Overnight Z/VolRatio SignalThis indicator highlights overnight setups where both volatility expansion and prior-day range deviation suggest directional opportunity at the RTH open.

It calculates:

• Overnight Z-Score (Z_long): how far the overnight session’s range tilts from the 20-day overnight mean, standardized by its standard deviation.

• VolRatio: ratio of the current RTH session volume to the 20-day average, a proxy for participation and conviction.

Signal Logic (LONG bias)

A long-bias condition triggers when:

• Z_long ≥ 0.40 (overnight tilt strongly positive)

• VolRatio ≥ 1.30 (above-average RTH volume)

• Optional filters: R1/R4 region alignment, YDH/YDL proximity, and other context flags.

Visuals mark qualifying days with colored labels and session highlights.

It is intended as a context signal — not an auto-trading system — for SPY/SPX/ES or correlated large-cap indices.

Usage Notes

• Works best when applied to daily or intraday 5m chart with extended hours enabled.

• Typical exit: ~150 minutes after 09:30 ET.

• Fridays are optionally excluded to avoid expiration-related distortions.

Overnight

NightWatch 24/5 [theUltimator5]NightWatch 24/5 is a comprehensive indicator designed to seamlessly display both regular and overnight trading (BOATS exchange) into a single chart. Current TV limitations don't allow both overnight trading and regular exchanges to appear on the same chart due to timeframe visibility settings. We can either select between RTH (Regular Trading Hours) or ETH (Extended Trading Hours). There is no option to show 24 hour charts when looking at a stock. This indicator attempts to solve this issue.

Please read the entire description thoroughly because this indicator takes a little bit of setup to work properly!

---IMPORTANT-- -

This indicator MUST be used over a liquid cryptocurrency chart, like Bitcoin. It requires access to something that trades 24/7 and has volume data for all periods. Bitcoin on Coinbase is the best option. Please select Bitcoin as your main ticker before adding this indicator to the chart.

-------------------

This indicator combines the price of both the regular trading hours and the overnight trading to create a single price line and volume candles. You can select view settings to either overlay the price on the chart, or have it below the chart. Volume can be toggled on or off as well.

Default settings:

Ticker = GME

Overlay Candles on Main Chart = true

Display Data = Both Price and Volume

Show Status Table = true

Here is an explanation for each of these settings:

Ticker - Type in the ticker you want to track overnight and intraday data for

Overlay Candles on Main chart - This will push the price candles onto the main chart area instead of below it. Volume candles will remain in their own separate pane below. This is useful if you want to track both price and volume without adding the indicator twice.

Display Data - This determines what data to show. Volume, price, or both volume and price.

Show Status Table - This toggles on or off the table that shows the ticker name, current session, and the price (change) of the ticker since the most recent daily close.

If you overlay the price onto the chart, the price of the stock you are looking at will likely be a VERY different price than the crypto it is overlaying against. There are a couple workarounds. You can either zoom into the chart around the price of the stock you are looking at (time consuming), or you can go into your object tree and drag the indicator up into the main chart area. This will overlay the price onto the crypto while maintaining it's own unique y-axis.

After you move the indicator up, you can add the indicator back a second time, then change the settings to only show the volume candles. You can then toggle off the table on one of the two so you don't see duplicate tables. This is the setting I am showing in my chart above. The indicator is added twice with the price being pulled up into the same window as Bitcoin, then a second instance below showing just volume.

--LIMITATIONS--

Since the indicator requires the use of a 24 hour market ticker like Bitcoin, it DOES NOT display extended hours data. The price and volume data STOPS at 16:00 EST then resumes back up at 20:00 EST when BOATS opens. At 04:00, the price and volume then stops until 09:30, when the regular trading hours begin. This causes a flat line in the price during those periods. Unfortunately, there is no current workaround to this issue.

If Bitcoin becomes illiquid (or whatever crypto you choose), it will only populate data for the ticker you want if there is data available for that crypto at the same time period. A gap in Bitcoin volume will show a gap in trade activity for your ticker.

Intraday vs Overnight OBV🔍 Purpose

This indicator provides a volume-weighted cumulative flow model that mimics On-Balance Volume (OBV) logic but splits the volume impact into intraday vs. overnight sessions. It allows traders to track how volume contributes to price movement in each session and identify whether buying/selling pressure is stronger during or outside of regular trading hours.

This indicator attempts to alleviate some of the downfalls of the standard OBV indicator, which only looks at total volume and total direction. The price of stocks generally behaves extremely differently during market hours and outside market hours, and many of the large moves happen outside of regular market hours on low volume.

⚙️ Core Features

1) OBV-style calculation:

If price increases → volume is added to the OBV stream.

If price decreases → volume is subtracted.

If price is flat → OBV remains unchanged.

2) Session splitting:

Intraday session: movement from today's open to close.

Overnight session: movement from yesterday’s close to today’s open.

Volume is split proportionally between these two periods based on user input.

3) Four visualization modes:

"Intraday" — plots only OBV from intraday price movement.

"Overnight" — plots only OBV from overnight price movement.

"Aggregate" — plots the sum of intraday and overnight OBV for a holistic view.

"Both Intraday and Overnight" — plots intraday and overnight OBV separately on the same chart.

📐 Inputs

1) Synthetic OBV Type:

"Intraday" — Show OBV from open to close only.

"Overnight" — Show OBV from prior close to today's open only.

"Aggregate" — Show a single line combining both.

"Both Intraday and Overnight" — Show both lines on the same chart.

2) Estimated Overnight Volume %:

Percentage of total daily volume assumed to occur during extended hours.

The rest is allocated to regular session (intraday).

Default: 20% overnight, 80% intraday.

🧮 How It Works

Volume Splitting:

Total bar volume is split into overnight Volume and intraday Volume:

Intraday change is the difference between today’s close and open.

Overnight change is the difference between today’s open and yesterday’s close.

Session OBV Calculations:

OBV is incremented/decremented by the session's allocated volume, depending on whether the session’s price change was positive or negative.

Aggregate OBV:

Combines both session deltas for a holistic volume flow view.

📊 Interpretation

Rising OBV (any stream) suggests accumulation; falling OBV suggests distribution.

Divergences between price and OBV lines (especially overnight vs. intraday) can reveal where hidden buying/selling is occurring.

Comparing intraday vs overnight OBV can help:

Spot whether institutional demand is building off-hours.

Detect retail vs. institutional behavior (retail trades often dominate intraday; institutional may prefer after-hours).

💡 Use Cases

Identify whether overnight gaps are supported by overnight volume momentum.

Detect accumulation in low-volume overnight sessions.

Compare intraday and overnight strength during earnings season or news events.

Complement traditional OBV by seeing session-based breakdowns.

Overnight vs Intra-day Performance█ STRATEGY OVERVIEW

The "Overnight vs Intra-day Performance" indicator quantifies price behaviour differences between trading hours and overnight periods. It calculates cumulative returns, compound growth rates, and visualizes performance components across user-defined time windows. Designed for analytical use, it helps identify whether returns are primarily generated during market hours or overnight sessions.

█ USAGE

Use this indicator on Stocks and ETFs to visualise and compare intra-day vs overnight performance

█ KEY FEATURES

Return Segmentation : Separates total returns into overnight (close-to-open) and intraday (open-to-close) components

Growth Tracking : Shows simple cumulative returns and compound annual growth rates (CAGR)

█ VISUALIZATION SYSTEM

1. Time-Series

Overnight Returns (Red)

Intraday Returns (Blue)

Total Returns (White)

2. Summary Table

Displays CAGR

3. Price Chart Labels

Floating annotations showing absolute returns and CAGR

Color-coded to match plot series

█ PURPOSE

Quantify market behaviour disparities between active trading sessions and overnight positioning

Provide institutional-grade attribution analysis for returns generation

Enable tactical adjustment of trading schedules based on historical performance patterns

Serve as foundational research for session-specific trading strategies

█ IDEAL USERS

1. Portfolio Managers

Analyse overnight risk exposure across holdings

Optimize execution timing based on return distributions

2. Quantitative Researchers

Study market microstructure through time-segmented returns

Develop alpha models leveraging session-specific anomalies

3. Market Microstructure Analysts

Identify liquidity patterns in overnight vs daytime sessions

Research ETF premium/discount mechanics

4. Day Traders

Align trading hours with highest probability return windows

Avoid overnight gaps through informed position sizing

GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

Overnight Positioning w EMA - Strategy [presentTrading]I've recently started researching Market Timing strategies, and it’s proving to be quite an interesting area of study. The idea of predicting optimal times to enter and exit the market, based on historical data and various indicators, brings a dynamic edge to trading. Additionally, it is integrated with the 3commas bot for automated trade execution.

I'm still working on it. Welcome to share your point of view.

█ Introduction and How it is Different

The "Overnight Positioning with EMA " is designed to capitalize on market inefficiencies during the overnight trading period. This strategy takes a position shortly before the market closes and exits shortly after it opens the following day. What sets this strategy apart is the integration of an optional Exponential Moving Average (EMA) filter, which ensures that trades are aligned with the underlying trend. The strategy provides flexibility by allowing users to select between different global market sessions, such as the US, Asia, and Europe.

It is integrated with the 3commas bot for automated trade execution and has a built-in mechanism to avoid holding positions over the weekend by force-closing positions on Fridays before the market closes.

BTCUSD 20 mins Performance

█ Strategy, How it Works: Detailed Explanation

The core logic of this strategy is simple: enter trades before market close and exit them after market open, taking advantage of potential price movements during the overnight period. Here’s how it works in more detail:

🔶 Market Timing

The strategy determines the local market open and close times based on the selected market (US, Asia, Europe) and adjusts entry and exit points accordingly. The entry is triggered a specific number of minutes before market close, and the exit is triggered a specific number of minutes after market open.

🔶 EMA Filter

The strategy includes an optional EMA filter to help ensure that trades are taken in the direction of the prevailing trend. The EMA is calculated over a user-defined timeframe and length. The entry is only allowed if the closing price is above the EMA (for long positions), which helps to filter out trades that might go against the trend.

The EMA formula:

```

EMA(t) = +

```

Where:

- EMA(t) is the current EMA value

- Close(t) is the current closing price

- n is the length of the EMA

- EMA(t-1) is the previous period's EMA value

🔶 Entry Logic

The strategy monitors the market time in the selected timezone. Once the current time reaches the defined entry period (e.g., 20 minutes before market close), and the EMA condition is satisfied, a long position is entered.

- Entry time calculation:

```

entryTime = marketCloseTime - entryMinutesBeforeClose * 60 * 1000

```

🔶 Exit Logic

Exits are triggered based on a specified time after the market opens. The strategy checks if the current time is within the defined exit period (e.g., 20 minutes after market open) and closes any open long positions.

- Exit time calculation:

exitTime = marketOpenTime + exitMinutesAfterOpen * 60 * 1000

🔶 Force Close on Fridays

To avoid the risk of holding positions over the weekend, the strategy force-closes any open positions 5 minutes before the market close on Fridays.

- Force close logic:

isFriday = (dayofweek(currentTime, marketTimezone) == dayofweek.friday)

█ Trade Direction

This strategy is designed exclusively for long trades. It enters a long position before market close and exits the position after market open. There is no shorting involved in this strategy, and it focuses on capturing upward momentum during the overnight session.

█ Usage

This strategy is suitable for traders who want to take advantage of price movements that occur during the overnight period without holding positions for extended periods. It automates entry and exit times, ensuring that trades are placed at the appropriate times based on the market session selected by the user. The 3commas bot integration also allows for automated execution, making it ideal for traders who wish to set it and forget it. The strategy is flexible enough to work across various global markets, depending on the trader's preference.

█ Default Settings

1. entryMinutesBeforeClose (Default = 20 minutes):

This setting determines how many minutes before the market close the strategy will enter a long position. A shorter duration could mean missing out on potential movements, while a longer duration could expose the position to greater price fluctuations before the market closes.

2. exitMinutesAfterOpen (Default = 20 minutes):

This setting controls how many minutes after the market opens the position will be exited. A shorter exit time minimizes exposure to market volatility at the open, while a longer exit time could capture more of the overnight price movement.

3. emaLength (Default = 100):

The length of the EMA affects how the strategy filters trades. A shorter EMA (e.g., 50) reacts more quickly to price changes, allowing more frequent entries, while a longer EMA (e.g., 200) smooths out price action and only allows entries when there is a stronger underlying trend.

The effect of using a longer EMA (e.g., 200) would be:

```

EMA(t) = +

```

4. emaTimeframe (Default = 240):

This is the timeframe used for calculating the EMA. A higher timeframe (e.g., 360) would base entries on longer-term trends, while a shorter timeframe (e.g., 60) would respond more quickly to price movements, potentially allowing more frequent trades.

5. useEMA (Default = true):

This toggle enables or disables the EMA filter. When enabled, trades are only taken when the price is above the EMA. Disabling the EMA allows the strategy to enter trades without any trend validation, which could increase the number of trades but also increase risk.

6. Market Selection (Default = US):

This setting determines which global market's open and close times the strategy will use. The selection of the market affects the timing of entries and exits and should be chosen based on the user's preference or geographic focus.

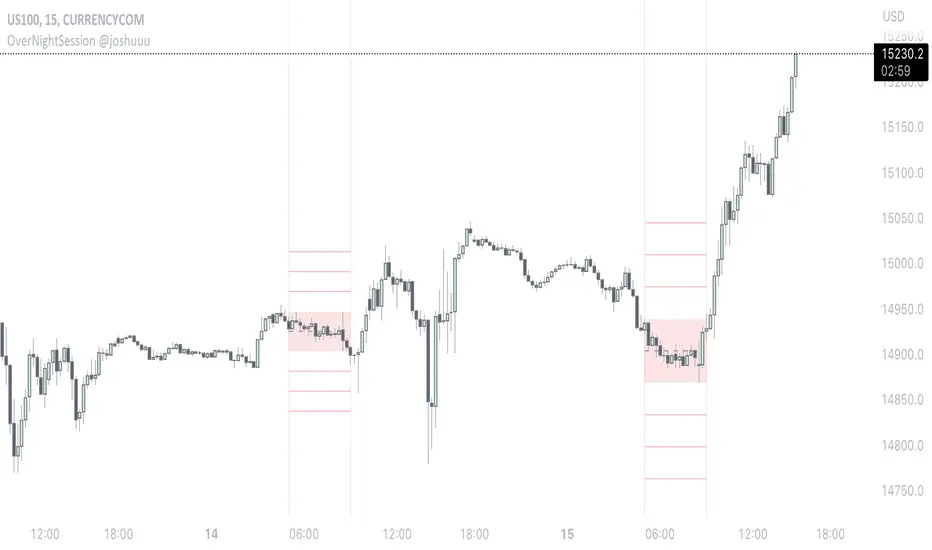

OverNightSession @joshuuuThis indicator highlights the Overnightsession (ONS), taught by TheCurrenyMerchant.

The Overnightsession is from 4-8 am UTC-5. This session can be used to form trades, e.g. after one side has been taken out.

It has the options to display Projection and the equilibrium level. Equilibrium level (50%) can be used to identify if price is currently in premium/discount of the range and the projections (standard deviations of the range) can be used to identify possible targets.

A classic setup he teaches is:

Price trades agressively out of the range taking liquidity. As soon as we trade above the high of the candle that took liquidity, that candle can be considered an orderblock, where the 50% level can be used for long setups.

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

Pre-market Highs & Lows on regular trading hours (RTH) chartShows pre-market highs and lows on RTH or ETH chart

-Pre-market duration user input (default is 16 'bar hours'; covering the time from S&P RTH close at 4pm >> 9:30am RTH open next day

-Displays on both RTH and ETH charts

-Written for ES (ES1! or e.g ESM2023), but tested and working on SPY, SPX

-Works across timeframes

Example usage on Electronic trading hours (ETH) chart; showing the 'bar hours' user input lookback duration visually

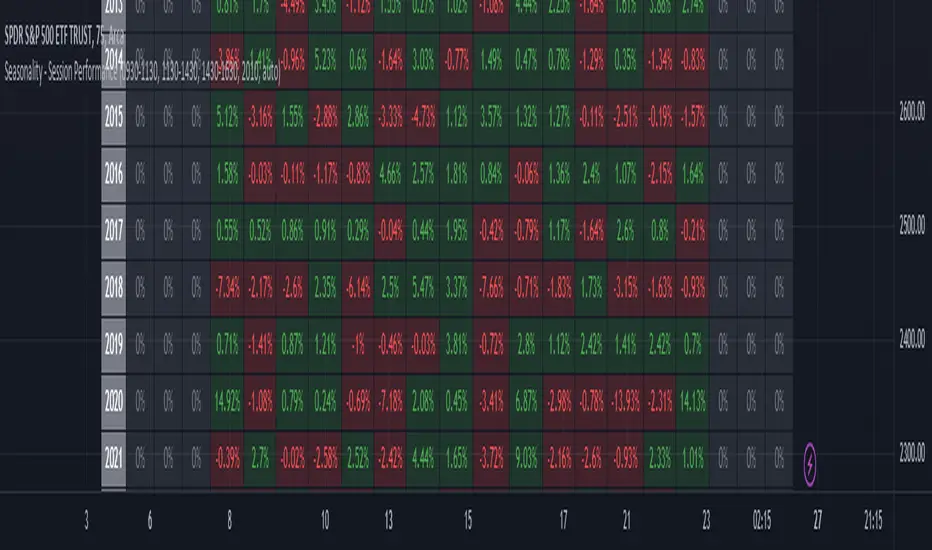

Seasonality - Session Performance - Morning Afternoon EveningUse this indicator on Intraday Timeframe. Higher the timeframe, more the data

This script calculates the performance of an instrument for different sessions.

Session inputs can be updated to study performance of

- Morning vs Afternoon vs Evening

- Pre-Market vs Market vs Post-Market (provided the data feed supports pre and post market)

- Overnight vs Intraday

Three session inputs are provided to tweak the session range

Performance is calculated as session close / session open - 1

Session timeframes can be set for various countries. Make sure the session timeframe aligns with the Candle open/close for the timeframe you choose. Some examples below

US Markets: 0930-1130 1130-1430 1430-1630 Timeframe 1 hour

India Markets: 0915-1030 1030-1415 1415-15:30 Timeframe 75min

ILM Overnight vs Intraday Performance - Tabular FormUse this indicator on Daily Timeframe

This script compares Overnight vs Intraday Performance based on the Day of the Week (DOW) - Sun - Sat of index/stock/currency/commodity symbols.

ON column indicates Overnight performance = open/close -1

ID column indicates Intraday performance = close-open/1

The calculations are detailed in the tooltips of the individual table cells.

Federal Funds Rate and Overnight Bank Fund RateAMEX:SPY

Comparison of the Overnight Bank Fund Rate and the Effective Federal Funds Rate.

The Fed sets a discount rate of 100 basis points above the effective federal funds rate to discourage ("penalize") banks from borrowing from its reserves. If lending banks have excess in their reserves, the borrowing banks have ease in negotiating a lower rate overnight to maintain its requirements. For this reason its a good indicator of the economy. If it becomes more difficult for banks to maintain the required reserve amount they may charge borrowing banks higher rates.

Both the Effective Federal Funds Rate and Overnight Bank Fund Rate use the same data. Except, the OBFR includes overnight Eurodollar transaction data and certain overnight “selected deposit” transactions that are placed at domestic bank branches controlled by a U.S. banking office.

The indicator includes the lower and upper bound target rate set by the Federal Reserve.

An interesting note:

Notice the jump in the Overnight Bank Rate followed by Fed buying to provide liquidity and lower rates in Sept 2019.

Equity Index Extended HoursHighlights the extended hours/Globex session for US Equity Index Futures.

Overnight Bollinger Band ExtremesThis script is a combination of my overnight fakeout script and bollinger band color bars. It's designed to be used on CME/CBOT Equity Indexes during their GLOBEX session. It uses the built in Bollinger Band script and highlights bars that exceed the upper/lower bands during the overnight session.

Equity Index Overnight FakeoutThis script highlights when price violates the highest high or lowest low within the user's selected lookback period, with the caveat that it occurs during the GLOBEX session. The script is designed to work exclusively with the trading hours for CME and CBOT Equity Index futures. I'm planning to make a more customizable version down the line.

My reasoning behind this very simple script is that the low liquidity and participation of the overnight session creates a tendency for moves at extremes to mean revert. Let me know what you think.

Market Profile for Futures with Session and After Hours SplitAdapted existing Market Profile scripts to be move suitable for Futures Markets with Session and After Hours split

Script Provides split Market Profiles for Session and After Hours

Users can customize the Session and AH hours inputs to suit any ticker and their interpretation of prime and non-prime hours