Trends in Black and White'Trends in Black and White' is now rolling out to all of our Pro Community members

What is it for? This is a simple visual indicator designed to help users identify long or short bias. It does not provide direct entries and exits but can be used effectively in combination with Trendmaster Premium and other technical analysis methods.

How do i get access?

This indicator is available as a free extra to all of our Pro community members only.

All of our packages are listed below.

- Premium - $50 - This gives you access to the TrendMaster Premium TradingView indicator (www.tradingview.com), the TrendMaster Premium Binance signal bots and the Premium Discord channels.

- Premium+ - $75 or $25 for existing Premium users - All the benefits of the Premium package, but with added signal bots for Bittrex, Bitfinex and Kucoin exchanges.

- Pro - $100 or $50 for existing Premium users/$25 for existing Premium+ users -Access to 'Trendmaster Premium' and 'Trends in Black and White' indicators. All the benefits of the Premium+ package, but with added signal bots for D1 and H4 Ichimoku TK cross and Ichimoku cloud breakout for Binance.

The mandatory Legal bit:

@IchimokuScholar and @Crypto_C00kie wish you the best of luck in achieving your trading goals. Please apply appropriate risk management.

Any form of trading has large potential rewards but also large potential risks. The Purchaser must be aware of those risks and be willing to accept them. Don't trade with money that you, the Purchaser cannot afford to lose. No representation is being made that you are guaranteed positive results. The past performance of any trading methodology is not necessarily indicative of future results. Trading involves high risks. @TrendmasterTM, @IchimokuScholar or @Crypto_C00kie are NOT responsible for any trades that you, the Purchaser take. All trades taken are entirely at the Purchasers own risk. Refunds are neither offered nor implied.

在脚本中搜索"implied"

TrendMaster Premium ©Trendmaster Premium©

We are proud to release the final version of Trendmaster Premium©. This indicator is the result of months of development between @TrendmasterTM and @Crypto_C00kie.

Trendmaster Premium© is a Trend following system that provide entries, exits and stop loss placement. It is extremely simple to follow and we have experienced outstanding results.

When purchasing Trendmaster Premium© you will receive access to the indicator suite and access to our private members discord group.

Discord: The discord channel is a place where traders can discuss ideas and share content.

It includes

Bots – The discord channel currently has two bots that constantly scan Binance for signals. They will alert you by notification of any BTC pair that has printed a signal candle. Currently the bots report D1 and H4 signals as these are the time frames the indicator is designed for. These are designed to alert you to possible trades and should NOT be blindly traded from.

Chat – Several chat servers offering educational resources, guidance on how to use the indicator and chart/idea sharing.

The mandatory Legal bit:

@IchimokuScholar and @Crypto_C00kie wish you the best of luck in achieving your trading goals. Please apply appropriate risk management.

Any form of trading has large potential rewards but also large potential risks. The Purchaser must be aware of those risks and be willing to accept them. Don't trade with money that you, the Purchaser cannot afford to lose. No representation is being made that you are guaranteed positive results. The past performance of any trading methodology is not necessarily indicative of future results. Trading involves high risks. Neither @TrendmasterTM or @Crypto_C00kie are responsible for any trades that you, the Purchaser take. All trades taken are entirely at the Purchasers own risk. Refunds are neither offered nor implied.

Bollinger Bear SniperThis script uses Bollinger Band but with different interpretation. The upper Bollinger Band is the resistant level, the lower Bollinger Band is the base or support level. The Commodity Channel Index (CCI) and the Bollinger Bandwidth helps us avoid high risk.

The script identifies candles that are marking bold upward moves in prices and fires buy signal. Sales signals are fired when the candle closes in positive. The idea is to buy and sell on the same candle or next positively closed candle. This is anti-bear-anti-bags strategy. You either make profit or loss holding no bag. When you gain more than lose you are in business. This script is set to gain more than lose. We however offer no guarantee, expressed or implied. We are NOT responsible.

Nq/ES daily CME risk intervalReverse engineering the risk interval for CME (Chicago Mercantile Exchange) products based on margin requirements involves understanding the relationship between margin requirements, volatility, and the risk interval (price movement assumed for margin calculation)

The CME uses a methodology called SPAN (Standard Portfolio Analysis of Risk) to calculate margins. At a high level, the initial margin is derived from:

Initial Margin = Risk Interval × Contract Size × Volatility Adjustment Factor

Where:

Risk Interval: The price movement range used in the margin calculation.

Contract Size: The unit size of the futures contract.

Volatility Adjustment Factor: A measure of how much price fluctuation is expected, often tied to historical volatility.

To calculate an approximate of the daily CME risk interval, we need:

Initial Margin Requirement: Available on the CME Group website or broker platforms.

Contract Size: The size of one futures contract (e.g., for the S&P 500 E-mini, it is $50 × index points).

Volatility Adjustment Factor: This is derived from historical volatility or CME's implied volatility estimates.

As we do not have access to CME calculations , the volatility adjustment factor can be estimated using historical volatility: We calculate the standard deviation of daily returns over a specific period (e.g., 20 or 30 or 60 days).

Key Considerations

The exact formulas and parameters used by CME for CME's implied volatility estimates are proprietary, so this calculation based on standard deviation of daily returns is an approximation.

How to use:

Input the maintenance margin obtained from the CME website.

Adjust volatility period calculation.

The indicator displays the range high and low for the trading day.

1.Lines can be used as targets intraday

2.Market tends to snap back in between the lines and close the day in the range

Predicted Funding RatesOverview

The Predicted Funding Rates indicator calculates real-time funding rate estimates for perpetual futures contracts on Binance. It uses triangular weighting algorithms on multiple different timeframes to ensure an accurate prediction.

Funding rates are periodic payments between long and short position holders in perpetual futures markets

If positive, longs pay shorts (usually bullish)

If negative, shorts pay longs (usually bearish)

This is a prediction. Actual funding rates depend on the instantaneous premium index, derived from bid/ask impacts of futures. So whilst it may imitate it similarly, it won't be completely accurate.

This only applies currently to Binance funding rates, as HyperLiquid premium data isn't available. Other Exchanges may be added if their premium data is uploaded.

Methods

Method 1: Collects premium 1-minunute data using triangular weighing over 8 hours. This granular method fills in predicted funding for 4h and less recent data

Method 2: Multi-time frame approach. Daily uses 1 hour data in the calculation, 4h + timeframes use 15M data. This dynamic method fills in higher timeframes and parts where there's unavailable premium data on the 1min.

How it works

1) Premium data is collected across multiple timeframes (depending on the timeframe)

2) Triangular weighing is applied to emphasize recent data points linearly

Tri_Weighing = (data *1 + data *2 + data *3 + data *4) / (1+2+3+4)

3) Finally, the funding rate is calculated

FundingRate = Premium + clamp(interest rate - Premium, -0.05, 0.05)

where the interest rate is 0.01% as per Binance

Triangular weighting is calculated on collected premium data, where recent data receives progressively higher weight (1, 2, 3, 4...). This linear weighting scheme provides responsiveness to recent market conditions while maintaining stability, similar to an exponential moving average but with predictable, linear characteristics

A visual representation:

Data points: ──────────────>

Weights: 1 2 3 4 5

Importance: ▂ ▃ ▅ ▆ █

How to use it

For futures traders:

If funding is trending up, the market can be interpreted as being in a bull market

If trending down, the market can be interpreted as being in a bear market

Even used simply, it allows you to gauge roughly how well the market is performing per funding. It can basically be gauged as a sentiment indicator too

For funding rate traders:

If funding is up, it can indicate a long on implied APR values

If funding is down, it can indicate a short on implied APR values

It also includes an underlying APR, which is the annualized funding rate. For Binance, it is current funding * (24/8) * 365

For Position Traders: Monitor predicted funding rates before entering large positions. Extremely high positive rates (>0.05% for 8-hour periods) suggest overleveraged longs and potential reversal risk. Conversely, extreme negative rates indicate shorts dominance

Table:

Funding rate: Gives the predicted funding rate as a percentage

Current premium: Displays the current premium (difference between perpetual futures price and the underlying spot) as a percentage

Funding period: You can choose between 1 hour funding (HyperLiquid usually) and 8 hour funding (Binance)

APR: Underlying annualized funding rate

What makes it original

Whilst some predicted funding scripts exist, some aren't as accurate or have gaps in data. And seeing as funding values are generally missing from TV tickers, this gives traders accessibility to the script when they would have to use other platforms

Notes

Currently only compatible with symbols that have Binance USDT premium indices

Optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off

Actual funding rates may differ

Inputs

Funding Period: Choose between "8 Hour" (standard Binance cycle) or "1 Hour" (divides the 8-hour rate by 8 for granular comparison)

Plot Type: Display as "Funding Rate" (percentage per interval) or "APR" (annualized rate calculated as 8-hour rate × 3 × 365)

Table: Toggle the information table showing current funding rate, premium, funding period, and APR in the top-right corner

Positive Colour: Sets the colour for positive funding rates where longs pay shorts (default: #00ffbb turquoise)

Negative Colour: Sets the colour for negative funding rates where shorts pay longs (default: red)

Table Background: Controls the background colour and transparency of the information table (default: transparent dark blue)

Table Text Colour: Sets the colour for all text labels in the information table (default: white)

Table Text Size: Controls font size with options from Tiny to Huge, with Small as the default balance of readability and space

CMC Macro Regime PanelOverview (what it is):

A macro‑regime gate built entirely from TradingView-native symbols (CRYPTOCAP, FRED, DXY/VIX, HYG/LQD). It aggregates central‑bank liquidity (Fed balance sheet − RRP − Treasury General Account), USD strength, credit conditions, stablecoin flows/dominance, tech beta and BTC–NDX co‑move into one normalized score (CLRC). The panel outputs Risk‑ON/OFF regimes, an Early 3/5 pre‑signal, and an automatic BTC vs ETH vs ALTs preference. It is intentionally scoped to Daily & Weekly reads (no intraday timing). Publish with a clean chart and a clear description as per TradingView rules.

TradingView

Why we also use other TradingView screens (and why that is compliant)

This script pulls data via request.security() from official TV symbols only; users often want to open the raw series on separate charts to sanity‑check:

CRYPTOCAP indices: TOTAL, TOTAL2, TOTAL3 (market cap aggregates) and dominance tickers like BTC.D, USDT.D. Helpful for regime & rotation (ALTs vs BTC). TradingView provides definitions for crypto market cap and dominance symbols.

TradingView

+3

TradingView

+3

TradingView

+3

FRED releases: WALCL (Fed assets, weekly), RRPONTSYD (ON RRP, daily), WTREGEN (TGA, weekly), M2SL (M2, monthly). These are the official macro sources exposed on TV.

FRED

+3

FRED

+3

FRED

+3

Risk proxies: TVC:DXY (USD index), TVC:VIX (implied vol), AMEX:HYG/AMEX:LQD (credit), NASDAQ:NDX (tech beta), BINANCE:ETHBTC. VIX/NDX relationship is well-documented; VIX measures 30‑day expected S&P500 vol.

TradingView

+2

TradingView

+2

Compliance note: Using multiple screens is optional for users, but it explains/justifies how components work together (a requirement for public scripts). Keep publication chart clean; use extra screens only to illustrate in the description.

TradingView

How it works (high level)

Liquidity block (Weekly/Monthly)

Net Liquidity = WALCL − RRPONTSYD − WTREGEN (YoY z‑score). WALCL is weekly (as of Wednesday) via H.4.1; RRP is daily; TGA is a Fed liability series. M2 YoY is monthly.

FRED

+3

FRED

+3

FRED

+3

Risk conditions (Daily)

DXY 3‑month momentum (inverted), VIX level (inverted), Credit (HYG/LQD ratio or HY OAS). VIX is a 30‑day constant‑maturity implied vol index per Cboe methodology.

Cboe

+1

Crypto‑internal (Daily)

Stablecoins (USDT+USDC+DAI 30‑day log change), USDT dominance (20‑day, inverted), TOTAL3 (63‑day momentum). Dominance symbols on TV follow a documented formula.

TradingView

Beta & co‑move (Daily)

NDX 63‑day momentum, BTC↔NDX 90‑day correlation.

All components become z‑scores (optionally clipped), weighted, missing inputs drop and weights renormalize. We never use lookahead; we confirm on bar close to avoid repainting per Pine docs (barstate.isconfirmed, multi‑TF).

TradingView

+2

TradingView

+2

What you see on the chart

White line (CLRC) = macro regime score.

Background: Green = Risk‑ON, Red = Risk‑OFF, Teal = Early 3/5 (pre‑signal).

Table: shows each component’s z‑score and the Preference: BTC / ETH / ALTs / Mixed.

Signals & interpretation

Designed for Daily (1D) and Weekly (1W) only.

Regime gates (default Fast preset):

Enter ON: CLRC ≥ +0.8; Hold ON while ≥ +0.5.

Enter OFF: CLRC ≤ −1.0; Hold OFF while ≤ −0.5.

0 / ±1 reading: CLRC is a standardized composite.

~0 = neutral baseline (no macro edge).

≥ +1 = strong macro tailwind (≈ +1σ).

≤ −1 = strong headwind (≈ −1σ).

Early 3/5 (teal): a fast pre‑signal when at least 3 of 5 daily checks align: USDT.D↓, DXY↓, VIX↓, HYG/LQD↑, ETHBTC↑ or TOTAL3↑. It often precedes a full ON flip—use for pre‑positioning rather than full sizing.

BTC/ETH/ALTs selector (only when ON):

ALTs when BTC.D↓ and (ETHBTC↑ or TOTAL3↑) ⇒ rotate down the risk curve.

BTC when BTC.D↑ and ETHBTC↓ ⇒ keep it concentrated.

ETH when ETHBTC↑ while BTC.D flat/up ⇒ add ETH beta.

(Dominance mechanics are documented by TV.)

TradingView

Dissonance (incompatibility) rules — when to stand down

Use these overrides to avoid false comfort:

CLRC > +1 but USDT.D↑ and/or VIX spikes day‑over‑day → downgrade to Neutral; wait for USDT.D to stabilize and VIX to cool (VIX is a fear gauge of 30‑day expectation).

Cboe Global Markets

CLRC > +1 but DXY↑ sharply (USD squeeze) → size below normal; require DXY momentum to roll over.

CLRC < −1 but Early 3/5 = true two days in a row → start reducing underweights; look for ON flip within a few bars.

NetLiq improving (W) but credit (HYG/LQD) deteriorating (D) → treat as mixed regime; prefer BTC over ALTs.

How to use (step‑by‑step)

A. Read on Daily (1D) — main regime

Open CRYPTOCAP:TOTAL3, 1D (panel applied).

Wait for bar close (use alerts on confirmed bar). Pine docs recommend barstate.isconfirmed to avoid repainting on realtime bars.

TradingView

If ON, check Preference (BTC / ETH / ALTs).

Then drop to 4H on your trading pair for micro entries (this indicator itself is not for intraday timing).

B. Confirm weekly macro (1W) — once per week)

Review WALCL/RRP/TGA after the H.4.1 release on Thursdays ~4:30 pm ET. WALCL is “Weekly, as of Wednesday”; M2 is Monthly—so do not expect daily responsiveness from these.

Federal Reserve

+2

FRED

+2

Recommended check times (practical schedule)

Daily regime read: right after your chart’s daily close (confirmed bar). For consistent timing across crypto, many users set chart timezone to UTC and read ~00:05 UTC; you can change chart timezone in TV’s settings.

TradingView

In‑day monitoring: optional spot checks 16:00 & 20:00 UTC (DXY/VIX move during US hours), but act only after the daily bar confirms.

Weekly macro pass: Thu 21:30–22:30 UTC (after H.4.1 4:30 pm ET) or Fri after daily close, to let weekly FRED series propagate.

Federal Reserve

Limitations & data latency (be explicit)

Higher‑TF data & confirmation: FRED weekly/monthly series will not reflect intraday risk in crypto; we aggregate them for regime, not for entry timing.

Repainting 101: Realtime bars move until close. This script does not use lookahead and follows Pine guidance on multi‑TF series; still, always act on confirmed bars.

TradingView

+1

Public‑library compliance: Title EN‑only; description starts in EN; clean chart; justify component mash‑up; no lookahead; no unrealistic claims.

TradingView

Alerts you can use

“Macro Risk‑ON (entry)” — fires on ON flip (confirmed bar).

“Macro Risk‑OFF (entry)” — fires on OFF flip.

“Early 3/5” — fires when the teal pre‑signal appears (not a regime flip).

“Preference change” — BTC/ETH/ALTs toggles while ON.

Publish note: Alerts are fine; just avoid implying guaranteed accuracy/performance.

TradingView

Background research (why these inputs matter)

Liquidity → Crypto: Fed H.4.1 timing and series definitions (WALCL, RRP, TGA) formalize the “net liquidity” concept used here.

FRED

+3

Federal Reserve

+3

FRED

+3

Stablecoins ↔ Non‑stable crypto: empirical work shows bi‑directional causality between stablecoin market cap and non‑stable crypto cap; stablecoin growth co‑moves with broader crypto activity.

Global liquidity link: world liquidity positively relates to total crypto market cap; lagged effects are observed at monthly horizons.

VIX/Uncertainty effect: fear shocks impair BTC’s “safe haven” behavior; VIX is a meaningful risk‑off read.

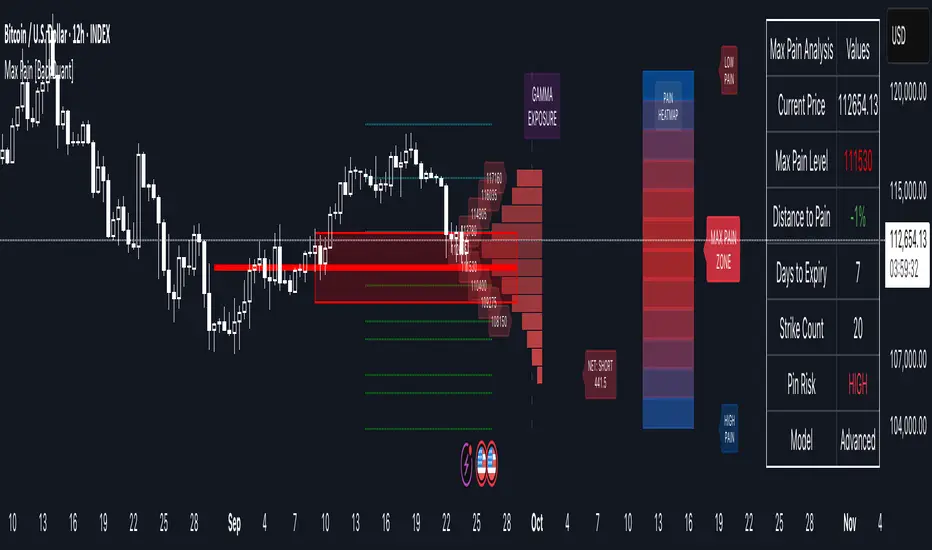

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

GSR BandsGSR Bands is an indicator designed to analyze the dynamics of an implied volatility index based on opening gaps. The model builds an accumulated series of gaps and generates additional offset bands derived from Fibonacci numbers and prime numbers (+10, +20, +30, +50, +70, +80, +110, +125).

The result is a set of cumulative gap curves that help visualize relevant zones in the evolution of the volatility index (potential areas of maximum volatility). Users can customize the offset values displayed on the chart, making it easier to explore different analytical scenarios.

The indicator can be applied to volatility indices such as VIX or VDAX-NEWS, and may serve as a complementary tool when studying the relationship between implied volatility and equity markets.

Note : This indicator does not constitute an investment recommendation. It is intended solely as a technical analysis tool.

Position Size & Stop Loss | QuantEdgeBPosition Size & Stop Loss | QuantEdgeB

QuantEdgeB indicator for calculating risk-based position sizing, leverage, and dynamic stop-loss levels—all in one on-chart dashboard.

🔍 What It Does

1. Position Sizing

o Takes your Portfolio Value and Risk Percentage to compute how much dollar risk you’re willing to take.

o Given an Entry Price and Stop-Loss Price, it derives the per-trade risk and thus the optimal Position Size (number of contracts/shares).

o Based on your available Margin, it calculates the implied Leverage.

2. Stop-Loss Levels

o Offers two modes:

High-Low SL — plots the highest high and lowest low over user-defined lookback windows.

Market-Structure SL — dynamically tracks the current up/down “wick” extremes using an HMA-driven regime filter and places your stop just inside the recent high/low wicks.

o Always overlays both a “Highest Band” and “Lowest Band” as steplines, plus a simple moving average for trend context.

3. Dashboard Table

o Presents all core inputs and outputs in a neat on-chart table:

Portfolio Value, Margin, Risk %, Entry, Stop Loss

Computed Position Size and Leverage

Final Long SL and Short SL levels (depending on your chosen SL type)

o Fully customizable: choose table position, text size, color theme, and transparency.

⚙️ Inputs & Settings

Portfolio Value ($) -> Total account equity.

Margin on Exchange ($) -> Available margin for this trade.

Risk Percentage (%) -> Percent of portfolio to risk per trade.

Entry Price -> Your intended entry level.

Stop Loss Price -> Your intended stop level.

Decimal Places -> Rounding precision for “Position Size.”

Below the hood, “Position Size” is simply the number of units you should buy (or sell) so that, if your stop-loss is hit, you lose exactly your pre-defined risk amount. Here’s how to translate it into a real trade—and a quick example using the script’s default settings:

🔢 What “Position Size” Means - Deep Dive

• Units: the raw number of shares, contracts, or cryptocurrency coins.

• Risk per unit = |Entry Price – Stop-Loss Price|

• Total Risk = Portfolio Value × (Risk %)

• Position Size = Total Risk ÷ Risk per unit

If you trade instruments that are fractional (e.g. BTC) you’ll buy that many coins; if it’s a futures contract, you buy that many contracts; if it’s stock, that many shares.

🧮 Hypothetical Example

1. Inputs

o Portfolio Value = $100 000

o Risk % = 1%

o Entry Price = 105 000

o Stop-Loss Price = 104 000

o Margin Available = $10 000

2. Compute Your Risk Budget

3. Total Risk = 100 000 × (1 / 100) = $1 000

4. Compute Risk Per Unit

5. Risk per Unit = |105 000 – 104 000| = $1 000 per unit

6. Compute Position Size

7. Position Size = 1 000 ÷ 1 000 = 1 unit

o If you’re trading 1 BTC contract, you buy 1 contract.

o If it were stock, you’d buy 1 share.

o If it were spot BTC, you’d buy 1 BTC.

8. Compute Implied Leverage

9. Notional Exposure = Position Size × Entry Price = 1 × 105 000 = $105 000

10. Leverage = 105 000 ÷ 10 000 ≈ 10.5×

11. Place the Trade

o Buy 1 unit at 105 000.

o Place your stop-loss at 104 000.

o If price drifts down to 104 000, you lose exactly $1 000 (1% of your $100 000 account).

📋 Putting It All Together on the Chart

When the indicator’s table shows:

1. Portfolio Value = 100'000

2. Margin = 10'000

3. Risk% = 1%

4. Entry = 105'000

5. Stop Loss = 104'000

6. Size = 1

7. Leverage = 10.5x

…that tells you in plain terms:

“With $100 000 behind me and a 1% risk threshold, buying 1 unit here—with my stop at 104 000—means I stand to lose $1 000 if I’m wrong. I’m using $10 000 of margin, so I’m at roughly 10.5× leverage.”

No more guesswork around lot sizes or margin calls—this table gives you the exact numbers you need to place that order.

🎨 Visual Output

1. Stepline Plots

o Highest Band (short-side stop) in your down-color.

o Lowest Band (long-side stop) in your up-color.

o EMA Trend Line for context.

2. Dashboard Table

o Header with the indicator name.

o First section: all your Position Size inputs & results.

o Separator line + SL-Type label.

o Final section: Long SL and Short SL values under the chosen mode.

o Color and transparency reflect your selected theme.

🧑💼 Why It’s Useful

• Risk-First Sizing: Never guess your position again—risk is dollar-accurately defined.

• Flexible Stop-Loss: Choose the simple bar-high/low bands or an adaptive “wick-insider” based on market structure.

• On-Chart Clarity: Everything you need to size, stop-loss, and monitor your trade sits in one unified panel.

• Customizable: Color themes, font sizes, SL methods, and more—tailor it to your workflow.

Use this indicator to keep your risk parameters crystal-clear, automate your position sizing, and visualize both static and dynamic stop-loss levels—all without leaving your TradingView chart.

Monthly Expected Move (IV + Realized)What it does

Overlays 1-month expected move bands on price using both forward-looking options data and backward-looking realized movement:

IV30 band — from your pasted 30-day implied vol (%)

Straddle band — from your pasted ATM ~30-DTE call+put total

HV band — from Historical Volatility computed on-chart

ATR band — from ATR% extrapolated to ~1 trading month

Use it to quickly answer: “How much could this stock move in ~1 month?” and “Is the market now pricing more/less movement than we’ve actually been getting?”

Inputs (quick)

Implied (forward-looking)

Use IV30 (%) — paste annualized IV30 from your options platform.

Use ATM 30-DTE Straddle — paste Call+Put total (per share) at the ATM strike, ~30 DTE.

Realized (backward-looking)

HV lookback (days) — default 21 (≈1 trading month).

ATR length — default 14.

Note: TradingView can’t fetch option data automatically. Paste the IV30 % or the straddle total you read from your broker (use Mark/mid prices).

How it’s calculated

IV band (±%) = IV30 × √(21/252) (annualized → ~1-month).

Straddle band (±%) = (ATM Call + Put) / Spot to that expiry (≈30 DTE).

HV band (±%) = stdev(log returns, N) × √252 × √(21/252).

ATR band (±%) = (ATR(len)/Close) × √21.

All bands are plotted as upper/lower envelopes around price, plus an on-chart readout of each ±% for quick scanning.

How to use it (at a glance)

IV/Straddle bands wider than HV/ATR → market expects bigger movement than recent actuals (possible catalyst/expansion).

All bands narrow → likely a low-mover; look elsewhere if you want action.

HV > IV → realized swings exceed current pricing (mean-reversion or vol bleed often follows).

Pro tips

For ATM straddle: pick the expiry closest to ~30 DTE, use the ATM strike (closest to spot), and add Call Mark + Put Mark (per share). If the exact ATM strike isn’t quoted, average the two neighboring strikes.

The simple straddle/spot heuristic can read slightly below the IV-derived 1σ; that’s normal.

Keep the chart on daily timeframe—the math assumes trading-day conventions (~252/yr, ~21/mo).

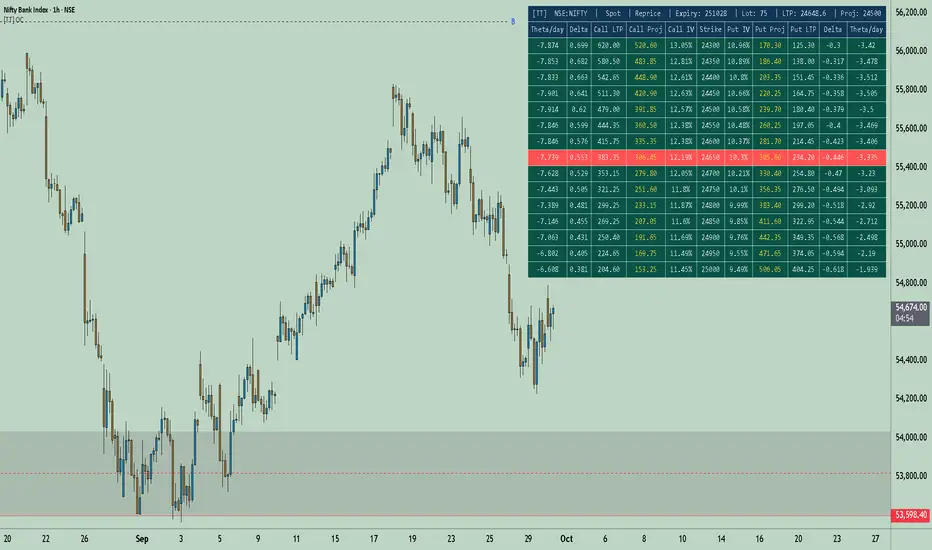

[TT] Option Chain✅Option Geeks for NSE India

Option Geeks is a powerful tool designed for options traders on the NSE (National Stock Exchange of India). It provides real-time visualization and insights based on key option greeks such as Delta, Gamma, Theta, and Implied Volatility (IV) — enabling traders to make more informed decisions when analyzing option chains and positions.

✅What This Script Does:

Calculates and displays the main option greeks for both Call and Put options.

Highlights sensitivity of option prices to changes in:

Underlying price (Delta, Gamma)

Time decay (Theta)

Implied Volatility Calculation.

Tracks live changes in IV and allows comparison across strikes and expiries.

Helps identify favorable option setups and hedging opportunities.

Designed for Bank Nifty, Nifty 50, and top NSE FnO stocks.

✅ How It Works (Conceptually):

Uses a simplified Black-Scholes model adapted for Indian markets.

Takes into account underlying price, strike, days to expiry, interest rate, and volatility to compute the Greeks. Plots real-time values on chart

Manually You need to input the ATM Strike and nearest expiry to update Greeks accordingly.

✅ Who Should Use It:

Options traders seeking deeper insight beyond price charts.

Scalpers and positional traders looking to understand how their trades react to time, price, and volatility.

Anyone trading on NSE’s F&O segment who wants to make smarter trades based on calculated risk metrics

Option CalculatorOption Calculator – Comprehensive Feature Guide

The aiTrendview Option Calculator is a feature-rich options trading dashboard built using Pine Script, designed for real-time market interpretation and strategy selection. It integrates Black-Scholes-based pricing models with dynamic market inputs to help traders evaluate directional bias, volatility, risk, and potential profitability in a structured, intuitive format. The tool supports both beginner and experienced options traders in making data-driven decisions.

Core Inputs and Pricing Foundations

Users can input the strike price, days to expiration, implied volatility (IV), interest rate, and option type (call or put). These values feed directly into calculations for the option's theoretical price, Greeks, and expected move. For example:

• Strike Price helps define moneyness, impacting delta and risk/reward balance.

• Days to Expiry determines the speed of time decay (theta).

• Risk-Free Rate adjusts for time value and interest rate impact (rho).

• Implied Volatility affects premium pricing and vega exposure.

• Option Type sets the directional foundation for strategy analysis.

Live Market Data Integration

The script pulls current underlying price, price change, and volume comparison against a moving average (e.g., current volume vs. 20-day average). This helps identify unusual trading activity or volume spikes. Volatility readings are also incorporated using ATR or external volatility indexes to enhance the realism of IV assessments.

Greek Calculations

The dashboard provides visual and numerical values for all five major Greeks:

• Delta shows directional sensitivity and is plotted with a visual bar.

• Gamma represents the rate of delta change, especially critical near-the-money.

• Theta measures time decay and is most impactful in the final weeks before expiration.

• Vega tracks sensitivity to volatility shifts, crucial for premium-selling strategies.

• Rho reflects sensitivity to interest rates, primarily relevant in long-dated options.

Each Greek is calculated based on real-time inputs, providing a statistical framework for assessing risk and return.

Market Sentiment & Risk Environment

A sentiment scoring system interprets the put-call ratio (PCR), volume trends, and price momentum (e.g., RSI). IV levels are color-coded (e.g., low, medium, high) to identify whether options are relatively cheap or expensive. These values support better timing decisions and help identify whether to be a buyer or seller of premium.

Strategy Recommendation Engine

The script dynamically evaluates six core strategies based on current data:

1. Long Call

2. Short Put

3. Long Put

4. Bull Call Spread

5. Long Straddle

6. Iron Butterfly

Each strategy is assigned a confidence score (0–100%) and updated in real-time. This system is designed to match the appropriate strategy to market conditions such as trend, volatility, and time to expiration.

Risk-Adjusted Trading Insights

The dashboard helps traders evaluate whether to initiate trades, reduce exposure, or wait:

• High Confidence (80%+): Favorable environment; standard sizing recommended.

• Moderate Confidence (60–80%): Trade with caution and reduced risk.

• Low Confidence (<60%): Consider avoiding the trade or waiting for better setup.

It also supports risk mitigation through defined-risk strategies and provides guidance on stop-loss, profit targets, and time-based exits (e.g., managing options with <21 days to expiry).

Real-Time Monitoring

The script continuously tracks:

• Changes in Greeks as price, volatility, or time evolve.

• Profit probability estimates using expected move and breakeven pricing.

• Volume activity and IV rank to spot institutional behavior.

This empowers traders to manage trades proactively, adjust exposure, or lock in profits based on changing market conditions.

Practical Use Case Flow

Step 1: Input Setup

Enter option-specific parameters (strike, expiry days, IV, etc.) and let the dashboard auto-calculate risk metrics.

Step 2: Analyze Market

Use sentiment analysis, IV level, and volume data to understand the environment.

Step 3: Select Strategy

Rely on the confidence score and recommendation engine to choose a suitable options strategy.

Step 4: Manage Risk

Apply size rules based on signal strength, adjust based on exposure, and set alerts if needed.

Step 5: Monitor Outcomes

Track Greeks, probability, and progress metrics to stay informed throughout the trade.

Trading Environment Adaptation

• Low IV: Favor long premium strategies (e.g., long straddles, long calls).

• High IV: Favor premium selling strategies (e.g., iron condors, credit spreads).

• Bullish Markets: Focus on call-based trades or bullish spreads.

• Sideways Markets: Use neutral setups like iron butterflies or calendar spreads.

Position sizing and stop-loss logic are aligned with industry practices (e.g., risk no more than 2% per trade, take profit at 50%, and cut losses at double the premium received).

Dashboard Interpretation Guide

• Green: High confidence strategy, favourable IV, and strong volume confirmation.

• Yellow: Mixed signals or moderate conviction – proceed with caution.

• Red: Low confidence, poor conditions – better to wait for clearer opportunities.

Disclaimer from aiTrendview

This script is intended for educational and informational use only. It does not offer financial advice or trading signals, nor does it guarantee results. aiTrendview and its affiliates are not responsible for any financial loss or decision made using this tool. Options trading involves substantial risk and is not suitable for all investors. Past performance of any strategy or metric does not guarantee future results. Users are encouraged to consult with a certified financial advisor and conduct independent research before making trading decisions.

IV PercentileIV Percentile Indicator - Brief Description

What It Does

The IV Percentile Indicator measures where current implied volatility ranks compared to the past year, showing what percentage of time volatility was lower than today's level.

How It Works

Data Collection:

Tracks implied volatility (or historical volatility as proxy) for each trading day

Stores the last 252 days (1 year) of volatility readings

Uses VIX data for SPY/SPX, historical volatility for other stocks

Calculation:

IV Percentile = (Days with IV below current level) ÷ (Total days) × 100

Example: If IV Percentile = 75%, it means current volatility is higher than 75% of the past year's readings.

Visual Output

Main Display:

Blue line showing percentile (0-100%)

Reference lines at key levels (20%, 30%, 50%, 70%, 80%)

Color-coded backgrounds for quick identification

Info table with current readings

Key Levels:

80%+ (Red): Very high IV → Sell premium

70-79% (Orange): High IV → Consider selling

30-20% (Green): Low IV → Consider buying

<20% (Bright Green): Very low IV → Buy premium

Trading Application

When IV Percentile is HIGH (70%+):

Options are expensive relative to recent history

Good time to sell premium (iron condors, credit spreads)

Expect volatility to decrease toward normal levels

When IV Percentile is LOW (30%-):

Options are cheap relative to recent history

Good time to buy premium (straddles, long options)

Expect volatility to increase from compressed levels

Core Logic

The indicator helps answer: "Is this a good time to buy or sell options based on how expensive/cheap they are compared to recent history?" It removes the guesswork from volatility timing by providing historical context for current option prices.

Improved Historical Volatility Calculator (No Options)Improved Historical Volatility Calculator (No Options)

Description

The "Improved Historical Volatility Calculator (No Options)" is a Pine Script indicator designed to calculate the historical volatility (HV) of assets without relying on options data. This tool is particularly useful for markets like forex, indices, or stocks where options trading might be limited or unavailable. It provides a customizable way to measure volatility based on historical price movements, with options to adjust the calculation period, trading days per year, and use an exponentially weighted moving average (EWMA) for enhanced sensitivity to recent data.

This indicator can be used standalone to visualize volatility trends or integrated with other scripts (e.g., option pricing models) to provide a manual input for implied volatility (IV).

Features

Customizable Period: Adjust the number of days (5 to 365) for volatility calculation.

Flexible Annualization: Set the number of trading days per year (default 252) to suit different markets (e.g., 365 for forex).

EWMA Option: Toggle between standard deviation and EWMA for a more responsive volatility measure.

Trend Adjustment: Removes the influence of price trends using an EMA-based detrending method.

Visual Output: Displays volatility as a histogram and labels the latest value on the chart.

How to Use

Add the Indicator: Load the indicator onto your chart via the Pine Script editor or the Indicators menu.

Configure Settings:

Period for Calculation: Set the lookback period (e.g., 30 days) to calculate volatility.

Trading Days per Year: Adjust for your market (e.g., 252 for stocks, 365 for continuous markets).

Use EWMA: Enable for a weighted approach focusing on recent volatility.

Interpret the Results: The histogram shows volatility in decimal form (e.g., 0.03136 = 3.136%), and the label displays the percentage on the last bar.

Integration: Use the calculated volatility value (in decimal form) as a manual IV input in other scripts, such as option pricing models.

Example

For the DXY index, with a 60-day period and 252 trading days per year, the indicator might output a volatility of 0.03136 (3.136%). You can input this value into an options model to estimate standard deviation levels, adjusting for the days to expiry.

Notes

Accuracy: The indicator provides a reliable estimate of historical volatility, with improvements like trend removal and EWMA. For precision, use a period that matches your trading horizon (e.g., 30-90 days).

Limitations: Volatility is based on historical data and may not reflect future market conditions or implied volatility from options.

Compatibility: Tested on TradingView as of June 16, 2025. Ensure sufficient historical data is available for the chosen period.

Suggestions

Increase the period for volatile assets to smooth out noise.

Share feedback or request enhancements in the comments!

Option Range Projector PRO (with Alerts)Indicator Name: Option Range Projector PRO (with Alerts)

Short Description

This is a powerful and flexible tool for traders that visualizes expected price movement ranges based on option pricing principles and statistical deviations. The indicator plots standard deviation levels (Sigmas) and boundaries calculated from the price of an options Straddle, providing a unique insight into market volatility expectations.

It is ideal for options traders, as well as those who trade futures or spot assets and want to gain an edge by understanding where the market anticipates price boundaries on a specific date.

Core Concepts

The indicator is based on three key ideas:

Standard Deviation (Sigma, σ): In statistics, this is a measure of value dispersion. In trading, when applied to prices, standard deviation levels show the probable range within which the price is expected to remain until a specific date (expiration).

±1σ (1 Sigma): Approximately 68.2% probability that the price will stay within this range.

±2σ (2 Sigmas): Approximately 95.4% probability. These levels often act as strong support/resistance.

±3σ (3 Sigmas): Approximately 99.7% probability. Reaching these levels is a statistically rare event.

Implied Volatility (IV): This is a key component. IV is the market's forecast of the asset's future volatility. It is derived from current option prices and reflects how significant the price movements are expected to be by traders. The higher the IV, the wider the calculated ranges will be.

Straddle-Based Levels: A straddle is an options strategy involving the simultaneous purchase of a Call and a Put option with the same strike price and expiration date. The cost of this combination (Call + Put) directly reflects the market's expected price movement in points. Our indicator uses this value to construct alternative, highly accurate boundaries of the expected range.

Key Features

Flexible Expiration Choice: Easily switch between standard contracts (Weekly, Monthly, Quarterly) or set any custom number of days to expiration (DTE).

Dual Volatility Calculation Mode: Use automatic calculation based on historical data or enter a precise IV value manually (e.g., from your broker's terminal) for maximum accuracy.

Two Types of Predictive Levels: Visualize classic standard deviations (Sigmas) and/or levels calculated from the Straddle price for a comprehensive analysis.

Expiration Comparison: Enable the display of additional levels for a different expiration date to visually compare short-term and long-term market expectations.

"Greeks" Calculation: The indicator calculates and displays key option Greeks (Delta, Gamma, Theta, Vega), helping to deepen the understanding of an option position's characteristics.

Informative Table: All key data—ATM price, IV, DTE, level prices, Greeks, and option prices—are consolidated into one clear table for quick analysis.

Customizable Alerts: Get instant notifications directly in TradingView when the price crosses any of the important levels (±1σ, ±2σ, ±3σ).

Full Visual Customization: Control colors, line thickness, labels, and zone fills to adapt the indicator to your trading style.

How to Use (Settings)

Price Settings:

Auto-detect ATM Price: When enabled, the indicator will use the current closing price as the At-The-Money (ATM) price.

Manual ATM Price: If auto mode is disabled, you can set a precise ATM price manually.

Volatility Settings:

Auto-calculate IV: Calculates historical volatility over a specified period. Useful if you don't have access to real-time IV.

Manual IV Value: (Recommended for accuracy). Enter the Implied Volatility (IV) value for the desired strike from your brokerage terminal or analytical services here.

Expiration:

Contract Type: Choose one of the standard terms (Weekly, Monthly, Quarterly) or "Custom" to use a manual day input.

Days to Expiration: Active only for the "Custom" type.

Show Multiple Expirations: Enables a second set of levels with a different term for comparison.

Straddle Boundaries:

Use Manual Input: Allows you to enter the precise Call and Put Settle prices from the official exchange summary (e.g., from the CME website). This provides the most accurate boundaries based on real market prices.

Trading Ideas and Application

Mean Reversion Trading: The ±2σ and ±3σ levels often act as strong overbought/oversold zones. A price reaching these extreme values has a high statistical probability of reversing or correcting back towards the central ATM price.

Trend Confirmation and Breakouts: A confident close outside the ±1σ range can indicate the beginning of a strong directional move.

Risk Management: Use the levels to set stop-losses or determine profit targets. For example, when opening a trade near the +1σ level, you might consider a target at +2σ and place a stop-loss behind the ATM level.

Volatility Analysis: By comparing the width of the ranges for different expirations, you can assess how the market is pricing short-term versus long-term risks. A narrow range suggests low expectations, while a wide range indicates high ones.

Disclaimer: This indicator is an analysis tool and does not provide direct financial advice or trading signals. All trading decisions are your own. Use this indicator in conjunction with other analysis methods.

ADR, ATR & VOL OverlayThis is a combined version of 2 of my other indicators:

ADR / ATR Overlay

VOL / AVG Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Custom Session Volume

Average For Selected Session

Volume Percentage Comparison

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Custom Session Volume : User chosen time frame to monitor volume

Average For Selected Session : Average for the custom session volume

Volume Percentage Comparison : Current session compared to the average (calculated at session close)

Options:

ADR/ATR:

Time Frame

Length

Smoothing

Volume:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Table:

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement

ADR / ATR Example:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential (coverage) move of 30% in Pre/Post market as suggested by averages.

Custom Volume Session Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed, the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

Volume indicator is for Intra-day time frames, not > Day.

How I use these values:

I use these calculations to determine if a ticker symbol has the necessary range to achieve target gains, to determine if the price oscillation is within "normal" ranges to determine if the trading day will be choppy, and to determine placement of stops and targets within average ranges in combination with support, resistance and retracement levels.

ADR & ATR OverlayADR & ATR Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Options:

Time Frame

Length

Smoothing

Enable or Disable each value

Text Color

Background Color

How to use this indicator:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential move of 30% in Pre/Post market as suggested by averages.

Notes:

These indicators are available as oscillators to place under your chart through trading view but this indicator will place them on the chart in numerical only format.

Please feel free to modify this script if you like but please acknowledge me, I am only a hobby coder so this takes some time & effort.

Black–Scholes model - Options premium calculatorBlack-Scholes Options Pricing Calculator in Pine Script Introduction

The Black-Scholes model is one of the most widely used mathematical models for pricing options. It provides a theoretical estimate of the price of European-style options based on factors such as the underlying asset price, strike price, time to expiration, volatility, risk-free rate, and option type.

This Pine Script implementation of the Black-Scholes options pricing model enables traders to calculate call and put option prices directly within TradingView, helping them assess potential trades more efficiently.

What Does This Script Do?

This script allows traders to input essential option parameters and instantly calculate both call and put option prices using the Black-Scholes formula. It provides:

• A user-friendly interface for inputting option parameters.

• Automatic computation of option prices.

• Real-time updates as market data changes.

Key Features:

• Uses the Black-Scholes formula to compute European call and put option prices.

• User-defined inputs for stock price, strike price, time to expiration, volatility, and risk-free rate.

• Displays calculated option prices on the TradingView chart.

Understanding the Black-Scholes Formula:

The Black-Scholes model is given by the following equations:

C=S0N(d1)−Xe−rtN(d2)C = S_0 N(d_1) - Xe^{-rt} N(d_2) P=Xe−rtN(−d2)−S0N(−d1)P = Xe^{-rt} N(-d_2) - S_0 N(-d_1)

Where:

• CC = Call option price

• PP = Put option price

• S0S_0 = Current stock price

• XX = Strike price

• rr = Risk-free interest rate

• tt = Time to expiration (in years)

• σ\sigma = Volatility of the stock (annualized)

• N(x)N(x) = Cumulative standard normal distribution

• d1d_1 and d2d_2 are given by:

d1=ln(S0/X)+(r+σ2/2)tσtd_1 = \frac{ \ln(S_0/X) + (r + \sigma^2/2)t }{ \sigma \sqrt{t} } d2=d1−σtd_2 = d_1 - \sigma \sqrt{t}

This script implements these calculations efficiently in Pine Script to help traders quickly determine fair values for options based on current market conditions.

Example Calculation:

(The following example values were true at the time of publishing this script. Option prices fluctuate constantly, so actual values may vary.)

• Underlying asset price (NIFTY): 23,519.35

• ATM Call Strike Price: 23,500

• ATM Put Strike Price: 23,550

• IV (Implied Volatility) for Call Option: 8.1%

• IV (Implied Volatility) for Put Option: 10.1%

• Expiry Date: April 3, 2025

Using the Black-Scholes model, the calculated theoretical prices are:

• Theoretical ATM CE price: ₹129

• Theoretical ATM PE price: ₹118

For comparison, the actual option prices from the option chain table at the time of writing were:

• Actual ATM CE price: ₹139.70

• Actual ATM PE price: ₹120.30

As we can see, there is a larger difference between the theoretical price and actual market price for the ATM Call option compared to the ATM Put option.

If you're an experienced trader, you likely know how to use this kind of information to identify potential market inefficiencies or trading opportunities.

How to Use This Script:

1. Add the script to your TradingView chart.

2. Input the necessary parameters such as stock price, strike price, volatility, risk-free rate, and time to expiration.

3. View the calculated call and put option prices directly on the chart.

This Black-Scholes options pricing calculator provides a convenient way to compute theoretical option prices within TradingView. It helps traders analyse whether an option is fairly priced based on market conditions.

While the Black-Scholes model has its limitations (e.g., it does not account for early exercise of American options or dividend payments), it remains a powerful tool for European-style options pricing and a foundational concept in financial markets.

A handy little tool! Unfortunately, this script requires manual data entry since automatic data capture is currently not possible. If this ever becomes feasible in the future, an updated version will be released.

Try it out and let me know your feedback!

Disclaimer:

Please note that this is only for study/educational purpose and is just one of the many tools a trader may use.

Use it at your own risk.

Regards!

NSE & BSE Option Chain - Auto Option Data InputDefinition

An options chain is a list of all available option contracts for a specific security, organized by expiration date and strike price.

What Is an Options Chain ?

Understanding how to read and analyze options chains is crucial for investors venturing into options trading. These display all available option contracts for a particular security, typically in a table format that organizes contracts by expiration date and strike price. The tool provides a wealth of information at a glance, including present prices, trading volume, and implied volatility (IV) for both call and put options.

While the long list of prices and other information can look at first to be overly complicated, learning to navigate an options chain will significantly improve your ability to trade in these derivatives and identify prospects in the market. As options continue to gain popularity among retail investors, mastering the intricacies of the options chain has become an essential skill for those looking to expand their trading strategies beyond traditional stock investments.

Key Takeaways

An options chain displays all available option contracts for a security, organized by expiration date and strike price.

Options chains typically show each contract's bid price, ask price, volume, open interest, and implied volatility (IV).

Options chains can be used to identify trading prospects, such as mispriced options or favorable risk-reward scenarios.

Understanding Options Chains

Option chains list all available option contracts for a particular underlying security. For traders, they provide a snapshot of crucial information about each contract, including strike prices, expiration dates, and market prices.

Typically organized in a table, options chains have separate sections for call and put options. The rows represent different strike prices, while the columns show various data points for each contract. This lets traders quickly compare options with different characteristics to make informed decisions.

Decoding Options Chains

The columns of an option chain, as seen in the example chart above, include the following:

Strike price: The price the option holder can buy (for calls) or sell (for puts) the underlying asset.

Expiration date: The last day the option contract is valid.

1

Bid price: The highest price a buyer is willing to pay for the option.

Ask price: The lowest price a seller is willing to accept for the option.

Last price: The most recent trading price for the option.

Percentage change: The net change column reflects the direction (up, down, or flat) for the underlying asset, as well as the amount of the price shift.

Volume: The number of contracts traded during the current session.

2

Open interest: The total of outstanding contracts.

Mastering the art of reading options chains is essential for any serious options trader. It's where market sentiment, price inefficiencies, and trading prospects all come together.

In options trading, information is power. A well-analyzed option chain can reveal market inefficiencies that savvy traders can exploit. For example, comparing the bid-ask spread across different strike prices can help identify more liquid options, while analyzing open interest can help you understand market sentiment.

A skilled user can quickly decipher an options chain for what it says about price moves and where there are high and low levels of liquidity. For the best trades, this is critical information. For those not quite there yet, let's break down other parts of the options chain tables into manageable parts:

Calls vs. puts: Option chains typically separate call options (the right to buy) from put options (the right to sell). This division allows traders to focus straightaway on bullish or bearish strategies.

Filters and customization: Most trading platforms enable you to customize your options chain view. You can quickly filter by expiration date, strike price range, or specific Greek values to focus on the most relevant contracts.

The Bottom Line

The options chain is indispensable for options traders, providing a comprehensive view of all available contracts for a given security. By learning to read and analyze options chains, you can gain greater clarity about market sentiment, identify trading prospects, and make more informed decisions for your options strategies.

While it takes a bit of time to become proficient in interpreting all the data presented, mastering the options chain is crucial for those looking to leverage the full potential of options trading in their investment approaches.

Fully Auto Option Data Input for All Currently Available NSE Indices and Stock & BSE Sensex Indices

NSE BSE Option Chain with Greeks [Bluechip Algos]This indicator provides option chain information along with greeks of Delta, Vega, Theta, Gamma and Rho.

Make sure inputs are correctly entered; Symbol, reference spot price of ATM, Expiry date and Distance between strikes

Here’s a brief explanation of the logic used for calculating the Greeks in your Pine Script:

Implied Volatility (IV):

Implied Volatility is found using Black-Scholes formula by comparing the market price of the option to its theoretical price. An iterative process is used to adjust the volatility value until the theoretical price matches the market price, effectively reversing the pricing model to deduce the market’s expectation of volatility.

Delta:

Delta is calculated by estimating the probability of the option expiring in the money. This probability is derived using statistical methods based on price movement expectations. It is computed using the cumulative normal distribution function normDist

Gamma:

Gamma is calculated by evaluating how Delta changes when the underlying price moves slightly, giving a sense of the stability of Delta across different price levels. It is computed based on the derivative of Delta concerning the spot price

Theta:

Theta calculates the time decay of an option's value. It estimates how much the option's price will reduce as it gets closer to expiry, assuming all other factors remain constant. For this, the time left to expiry is broken into daily increments to assess the decay rate.

Vega:

Vega is determined by analyzing how the option's price would react to changes in market volatility. It uses the relationship between volatility and option pricing to measure this sensitivity, helping traders understand the impact of fluctuating volatility levels.

Rho:

Rho is calculated by estimating how much the option's price would change for a small increase in the risk-free interest rate. The calculation involves using Black-Scholes to assess how interest rate changes alter the discounted value of the option's payoff.

All computations depend on parameters like the spot price S, strike price X, time to expiry t, risk-free rate r, and volatility σ.

Tomas' Financial Conditions Z Score"The indicator is a composite z-score comprised of the following four components (equally-weighted):

Credit spreads - ICE BofA High Yield Option Adjusted Spread (BAMLH0A0HYM2) and ICE BofA Corporate Index Option Adjusted Spread (BAMLC0A0CM)

Volatility indexes - VIX (S&P 500 implied volatility) and MOVE (US Treasury bond implied volatility)

I've got it set to a 160-day lookback period, which I think is roughly the best setting after some tinkering.

When the z-score is above zero, it throws a red signal - and when the z-score is below zero, it throws a green signal.

This indicator is a follow-on from the "traffic light financial conditions indicator" that I wrote a thread about a couple of months ago.

I moved on from that previous indicator because it is based on the Federal Reserve's NFCI, which is regularly revised, but I didn't take that into account at the time.

So not a great real-time indicator, if the signal can be subsequently revised in the opposite direction weeks later.

This new indicator is based on real-time market data, so there's no revisions, and it also updates daily, as opposed to weekly for the NFCI"

IV Rank/Percentile with Williams VIX FixDisplay IV Rank / IV Percentile

This indicator is based on William's VixFix, which replicates the VIX—a measure of the implied volatility of the S&P 500 Index (SPX). The key advantage of the VixFix is that it can be applied to any security, not just the SPX.

IV Rank is calculated by identifying the highest and lowest implied volatility (IV) values over a selected number of past periods. It then determines where the current IV lies as a percentage between these two extremes. For example, if over the past five periods the highest IV was 30%, the lowest was 10%, and the current IV is 20%, the IV Rank would be 50%, since 20% is halfway between 10% and 30%.

IV Percentile, on the other hand, considers all past IV values—not just the highest and lowest—and calculates the percentage of these values that are below the current IV. For instance, if the past five IV values were 30%, 10%, 11%, 15%, and 17%, and the current IV is 20%, the IV Rank remains at 50%. However, the IV Percentile is 80% because 4 out of the 5 past values (80%) are below the current IV of 20%.

RunRox - Advanced SMC⭐️ Introducing Our Advanced SMC Indicator: Elevate Your Smart Money Concept Trading

We are excited to present our innovative indicator, specifically designed for the Smart Money Concept (SMC). Our approach goes beyond the traditional SMC strategy by offering significant enhancements that can help you achieve stronger trading performance.

We employ a more sophisticated SMC structure, incorporating improved IDM (Inducement) logic, both internal and external structures, and four types of order blocks. This allows for deeper insights into market trends and a clearer understanding of how major market participants may be manipulating price action.

🟠 Indicator Features:

Structure

HTF Structure – Choose any timeframe and display its structure on your current chart.

CHoCH | BOS | IDM – Display any components from this structure.

Market Minor Structure – Swing and Minor structure.

BOS/CHoCH Breaking by (Body | Wick) – Choose the principle for building the structure, either by the candle body or by their wicks.

BOS/CHoCH Move if Swept – When liquidity is taken, decide whether to move the structure line higher or consider it a structural break.

Move CHoCH/BOS – Relocate key points on the chart if the structure becomes too large.

FVG Concept

HTF FVG – Choose any timeframe from which you want to display FVG on your current chart

Three Types of FVG – Classic FVG, Double FVG, Implied Imbalance

Reaction to FVG – Show the market’s reaction to FVG on the chart

Mitigation Method – Select the fill method that suits your approach (Touch/Midline/Complete)

Remove Filled FVG – Remove FVGs from the chart once they have been filled

Combine FVG – Merge several consecutive FVGs into one

Length FVG – Adjust the number of candles that define the FVG

OrderBlock Concept

HTF OrderBlock – Choose any timeframe from which you want to display orderblocks on your current chart

Swing and Minor Orderblocks – Display only the orderblocks you need, whether from the Swing or Minor structure

Four Types of Order Blocks – Advanced OB, Classic OB, BTS/STB zones, Extremum Candle

Block Based on – Decide whether to base the orderblock on candle highs/lows or candle open/close

Mitigation Method – Define when an orderblock is considered filled (Touch/Midline/Complete)

Remove Blocks Older – Remove older orderblocks from the chart

Hide Overlap – Disable overlapping orderblocks when they appear in the same area

Eat Young Blocks – Reduce the size of an orderblock until it fully forms

Hide Distant Blocks – Remove orderblocks that are too far from the current price

Previous Highs & Lows

Four Level Types – Day, Week, Month, Quarter

Style Customization – Choose line color, line style, and transparency

Fibonacci Retracements

10 Template Options – Ten different bases on which you can build your Fibonacci grid

Up to 7 Levels – Add up to seven Fibonacci levels for your convenience

Fibo Inversion – Option to invert the Fibonacci grid

Style Customization – Choose line colors, line styles, and transparency

Additional Functions

Premium & Discount Zones – A popular concept we’ve incorporated to help identify potential trading areas within premium or discount prices

Equal Highs & Lows – High-liquidity levels where market makers may seek liquidity

Color Candles – Automatically colors candles based on the current trend

Market Structure ZigZag – Offers a clear visual of the zigzag pattern on which the structure is built

Key Point Labels – Displays important swing high/low points directly on the chart

General Styling – Customize any chart element, including size, style, color, and transparency

Alert Customization – Over 16 types of alerts, easily configured in a few clicks. Receive only the notifications you need. Custom alerts are also available for developers.

Next, we will provide a detailed overview of all the indicator’s features, accompanied by chart examples.

📈 Structure

What Is IDM?

IDM, or the Institutional Distribution Model, is an advanced concept within SMC that focuses on how institutional players distribute their positions in the market. By analyzing IDM, traders can better anticipate price movements and potential turning points, thereby gaining a meaningful edge in their trading.

In our structure concept, IDM can form under specific conditions. The market does not always provide a high-liquidity point to work with, so we’ve adopted a flexible approach. We generate IDM when a certain type of liquidity appears during the impulse and BOS break, allowing for a potential future liquidity sweep.

Below, I will provide an example that illustrates when IDM forms as a liquidity magnet within the structure - and when it does not.

As shown in the example above, we focus on the initial impulse after the BOS. If liquidity forms during this impulse - liquidity that needs to be taken out during the structural move - we mark an IDM level as a price magnet. However, if this liquidity does not appear, we do not create an IDM. In that case, the same point might serve as an FVG or play a different role, depending on your trading approach.

This concept makes the structure more flexible and better able to respond immediately to market movements and key structural points.

Above is an example on the chart illustrating what the structure looks like both with and without IDM. As you can see, when the structural move includes pullbacks and consolidation, there is an opportunity to form an IDM as a price magnet. However, if the impulses are strong and lack pullbacks, FVG becomes the only magnet in that move. Depending on the chart, our indicator adapts to the current market conditions and highlights potential liquidity collection points.

📊 Swing and Minor Structure

In the new version of the indicator, the minor structure and the swing structure differ from each other.

Swing structure - In this structure, as mentioned earlier, the IDM concept remains a price magnet and is formed at certain points on the chart if the conditions allow. If these points do not appear, IDM might not form at all.

Minor structure - Here, we have completely removed IDM and only kept BOS and CHoCH for structure formation. We found that for a minor structure, this approach allows faster reactions to trend changes, depending on market movements.

By making these adjustments, we have resolved the main issue of the advanced structure, which was the large distance between BOS and CHoCH that sometimes resulted in a month-long consolidation between these levels. In this version, those problems no longer occur.

If, for some reason, your settings result in a larger swing structure, you can still work with the minor structure using the same POI as in the swing structure. OrderBlock and FVG remain the primary drivers of order flow.

Shown above is a screenshot of the main structure settings you can adjust. These settings are highly flexible and can be tailored to fit a wide range of trading preferences.

⚖️ FVG Concept