messaged me asking if we could validate their claims.

Originally, we mimic verbatim the settings Online Trading Signals was using however weren't getting promising results. So before we stopped there we thought we might want to see if this could be improved on. So we adjusted the Renko Assignment modifier from ATR to Traditional and adjusted the value to be higher from 30 to 47. We also decided to try adding another signal confirmation to eliminate some of the ranged market conditions so we choose our favorite, ADX . Also, given we are using this on a higher time-frame we adjusted the G-Channel Trend detection source from close to OHLC4 to get better average price action indication and more accurate trend direction.

This strategy uses a combination of 2 open-source public indicators:

poki buy and sell Take profit and stop loss by RafaelZioni

G-Channel Trend Detection by jaggedsoft

Trading Rules

15m - 4h timeframe. We saw best results at the recommended 1 hour timeframe.

Long Entry:

When POKI triggers a buy signal

When G-Channel Trend Detection is in an upward trend (Green)

ADX Is above 25

Short Entry:

When POKI triggers a sell signal

When G-Channel Trend Detection is in an downward trend (red)

ADX Is above 25

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

PSAR BBPT ZLSMA BTC 1minLong entry:

PSAR gives buy signal

BBPT prints green histogram

ZLSMA is below the price

ZLSMA has uptrend

SL is smaller than the max SL

Optional Sessions and EMA filters

Short entry

PSAR gives sell signal

BBPT prints red histogram

ZLSMA is above the price

ZLSMA has downtrend

SL is smaller than the max SL

Optional Sessions and EMA filters

SL:

Placed below ZLSMA + offset on long

Placed above ZLSMA + offset on short

TP1:

1x the SL by default

Takes no profit by default, 50% is also a good setting

TP2:

2x the SL by default

Take out all remaining position size.

If price reaches TP1, the SL is set to the entry price.