Combo Strategy 123 Reversal & Ergodic CSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is one of the techniques described by William Blau in his book

"Momentum, Direction and Divergence" (1995). If you like to learn more,

we advise you to read this book. His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship between

price and momentum in step-by-step examples. From this grounding, he then looks

at the deficiencies in other oscillators and introduces some innovative techniques,

including a fresh twist on Stochastics. On directional issues, he analyzes the

intricacies of ADX and offers a unique approach to help define trending and

non-trending periods.

This indicator plots Ergotic CSI and smoothed Ergotic CSI to filter out noise.

WARNING:

- For purpose educate only

- This script to change bars colors.

在脚本中搜索"oscillator"

OBV with DivergenceAll I did was combine the logic from LazyBear for his OBV Oscillator to regular RSI divergence logic (where I replaced the RSI input to use LazyBear's OBV).

I didn't use any original code! Neither OBV (written by LazyBear) nor DIvergence (author unknown) was written by me. I merely modified the sytax a little to combine them.

Very useful for spotting divergences with OBV oscillator.

Combo Strategy 123 Reversal & Directional Trend Index (DTI) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This technique was described by William Blau in his book "Momentum,

Direction and Divergence" (1995). His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship between

price and momentum in step-by-step examples. From this grounding, he then looks

at the deficiencies in other oscillators and introduces some innovative techniques,

including a fresh twist on Stochastics. On directional issues, he analyzes the

intricacies of ADX and offers a unique approach to help define trending and

non-trending periods.

Directional Trend Index is an indicator similar to DM+ developed by Welles Wilder.

The DM+ (a part of Directional Movement System which includes both DM+ and

DM- indicators) indicator helps determine if a security is "trending." William

Blau added to it a zeroline, relative to which the indicator is deemed positive or

negative. A stable uptrend is a period when the DTI value is positive and rising, a

downtrend when it is negative and falling.

WARNING:

- For purpose educate only

- This script to change bars colors.

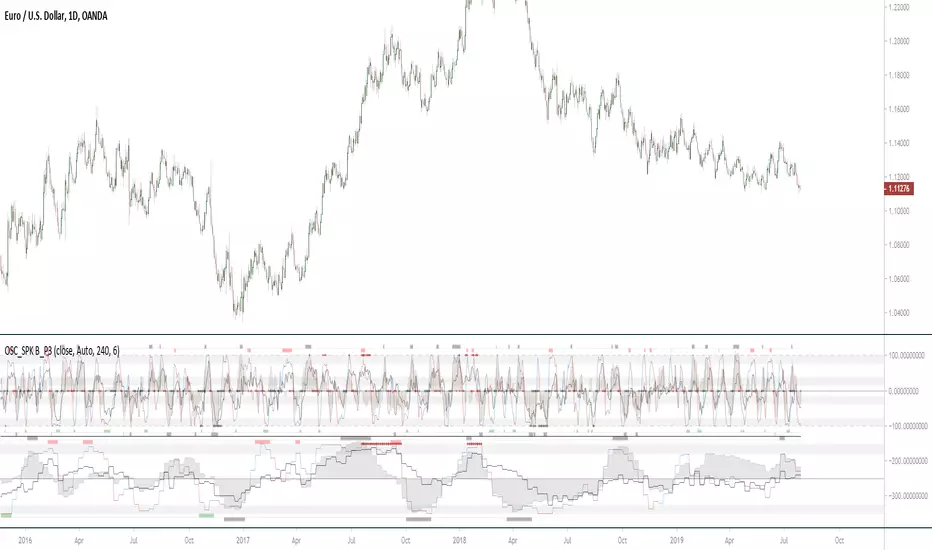

OSC_SpecialK Beta_Pine3A multiple signals|oscillators indicator based on custom stochrsi, custom BB% , CoG, Standard ChandeMoM,Standard overload RSI.

Work with all symbols. Requiert a correct volume source for SpK_Shadow and Fastsignal. (Some index have bad volume)

Legend :

Black Line : Standard ChandeMoM

Blue/Red Line : 14|9|3 StochRSI with sma called SpK

Black Squares : A fast and reactive signal (often a faster retracement, can be relativly horizontal or continuity trend with acceleration ) Really reactive with low interval. (!!Volume dependance!!) called FastSignal.

Red/Green Squares : Need other signal for confirmation. Can be slow to trigger, especially with low interval.(It is important to be in the right trend) Called Signal T1|T2 (!!Volume dependance!!)

Tiny diamond (top/bottom of both section) : Standard RSI saturation

Tiny diamond (middle line of top section) : Center of Gravity signal (standard value I think). Can help to confirm an other signal.

Histogram|area : Work as a difference because it is. Called SpK_Shadow (It's like Peter Pan shadow's ) Can help to see the FastSignal end (when hist arrives near the middle). || In combination with SignalT1/T2 : When shadow is on the middle and you have T1|T2 signals a strong impulsion is possible. (Keep in mind the trend with the LargeTimeFrame ) (!!Volume dependance!!)

Bottom Section is a Large TimeFrame of the top section, with a ratio. I use it to see the level of risk on the interval, according to the targets displayed by my overlay indicator. (OVL_Kikoocycle Beta_Pine3 )

By combining signals and oscillators, it is relatively easy to deduce good opportunities or avoid certain pitfalls. (Keep in mind this script was designed to be used with an overlay indicator, particulary my other script called OVL_Kikoocycle Beta_Pine3 (soon published ) )

Sorry if I do not use traders' common vocabulary...And for my dirty english.

APEX - Bollinger Bands %BBollinger Bands %B is essentially BB Range it is an indicator derived from the standard Bollinger Bands. Bollinger Bands are a volatility indicator that creates a band of three lines which are plotted on the screen.

Bollinger Bands %B works the same as other momentum oscillators, it is best to look for short-term oversold in this case a volatility imbalance between upper and lower volatility. You are looking for values that are near 0 or negative.

Compared to other momentum Oscillators the %B is slightly less responsive than CCI but it does provide more signals than RSI / STOCH and STOCHRSI.

TKE INDICATOR by KıvanÇ fr3762TKE INDICATOR is created by Dr Yasar ERDINC (@yerdinc65 on twitter )

It's exactly the arithmetical mean of 7 most commonly used oscillators which are:

RSI

STOCHASTIC

ULTIMATE OSCILLATOR

MFI

WIILIAMS %R

MOMENTUM

CCI

the calculation is simple:

TKE=(RSI+STOCHASTIC+ULTIMATE OSCILLATOR+MFI+WIILIAMS %R+MOMENTUM+CCI)/7

Buy signal: when TKE crosses above 20 value

Oversold region: under 20 value

Overbought region: over 80 value

Another usage of TKE is with its EMA ,

You can add the EMA line of TKE in the settings menu by clicking the "Show EMA Line" button:

the default value is defined as 5 bars of EMA of the TKE line,

Go long: when TKE crosses above EMALine

Go short: when TKE crosses below EMALine

BioSwarm Imprinter™BioSwarm Imprinter™ — Agent-Based Consensus for Traders

What it is

BioSwarm Imprinter™ is a non-repainting, agent-based sentiment oscillator. It fuses many short-to-medium lookback “opinions” into one 0–100 consensus line that is easy to read at a glance (50 = neutral, >55 bullish bias, <45 bearish bias). The engine borrows from swarm intelligence: many simple voters (agents) adapt their influence over time based on how well they’ve been predicting price, so the crowd gets smarter as conditions change.

Use it to:

• Detect emerging trends sooner without overreacting to noise.

• Filter mean-reversion vs continuation opportunities.

• Gate entries with a confidence score that reflects both strength and persistence of the move.

• Combine with your execution tools (VWAP/ORB/levels) as a state filter rather than a trade signal by itself.

⸻

Why it’s different

• Swarm learning: Each agent improves or decays its “fitness” depending on whether its vote matched the next bar’s direction. High-fitness agents matter more; weak agents fade.

• Multi-horizon by design: The crowd is composed of fixed, simple lookbacks spread from lenMin to lenMax. You get a blended, robust view instead of a single fragile parameter.

• Two complementary lenses: Each agent evaluates RSI-style balance (via Wilder’s RMA) and momentum (EMA deviation). You decide the weight of each.

• No repaint, no MTF pitfalls: Everything runs on the chart’s timeframe with bar-close confirmation; no request.security() or forward references.

• Actionable UI: A clean consensus line, optional regime background, confidence heat, and triangle markers when thresholds are crossed.

⸻

What you see on the chart

• Consensus line (0–100): Smoothed to your preference; color/area makes bull/bear zones obvious.

• Regime coloring (optional): Light green in bull zone, light red in bear zone; neutral otherwise.

• Confidence heat: A small gauge/number (0–100) that combines distance from neutral and recent persistence.

• Markers (optional): Triangles when consensus crosses up through your bull threshold (e.g., 55) or down through your bear threshold (e.g., 45).

• Info panel (optional): Consensus value, regime, confidence, number of agents, and basic diagnostics.

⸻

How it works (under the hood)

1. Horizon bins: The range is divided into numBins. Each bin has a fixed, simple integer length (crucial for Pine’s safety rules).

2. Per-bin features (computed every bar):

• RSI-style balance using Wilder’s RMA (not ta.rsi()), then mapped to −1…+1.

• Momentum as (close − EMA(L)) / EMA(L) (dimensionless drift).

3. Agent vote: For its assigned bin, an agent forms a weighted score: score = wRSI*RSI_like + wMOM*Momentum. A small dead-band near zero suppresses chop; votes are +1/−1/0.

4. Fitness update (bar close): If the agent’s previous vote agreed with the next bar’s direction, multiply its fitness by learnGain; otherwise by learnPain. Fitness is clamped so it never explodes or dies.

5. Consensus: Weighted average of all votes using fitness as weights → map to 0–100 and smooth with EMA.

Why it doesn’t repaint:

• No future references, no MTF resampling, fitness updates only on confirmed bars.

• All TA primitives (RMA/EMA/deltas) are computed every bar unconditionally.

⸻

Signals & confidence

• Bullish bias: consensus ≥ bullThr (e.g., 55).

• Bearish bias: consensus ≤ bearThr (e.g., 45).

• Confidence (0–100):

• Distance score: how far consensus is from 50.

• Momentum score: how strong the recent change is versus its recent average.

• Combined into a single gate; start filtering entries at ≥60 for higher quality.

Tip: For range sessions, raise thresholds (60/40) and increase smoothing; for momentum sessions, lower smoothing and keep thresholds at 55/45.

⸻

Inputs you’ll actually tune

• Agents & horizons:

• N_agents (e.g., 64–128)

• lenMin / lenMax (e.g., 6–30 intraday, 10–60 swing)

• numBins (e.g., 12–24)

• Weights & smoothing:

• wRSI vs wMOM (e.g., 0.7/0.3 for FX & indices; 0.6/0.4 for crypto)

• deadBand (0.03–0.08)

• consSmooth (3–8)

• Thresholds & hygiene:

• bullThr/bearThr (55/45 default)

• cooldownBars to avoid signal spam

⸻

Playbooks (ready-to-use)

1) Breakout / Trend continuation

• Timeframe: 15m–1h for day/swing.

• Filter: Take longs only when consensus > 55 and confidence ≥ 60.

• Execution: Use your ORB/VWAP/pullback trigger for entry. Trail with swing lows or 1.5×ATR. Exit on a close back under 50 or when a bearish signal prints.

2) Mean reversion (fade)

• When: Sideways days or low-volatility clusters.

• Setup: Increase deadBand and consSmooth.

• Signal: Bearish fades when consensus rolls over below ≈55 but stays above 50; bullish fades when it rolls up above ≈45 but stays below 50.

• Targets: The neutral zone (~50) as the first take-profit.

3) Multi-TF alignment

• Keep BioSwarm on 1H for bias, execute on 5–15m:

• Only take entries in the direction of the 1H consensus.

• Skip counter-bias scalps unless confidence is very low (explicit mean-reversion plan).

⸻

Integrations that work

• DynamoSent Pro+ (macro bias): Only act when macro bias and swarm consensus agree.

• ORB + Session VWAP Pro: Trade London/NY ORB breakouts that retest while consensus >55 (long) or <45 (short).

• Levels/Orderflow: BioSwarm is your “go / no-go”; execution stays with your usual triggers.

⸻

Quick start

1. Drop the indicator on a 1H chart.

2. Start with: N_agents=64, lenMin=6, lenMax=30, numBins=16, deadBand=0.06, consSmooth=5, thresholds 55/45.

3. Trade only when confidence ≥ 60.

4. Add your favorite execution tool (VWAP/levels/OR) for entries & exits.

⸻

Non-repainting & safety notes

• No request.security(); no hidden lookahead.

• Bar-close confirmation for fitness and signals.

• All TA calls are unconditional (no “sometimes called” warnings).

• No series-length inputs to RSI/EMA — we use RMA/EMA formulas that accept fixed simple ints per bin.

⸻

Known limits & tips

• Too many signals? Raise deadBand, increase consSmooth, widen thresholds to 60/40.

• Too few signals? Lower deadBand, reduce consSmooth, narrow thresholds to 53/47.

• Over-fitting risk: Keep learnGain/learnPain modest (e.g., ×1.04 / ×0.96).

• Compute load: Large N_agents × numBins is heavier; scale to your device.

⸻

Example recipes

EURUSD 1H (swing):

lenMin=8, lenMax=34, numBins=16, wRSI=0.7, wMOM=0.3, deadBand=0.06, consSmooth=6, thr=55/45

Buy breakouts when consensus >55 and confidence ≥60; confirm with 5–15m pullback to VWAP or level.

SPY 15m (US session):

lenMin=6, lenMax=24, numBins=12, consSmooth=4, deadBand=0.05

On trend days, stay with longs as long as consensus >55; add on shallow pullbacks.

BTC 1H (24/7):

Increase momentum weight: wRSI=0.6, wMOM=0.4, extend lenMax to ~50. Use dynamic stops (ATR) and partials on strong verticals.

⸻

Final word

BioSwarm is a state engine: it tells you when the market is primed to continue or mean-revert. Pair it with your entries and risk framework to turn that state into trades. If you’d like, I can supply a companion strategy template that consumes the consensus and back-tests the three playbooks (Breakout/Fade/Flip) with standard risk management.

Reversal Radar

**Reversal Radar - Multi-Indicator Confirmation System**

This script combines five proven technical analysis methods into a unified reversal signal, reducing false signals through multi-indicator confirmation.

**INDICATORS USED:**

1. ADX/Directional Movement System

Determines trend direction via +DI and -DI comparison. Signal only during downtrend condition (DI- > DI+). Filters out sideways markets.

2. Custom Linear Regression Momentum

Proprietary momentum calculation based on linear regression. Measures price deviation from Keltner Channel midline. Signal on negative but rising momentum (beginning trend reversal).

3. Williams VIX Fix (WVF)

Identifies panic-selling phases. Calculates relative distance to recent high. Signal when exceeding Bollinger Bands or historical percentiles.

4. RSI Oversold Filter

Default RSI < 35 (adjustable 30-40). Filters only oversold zones for reversal setups.

5. MACD Confirmation

Signal only when MACD below zero line and below signal line. Confirms ongoing weakness before potential reversal.

**FUNCTIONALITY:**

The system generates a BUY signal only when ALL activated filters are simultaneously met. Each indicator can be individually enabled/disabled. Flexible parameter adjustment for different markets/timeframes. Reduces false signals through multi-confirmation.

**APPLICATION:**

Suitable for swing trading on higher timeframes (4H, Daily), reversal strategies in oversold markets, and combination with additional confirmation indicators.

Setup: Activate desired filters, adjust parameters to market/timeframe, check BUY signal as entry opportunity. Additional confirmation through volume/support recommended.

**INNOVATION:**

The Custom Linear Regression Momentum is a proprietary development combining Keltner Channel logic with linear regression for more precise momentum detection than standard oscillators.

**DISCLAIMER:**

This tool serves as technical analysis support. No signal should be traded without additional confirmation and risk management.

Smart RSI Divergence PRO | Auto Lines + Alerts📌 Purpose

This indicator automatically detects Regular and Hidden RSI Divergences between price action and the RSI oscillator.

It plots divergence lines directly on the chart, labels signals, and includes alerts for automated monitoring.

🧠 How It Works

1. RSI Calculation

RSI is calculated using the selected Source (default: Close) and RSI Length (default: 14).

2. Divergence Detection via Fractals

Swing points on both price and RSI are detected using fractal logic (5-bar patterns).

Regular Divergence:

Bearish: Price forms a higher high, RSI forms a lower high.

Bullish: Price forms a lower low, RSI forms a higher low.

Hidden Divergence:

Bearish: Price forms a lower high, RSI forms a higher high.

Bullish: Price forms a higher low, RSI forms a lower low.

3. Auto Drawing Lines

Lines are drawn automatically between divergence points:

Red = Regular Bearish

Green = Regular Bullish

Orange = Hidden Bearish

Blue = Hidden Bullish

Line width and transparency are adjustable.

4. Labels and Alerts

Labels mark divergence points with up/down arrows.

Alerts trigger for each divergence type.

📈 How to Use

Use Regular Divergences to anticipate trend reversals.

Use Hidden Divergences to confirm trend continuation.

Combine with support/resistance, trendlines, or volume for higher probability setups.

Recommended Timeframes: Works on all timeframes; more reliable on 1h, 4h, and Daily.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

Source (Close, HL2, etc.)

RSI Length

Toggle Regular / Hidden Divergence visibility

Toggle Lines / Labels

Line Width & Line Transparency

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before using in live trading.

Ehlers Two-Pole StochasticThis indicator implements John Ehlers' Two-Pole Stochastic Filter, a smoother alternative to the traditional stochastic oscillator. Instead of relying on raw %K values, it applies a second-order IIR filter (recursive smoothing) to reduce noise and improve trend clarity.

It outputs a single line oscillating between 0 and 1, with less lag and false signals compared to standard stochastic implementations.

Key Features:

Uses a two-pole filter to smooth the normalized stochastic (%K).

Ideal for detecting clean reversals and trend continuations.

Designed for minimal visual noise and greater signal confidence.

Interpretation:

Values near 1.0 may suggest overbought conditions.

Values near 0.0 may suggest oversold conditions.

Crosses above 0.5 can signal bullish shifts, and below 0.5 bearish shifts.

Recommended Settings:

Default smoothing factor (alpha) is 0.7 — higher values make the output more responsive, while lower values smooth further.

Inspired by concepts from Cybernetic Analysis for Stocks and Futures by John F. Ehlers.

Trend Flow Trail [AlgoAlpha]OVERVIEW

This script overlays a custom hybrid indicator called the Money Flow Trail which combines a volatility-based trend-following trail with a volume-weighted momentum oscillator. It’s built around two core components: the AlphaTrail—a dynamic band system influenced by Hull MA and volatility—and a smoothed Money Flow Index (MFI) that provides insights into buying or selling pressure. Together, these tools are used to color bars, generate potential reversal markers, and assist traders in identifying trend continuation or exhaustion phases in any market or timeframe.

CONCEPTS

The AlphaTrail calculates a volatility-adjusted channel around price using the Hull Moving Average as the base and an EMA of range as the spread. It adaptively shifts based on price interaction to capture trend reversals while avoiding whipsaws. The direction (bullish or bearish) determines both the band being tracked and how the trail locks in. The Money Flow Index (MFI) is derived from hlc3 and volume, measuring buying vs selling pressure, and is further smoothed with a short Hull MA to reduce noise while preserving structure. These two systems work in tandem: AlphaTrail governs directional context, while MFI refines the timing.

FEATURES

Dynamic AlphaTrail line with regime switching logic that controls directional bias and bar coloring.

Smoothed MFI with gradient coloring to visually communicate pressure and exhaustion levels.

Overbought/oversold thresholds (80/20), mid-level (50), and custom extreme zones (90/10) for deeper signal granularity.

Built-in take-profit signal logic: crossover of MFI into overbought with bullish AlphaTrail, or into oversold with bearish AlphaTrail.

Visual fills between price and AlphaTrail for clearer confirmation during trend phases.

Alerts for regime shifts, MFI crossovers, trail interactions, and bar color regime changes.

USAGE

Add the indicator to any chart. Use the AlphaTrail plot to define trend context: bullish (trailing below price) or bearish (trailing above). MFI values give supporting confirmation—favor long setups when MFI is rising and above 50 in a bullish regime, and shorts when MFI is falling and below 50 in a bearish regime. The colored fills help visually track strength; sharp changes in MFI crossing 80/20 or 90/10 zones often precede pullbacks or reversals. Use the plotted circles as optional take-profit signals when MFI and trend are extended. Adjust AlphaTrail length/multiplier and MFI smoothing to better match the asset’s volatility profile.

QT RSI [ W.ARITAS ]The QT RSI is an innovative technical analysis indicator designed to enhance precision in market trend identification and decision-making. Developed using advanced concepts in quantum mechanics, machine learning (LSTM), and signal processing, this indicator provides actionable insights for traders across multiple asset classes, including stocks, crypto, and forex.

Key Features:

Dynamic Color Gradient: Visualizes market conditions for intuitive interpretation:

Green: Strong buy signal indicating bullish momentum.

Blue: Neutral or observation zone, suggesting caution or lack of a clear trend.

Red: Strong sell signal indicating bearish momentum.

Quantum-Enhanced RSI: Integrates adaptive energy levels, dynamic smoothing, and quantum oscillators for precise trend detection.

Hybrid Machine Learning Model: Combines LSTM neural networks and wavelet transforms for accurate prediction and signal refinement.

Customizable Settings: Includes advanced parameters for dynamic thresholds, sensitivity adjustment, and noise reduction using Kalman and Jurik filters.

How to Use:

Interpret the Color Gradient:

Green Zone: Indicates bullish conditions and potential buy opportunities. Look for upward momentum in the RSI plot.

Blue Zone: Represents a neutral or consolidation phase. Monitor the market for trend confirmation.

Red Zone: Indicates bearish conditions and potential sell opportunities. Look for downward momentum in the RSI plot.

Follow Overbought/Oversold Boundaries:

Use the upper and lower RSI boundaries to identify overbought and oversold conditions.

Leverage Advanced Filtering:

The smoothed signals and quantum oscillator provide a robust framework for filtering false signals, making it suitable for volatile markets.

Application: Ideal for traders and analysts seeking high-precision tools for:

Identifying entry and exit points.

Detecting market reversals and momentum shifts.

Enhancing algorithmic trading strategies with cutting-edge analytics.

Grucha Percentage Index (GPI) V2Grucha Percentage Index originally created by Polish coder named Grzegorz Antosiewicz in 2011 as mql code. This code is adapted by his original code to tradingview's pinescript.

What Does it Do

GPI is an oscillator that finds the lowest/highest prices with certain depth and generates signals by comparing the bull and bear bars. It use two lines, one is the original GPI calculation, the other is the smoothed version of the original line.

How to Use

GPI can catch quick volatility based movements and can be used as a confirmation indicator along with your existing trading system. When GDI (default color yellow) crosses above the GDI MA (default colored blue) it can be considered as a bullish movement and reverse can be considered as bearish movement.

How does it Work

The main calculation is done via the code below:

for i=0 to length

if candleC < 0

minus += candleC

if candleC >= 0

plus -= candleC

Simply we are adding green and red bars seperately and then getting their percentage to the bullish movement to reflect correctly in a 0-100 z-score enviroment via the code below:

res = (math.abs(minus)/sum)*100

Rest is all about plotting the results and adding seperate line with smoothing.

Note

These kind of oscillators are not designed to be used alone for signal generation but rather should be used in combination with different indicators to increase reliability of your signals.

Happy Trading.

Donchian Channels %I enjoy Donchian Channels for identifying trends. However, I hate having them on my chart. They are next to impossible to interpret at a glance. This script converts DCs to a % making a useful oscillator. The horizontal lines on the chart correspond to the Fib retracements below 50%. There are many ways to trade using this script and it works on any time frame. Moving average crosses are worth your attention, particularly, the 34 period MA (purple line). Enjoy and happy trading.

Voluminati: Uncovering Market SecretsVoluminati: Uncovering Market Secrets

Overview:

The Voluminati indicator dives deep into the secrets of trading volume, providing traders with unique insights into the market's strength and direction. This advanced tool visualizes the Relative Strength Index (RSI) of trading volume alongside the traditional RSI of price, presenting an enriched perspective on market dynamics.

Features:

Volume RSI: A unique twist on the traditional RSI, the Volume RSI measures the momentum of trading volume. This can help identify periods of increasing buying or selling pressure.

Traditional RSI: The renowned momentum oscillator that measures the speed and change of price movements. Useful for identifying overbought or oversold conditions.

Moving Averages: Both the Volume RSI and traditional RSI come with optional moving averages. These can be toggled on or off and are customizable in type (SMA or EMA) and length.

Overbought & Oversold Fills: Visual aids that highlight regions where the Volume RSI is in overbought (above 70) or oversold (below 30) territories. These fills help traders quickly identify potential reversal zones.

How to Use:

Look for divergence between the Volume RSI and price, which can indicate potential reversals.

When the Volume RSI moves above 70, it might indicate overbought conditions, and when it moves below 30, it might indicate oversold conditions.

The optional moving averages can be used to identify potential crossover signals or to smooth out the oscillators for a clearer trend view.

Customizations:

Toggle the display of the traditional RSI and its moving average.

Choose the type (SMA/EMA) and length for both the Volume RSI and traditional RSI moving averages.

Note: Like all indicators, the Voluminati is best used in conjunction with other tools and analysis techniques. Always use proper risk management.

Stochastic Zone Strength Trend [wbburgin](This script was originally invite-only, but I'd vastly prefer contributing to the TradingView community more than anything else, so I am making it public :) I'd much rather share my ideas with you all.)

The Stochastic Zone Strength Trend indicator is a very powerful momentum and trend indicator that 1) identifies trend direction and strength, 2) determines pullbacks and reversals (including oversold and overbought conditions), 3) identifies divergences, and 4) can filter out ranges. I have some examples below on how to use it to its full effectiveness. It is composed of two components: Stochastic Zone Strength and Stochastic Trend Strength.

Stochastic Zone Strength

At its most basic level, the stochastic Zone Strength plots the momentum of the price action of the instrument, and identifies bearish and bullish changes with a high degree of accuracy. Think of the stochastic Zone Strength as a much more robust equivalent of the RSI. Momentum-change thresholds are demonstrated by the "20" and "80" levels on the indicator (see below image).

Stochastic Trend Strength

The stochastic Trend Strength component of the script uses resistance in each candlestick to calculate the trend strength of the instrument. I'll go more into detail about the settings after my description of how to use the indicator, but there are two forms of the stochastic Trend Strength:

Anchored at 50 (directional stochastic Trend Strength):

The directional stochastic Trend Strength can be used similarly to the MACD difference or other histogram-like indicators : a rising plot indicates an upward trend, while a falling plot indicates a downward trend.

Anchored at 0 (nondirectional stochastic Trend Strength):

The nondirectional stochastic Trend Strength can be used similarly to the ADX or other non-directional indicators : a rising plot indicates increasing trend strength, and look at the stochastic Zone Strength component and your instrument to determine if this indicates increasing bullish strength or increasing bearish strength (see photo below):

(In the above photo, a bearish divergence indicated that the high Trend Strength predicted a strong downwards move, which was confirmed shortly after. Later, a bullish move upward by the Zone Strength while the Trend Strength was elevated predicated a strong upwards move, which was also confirmed. Note the period where the Trend Strength never reached above 80, which indicated a ranging period (and thus unprofitable to enter or exit)).

How to Use the Indicator

The above image is a good example on how to use the indicator to determine divergences and possible pivot points (lines and circles, respectively). I recommend using both the stochastic Zone Strength and the stochastic Trend Strength at the same time, as it can give you a robust picture of where momentum is in relation to the price action and its trajectory. Every color is changeable in the settings.

Settings

The Amplitude of the indicator is essentially the high-low lookback for both components.

The Wavelength of the indicator is how stretched-out you want the indicator to be: how many amplitudes do you want the indicator to process in one given bar.

A useful analogy that I use (and that I derived the names from) is from traditional physics. In wave motion, the Amplitude is the up-down sensitivity of the wave, and the Wavelength is the side-side stretch of the wave.

The Smoothing Factor of the settings is simply how smoothed you want the stochastic to be. It's not that important in most circumstances.

Trend Anchor was covered above (see my description of Trend Strength). The "Trend Transform MA Length" is the EMA length of the Trend Strength that you use to transform it into the directional oscillator. Think of the EMA being transformed onto the 50 line and then the Trend Strength being dragged relative to that.

Trend Transform MA Length is the EMA length you want to use for transforming the nondirectional Trend Strength (anchored at 0) into the directional Trend Strength (anchored at 50). I suggest this be the same as the wavelength.

Trend Plot Type can transform the Nondirectional Trend Strength into a line plot so that it doesn't murk up the background.

Finally, the colors are changeable on the bottom.

Explanation of Zone Strength

If you're knowledgeable in Pine Script, I encourage you to look at the code to try to understand the concept, as it's a little complicated. The theory behind my Zone Strength concept is that the wicks in every bar can be used create an index of bullish and bearish resistance, as a wick signifies that the price crossed above a threshold before returning to its origin. This distance metric is unique because most indicators/formulas for calculating relative strength use a displacement metric (such as close - open) instead of measuring how far the price actually moved (up and down) within a candlestick. This is what the Zone Strength concept represents - the hesitation within the bar that is not typically represented in typical momentum indicators.

In the script's code I have step by step explanations of how the formula is calculated and why it is calculated as such. I encourage you to play around with the amplitude and wavelength inputs as they can make the zone strength look very different and perform differently depending on your interests.

Enjoy!

Walker

MACD Normalized [ChartPrime]Overview of MACD Normalized Indicator

The MACD Normalized indicator, serves as an asset for traders seeking to harness the power of the moving average convergence divergence (MACD) combined with the advantages of the stochastic oscillator. This novel indicator introduces a normalized MACD, offering a potentially enhanced flexibility and adaptability to numerous market conditions and trading techniques.

This indicator stands out by normalizing the MACD to its average high and average low, also factoring in the deviation of the high-low position from the mean. This approach incorporates the high and low in the calculations, providing the benefits of stochastic without its common drawbacks, such as clipping problems. As a result, the indicator becomes exceptionally versatile and suitable for various trading strategies, including both faster and slower settings.

The MACD Normalized Indicator boasts a variety of options and settings. The features include:

Enable Ribbon: Toggle the display of the ribbon accompanying the MACD Normalized, as desired.

Fast Length: Determine the movement speed of the fast line to receive advance notice of potential market opportunities.

Slow Length: Control the movement pace of the slow line for smoother signals and a comprehensive outlook on market trends.

Average Length: Specify the length used to calculate the high and low averages, providing greater control over the indicator's granularity.

Upper Deviation: Establish the extent to which the high and low values deviate from the mean, ensuring adaptability to diverse market situations.

Inner Band (Middle Deviation): Adjust the balance between the high and low deviations to create an inner band signal, giving traders a secondary level of market analysis and decision-making support.

Enable Candle Color: Enable the coloring of candles based on the MACD Normalized value for effortless visualization of trading potential.

Use Cases for the MACD Normalized Indicator

In addition to analyzing market trends and identifying potential trading opportunities, ChartPrime's MACD Normalized Indicator offers a range of applications for traders. These use cases encompass distinct trading scenarios and strategies:

Overbought and Oversold Regions

One of the key applications of the MACD Normalized Indicator is identifying overbought and oversold regions. Overbought refers to a situation where an asset's price has risen significantly and is expected to face a downturn, while oversold indicates a price drop that may subsequently lead to a reversal.

By adjusting the indicator's parameters, such as the upper and inner deviation levels, traders can set precise boundaries to determine overbought and oversold areas. When the MACD moves into the upper region, it may signal that the asset is overbought and due for a price correction. Conversely, if the MACD enters the lower region, it possibly indicates an oversold condition with the potential for a price rebound.

Signal Line Crossovers

The MACD Normalized Indicator displays two lines: the fast line and the slow line (inner band). A common trading strategy involves observing the intersection of these two lines, known as a crossover. When the fast line crosses above the slow line, it may signify a bullish trend or a potential buying opportunity. Conversely, a crossover with the fast line moving below the slow line typically indicates a bearish trend or a selling opportunity.

Divergence and Convergence

Divergence occurs when the price movement of an asset does not align with the corresponding MACD values. If the price establishes a new high while the MACD fails to do the same, a bearish divergence emerges, suggesting a potential downtrend. Similarly, a bullish divergence takes place when the price forms a new low but the MACD does not follow suit, hinting at an upcoming uptrend.

Convergence, on the other hand, is represented by the MACD lines moving closer together. This movement signifies a potential change in the trend, providing traders with a timely opportunity to enter or exit the market.

TOTAL:(RSI+TSI)TOTAL:(RSI+TSI)

This indicator collects instant data of RSI and TSI oscillators. RSI moves between (0) and (100) values as a moving line, while TSI moves between (-100) and (+100) values as two moving lines.

The top value of the sum of these values is graphically;

It takes the total value (+300) from RSI (+100), TSI (+100) and (+100).

The lowest value of the sum of these values is graphically;

It takes the value (-200) from the RSI (0), (-100) and (-100) from the TSI.

In case this indicator approaches (+300) graphically; It can be seen that price candlesticks mostly move upwards. This may not always give accurate results. Past incompatibilities can affect this situation.

In case this indicator approaches (-200) graphically; It can be seen that price candlesticks mostly move downwards. This may not always give accurate results. Past incompatibilities can affect this situation.

The graphical movements and numerical values created by this indicator do not give precise results for price candles.

Unified Composite Index [UCI] [KuraiBlu] [LazyBear]The purpose of this indicator is to combine the four basic types of indicators (Trend, Volatility, Momentum and Volume) to create a singular, composite index in order to provide a more holistic means of observing potential changes within the market, known as the Unified Composite Index . The indicators used in this index are as follows:

Trend - Trend Composite Index

Volatility - Bollinger Bands %b

Momentum - Relative Strength Index

Volume - Money Flow Index

The average price source can’t be altered as I’ve made it an average between ((open + close) / 2) and ((high + low) / 2).

The best way to use this is by observing several of the indicators at once in conjunction with the average, rather than simply using the average produced to determine the right moment to enter, or exit a trade by itself. I've found when one indicator goes way out of bounds relative to the other three (and subsequently, the average array), then it presents a good buying, or selling opportunity.

Some adjustments were made to several of the indicators in order to standardize them on a scale of 1-100 so that they could better accommodate the average array that was finally produced. Thanks to LazyBear for letting me strip down the WaveTrend Oscillator.

T3 Slope Variation [Loxx]T3 Slope Variation is an indicator that uses T3 moving average to calculate a slope that is then weighted to derive a signal.

The center line

The center line changes color depending on the value of the:

Slope

Signal line

Threshold

If the value is above a signal line (it is not visible on the chart) and the threshold is greater than the required, then the main trend becomes up. And reversed for the trend down.

Colors and style of the histogram

The colors and style of the histogram will be drawn if the value is at the right side, if the above described trend "agrees" with the value (above is green or below zero is red) and if the High is higher than the previous High or Low is lower than the previous low, then the according type of histogram is drawn.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included

Alets

Signals

Bar coloring

Loxx's Expanded Source Types

Multi T3 Slopes [Loxx]Multi T3 Slopes is an indicator that checks slopes of 5 (different period) T3 Moving Averages and adds them up to show overall trend. To us this, check for color changes from red to green where there is no red if green is larger than red and there is no red when red is larger than green. When red and green both show up, its a sign of chop.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included

Signals: long, short, continuation long, continuation short.

Alerts

Bar coloring

Loxx's expanded source types

wolfpack by multigrainContext

WolfPack was originally published by @darrellfischer1. The indicator was then made popular as a useful companion to the famous Market Cipher (and other similar) oscillators.

Improvements

Inspired by the Bjorgum TSI I have gone ahead and applied a Exponential Moving Average to the original WolfPack plot. The color changes assist in anticipating trend reversals and curls.

Credits

@bjorgum for the coloring and interpretation ideas

@darrellfischer1 for WolfPack

Fear and Greed IndexI couldn't find one based on the original, so I made my own, it's not quite identical, but it does the job.

Red = greed

Green = fear

I updated a lot of the subcomponents and fixed a bug. I've reduced the smoothing to 1, it was previously 5 if you prefer smoother signals. Also added a McClellan oscillator.

I've commented out the plotting of individual sub-components, just uncomment them to see what they do. Some look like pretty useful indicators on their own.

Enjoy!